A Quiet War Is Being Fought With Your Money

The Dollar Is a Weapon. Here's What's Being Built to Replace It.

February 2022. The United States froze approximately $300 billion in Russian central bank reserves — dollar-denominated assets held in Western financial institutions. Russia couldn’t access them and the announcement arrived in a weekend press release. Predictably, the news cycle moved on within days.

In the finance ministries and central banks of roughly 150 other countries, it did not move on.

What every other nation took away from that moment was this: holding dollar reserves is not the same as owning them. You hold them only as long as the United States allows you to. The world’s supposedly neutral reserve currency turned out to be conditional.

That’s where this piece begins.

In The Hidden Tide, I spent four episodes explaining how the monetary tide has been rising for decades — how it shapes asset prices, how Bitcoin sits outside it. What I didn’t address is who controls the source of the tide, and what happens when two superpowers start fighting over it. That question is what this piece is about.

The weapon hidden inside the safe haven

The dollar’s dominance rests on two properties that seem like they should cancel each other out. On one hand, it’s the world’s safe harbor in a crisis. On the other, it’s the world’s most powerful financial weapon.

The safe harbor side works like this: most of the world’s debt is denominated in dollars. When a bank run, currency collapse, or other financial crisis hits anywhere, everyone scrambles for dollars to service their obligations.

That demand drives the dollar up precisely when everything else is falling. Brent Johnson, the macro strategist who developed the “Dollar Milkshake” theory, captured it well: the dollar’s global debt obligations are a straw reaching into every corner of the world economy. When things go wrong, the straw sucks harder.

The weapon side is less discussed but just as real. The SWIFT network routes international payments. Dollar correspondent banking is the plumbing that makes global trade flow. The U.S. controls the plumbing, so the U.S. can also shut off the water to any country that crosses a line. Russia in 2022 was the most visible use. Iran has lived under it for years. Venezuela and North Korea have faced similar financial isolation. The threat matters even when it isn’t deployed, because it shapes behavior constantly.

Then 2026 added a new chapter. The Iran war was the first time the United States tried to escalate from dollar weaponization to military enforcement — using the Hormuz blockade to cut off Iranian oil from the global market.

What emerged was more complicated than the opening move suggested. Iran retained far greater fire control over the Strait than western analysts had estimated. The US, facing spiking inflation and pressure on its own bond market, was quietly making payments to Iran through a third-party intermediary to keep ships moving. Both the financial weapon and the military were deployed. Neither achieved the intended effect.

That matters structurally in a way that goes beyond geopolitics. The enforcement mechanism behind dollar hegemony has real physical limits, not just political ones.

The tension in all of this: the thing the world uses as its safe haven is also the thing that can be pointed at any country that uses it. This is what Michael Howell calls the Capital Wars — the twenty-first century superpower contest is not armies against armies. It’s two monetary systems fighting for the world’s savings.

Why the dollar keeps winning — and why that’s complicated

Here’s the counter-intuitive part: despite the Russia lesson, the dollar hasn’t lost its dominant position. In some measures it’s strengthened.

The reason is pretty simple. The world has no ready replacement:

The euro doesn’t stand a chance; It’s backed by a single monetary policy set for nineteen countries that rarely need the same thing at the same time.

The yuan is capital-controlled, meaning China’s central bank doesn’t allow free movement in or out. Gold is heavy, slow, and expensive to move across borders.

Bitcoin is still too small and too volatile for sovereign reserve purposes at meaningful scale.

So the world is trapped. Nations know the dollar is weaponized. They have no viable alternative at the scale required. The result is something politically unstable: resentment plus continued use.

This is why central banks have been buying gold at record rates for three consecutive years. Not because they think gold will replace the dollar tomorrow. Because they are quietly building an alternative alongside the dollar system — for the day when the exit becomes more realistic. If you can’t instantly remove yourself from a bad arrangement, you quietly plan a slow exit.

One data point worth noting without overweighting: China’s cross-border payment network — CIPS, its operational SWIFT alternative — surged to all-time high transaction volumes during the Iran war. The conflict that was supposed to reinforce dollar hegemony accelerated adoption of the system being built to route around it.

The newest straw

The stablecoin story matters here, though if you’ve read this publication before, you’ve already seen the mechanism covered in my piece about the CLARITY Act:

What matters for the Capital Wars frame is the strategic layer, not the plumbing.

Dollar-denominated stablecoins have done something decades of financial diplomacy couldn’t: extended the reach of the dollar deep into countries with weak banking systems, capital controls, or currencies that lose value too fast to be useful.

In parts of Africa, Southeast Asia, and Latin America, USDT is functionally the most accessible stable currency many ordinary people can hold. The stablecoin network built itself. The dollar travels it for free.

