Why Bitcoin Absorbs Everything

$188 Trillion Is Looking for a Home. Bitcoin Is Already Absorbing It.

The case for why the world’s liquidity is slowly, inevitably, flowing into a single asset — and what that means for you.

There’s an invisible force that shapes nearly everything in the global economy. It determines whether your retirement account grows or shrinks. It decides whether a first-time homebuyer can afford the down payment or gets priced out. It moves markets before anyone on television has a chance to explain why.

That force is liquidity — the total pool of money available for borrowing, lending, investing, and spending across the global financial system.

Not cash in circulation. Not your savings account balance. Liquidity is bigger than that. It’s the gross capacity of the entire system to create funding. Michael Howell of Cross Border Capital, who has studied this for decades, defines it as the sum of private-sector savings plus changes in financial liabilities — the funding that flows through banks, shadow banks, and corporate balance sheets into asset markets. That funding pool currently stands near $190 trillion, spanning almost 80 economies.

When liquidity expands, asset prices tend to rise. When it contracts, they tend to fall. Not because of earnings reports or product launches — because of plumbing.

And here’s the part most people never consider: what if there were an asset specifically designed to absorb that liquidity without losing any of it?

That’s what Bitcoin is. And that’s what this publication — The Orange Sponge — is built around.

How Liquidity Actually Works

Most people hear “liquidity” and think of cash. But liquidity is better understood as the ability to fund wants and needs. Think about it this way: if Person A has $5,000 in cash and no credit, and Person B has $5,000 in cash plus a $5,000 credit line, Person B has twice the liquidity — even though they have the same amount of money.

This distinction matters because the modern financial system runs on credit, not cash. Debts are no longer paid back with existing money. They’re refinanced — new debt issued to service old debt. Most capital-raising today isn’t funding new productive endeavors; it’s rolling over existing obligations. As a result, the money supply must keep expanding or the entire system faces a cascade of defaults.

This is the engine that drives everything. When central banks expand their balance sheets, they’re adding liquidity. When the U.S. Treasury draws down its cash account at the Fed, that liquidity flows into the banking system. When reverse repo balances shift, liquidity moves with them.

Howell’s Global Liquidity Index tracks these flows on a standardized scale and has identified a roughly 65-month cycle — a predictable rhythm of expansion and contraction that coincides with booms and busts in asset prices. More than 80% of the variation in long-term Treasury yields over the past two decades has been driven by liquidity shifts, not changes in expected Fed policy rates.

In other words, liquidity is the tide. Everything else is a boat.

The Problem With Every Other Store of Value

Here’s where it gets personal.

When I graduated college, I had student debt and credit card debt. I was fortunate to land a good job with a company car, so my expenses were manageable. But when it came to storing the value of my earnings over time, my options were limited — and every single one had serious trade-offs.

Keep cash? Its value erodes every year. The Fed targets 2% annual inflation, and the actual average tends to run higher. A dollar today loses essentially all its purchasing power within 50 years. Holding cash isn’t saving — it’s slow-motion losing.

Savings account? The interest earned almost never keeps up with inflation. And in practice, most people can’t leave money sitting untouched for long. Life happens. Emergencies happen. The money gets spent.

401(k)? This was my best long-term option, especially with employer matching. But it’s essentially illiquid — withdraw before retirement and you’re hit with taxes and penalties. And if a crisis hits at the wrong time (ask anyone who was about to retire in 2008), decades of compounding can get cut in half right when you need it most.

Buy a house? Historically one of the best stores of value for ordinary people, but it requires a down payment many can’t afford, ties up capital in an illiquid asset, and carries the risk of leveraged collapse. I was fortunate to get my home before prices went sky-high. Many younger people today don’t have that option.