Howell calls this a second straw in the same milkshake — pulling dollar demand from the global economy even faster and more broadly than the traditional banking system ever did. They reach people and places that correspondent banks never touched.

What China sees when it looks at stablecoin adoption is not a technology story. It sees American monetary power extending into populations it is actively courting economically. The competition is not just for central bank reserves. It’s for the savings of ordinary people across the developing world.

The other side of the board

Understanding what China is doing requires holding two things simultaneously: a defensive play and an offensive one, and they’re two parts of the same strategy.

The internal pressure. China has a debt problem that doesn’t fit neatly into the standard crisis template. Decades of property and infrastructure investment created an enormous debt overhang — denominated in yuan — that cannot be repaid without triggering mass defaults and a deflationary spiral. Raising taxes heavily isn’t available to a government managing political stability. Cutting spending on social and military infrastructure isn’t either. And because the yuan isn’t freely convertible, China can’t let foreign capital serve as the release valve.

So what can it do? The same thing every government has done when facing this structure: quietly devalue the currency against real things. Not against the dollar — that’s a trade war waiting to happen. Against gold.

The tell is in the price. Gold denominated in yuan has been setting all-time highs consistently for years. When a government runs expansionary monetary policy to inflate away a debt burden, the first place it shows up is the gold price in that currency. China’s central bank has been accumulating physical gold at a pace not seen since the 1960s. The story isn’t yuan versus dollar. It’s yuan versus gold.

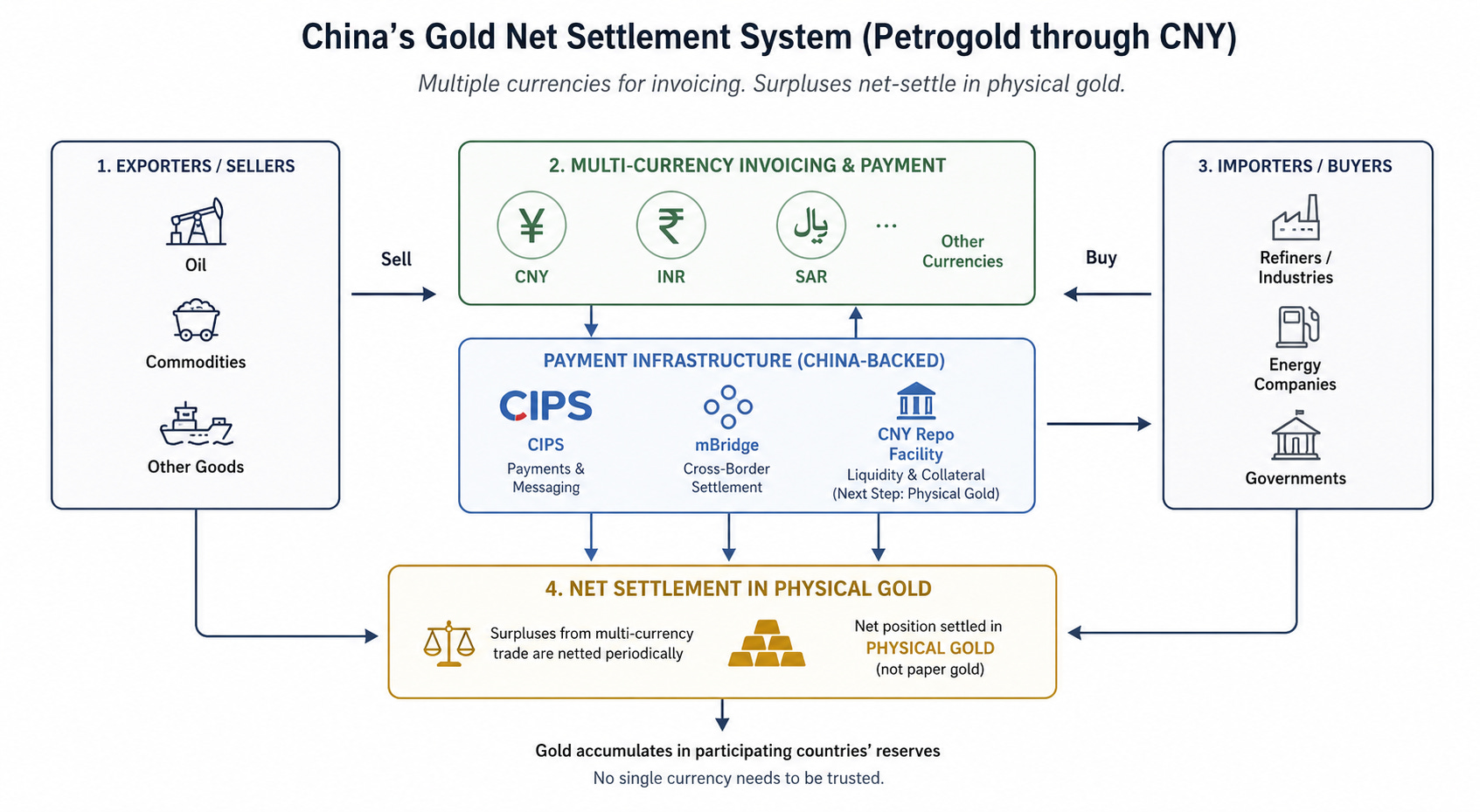

The external construction. China isn’t just accumulating gold internally. Simultaneously, it’s building the infrastructure for a global system in which gold becomes the settlement layer for large-scale energy and commodity trade.

The concept: oil and commodities can be invoiced and paid in multiple currencies rather than exclusively in dollars. The trade surpluses generated by those transactions then net-settle in physical gold. Not paper gold. Not the western “credit gold” held in unallocated accounts. Physical bullion that transfers between central banks.

Macro analysts tracking capital flows have started calling this system “Petrogold through CNY” — a successor to the petrodollar arrangement in which gold, rather than US Treasuries, becomes the reserve asset that accumulates on the back of global energy trade.

The infrastructure for this system is operational, not theoretical:

CIPS — China’s interbank payment network and SWIFT alternative — is already processing cross-border transactions at scale. Its volumes hit all-time highs during the Iran war, as countries needing to route around US-controlled rails found a functional alternative ready for them.

mBridge — a digital cross-border settlement platform backed by the central banks of China, Hong Kong, Thailand, UAE, and Saudi Arabia — is nearing commercial launch at roughly half the fees of conventional international payment systems. Designed specifically for large-scale commodity settlement.

The CNY oil contract, launched in 2018, was the first practical step: giving oil exporters a way to receive yuan instead of dollars for their crude. The result is visible in the data. China’s Treasury holdings and its dollar trade surplus had tracked each other closely for decades. They diverged in 2018 — precisely when the contract launched. China could now accumulate trade surpluses in yuan rather than recycling them back into US government debt.

The CNY repo facility allows foreign central banks and sovereign wealth funds to obtain yuan liquidity using bonds as collateral. The likely next step: physical gold becoming acceptable collateral. That would formally integrate bullion into China’s yuan-based liquidity system.

The Iran deal, if it holds, accelerates all of this. Iranian oil previously locked out of the dollar system by sanctions would flow through Chinese-backed payment channels, with Chinese investment paid in yuan and the resulting surpluses net-settled in gold. The largest single expansion of this system since the 2018 oil contract.

Here is the insight that’s easy to miss: China’s goal is not to replace the dollar with the yuan. In the end, China wants to make gold the settlement layer that sits beneath multiple currencies — so that no single nation’s currency, including China’s, has to be trusted by its trading partners. That’s a subtler and more durable move than simply issuing more yuan.

The one piece neither side controls

Every form of money currently used for major cross-border settlement is controlled by someone. Dollars by the United States. Euros by the ECB and European politics. Yuan by the Chinese Communist Party. Gold by nobody in particular — but it’s heavy, seizable, and slow to cross borders.

Bitcoin is the first widely held monetary asset that is controlled by no government, seizable by no single actor, and movable across borders in minutes. Bitcoin has those properties whether you like Bitcoin or not. Whether the dollar denominated price is $60k or $600k, that’s just how the technology works.

In a world where superpowers are using money as a weapon, an asset that cannot be weaponized has a specific kind of value that didn’t exist at meaningful scale before. You don’t need to believe Bitcoin will become a global reserve currency to recognize that its censorship resistance has strategic properties that are genuinely difficult to replicate.

This isn’t a “buy Bitcoin” conclusion. It’s a map of the board: the dollar is a conditional asset, the yuan is running its own playbook, and for the first time in monetary history there is a neutral option that neither side controls.

What to do with this

Most of us don’t run central banks. We don’t make policy. So what does any of this actually mean?

The honest answer: understanding that you’re living inside a contest between two monetary systems is the first step to thinking clearly about where you store the value of your work. Ask yourself these two questions:

Is the dollar is simultaneously the world’s safe haven and a potential weapon?

Is every national currency is somebody’s policy instrument?

If the answer is yes to one or both, then the question “what should I hold?” is not primarily an investment question. It’s a question about which instruments are most independent from the contest.

Most people have likely never thought about it that way. They’ve been making financial decisions inside a system they assumed was neutral. The Russian finance ministry made the same assumption until February 2022.

February 2022 didn’t start the Capital Wars because they have been running for decades. But it made something visible that had been hidden: every piece of money the world uses is somebody’s instrument. The world is now, slowly and consequentially, responding to that revelation.

The tide has been rising for decades. Now you know who’s fighting over the source.

This piece is a companion to The Hidden Tide — a series exploring the forces that shape money, markets, and wealth. If you’re starting here, Episode 1 is the on-ramp: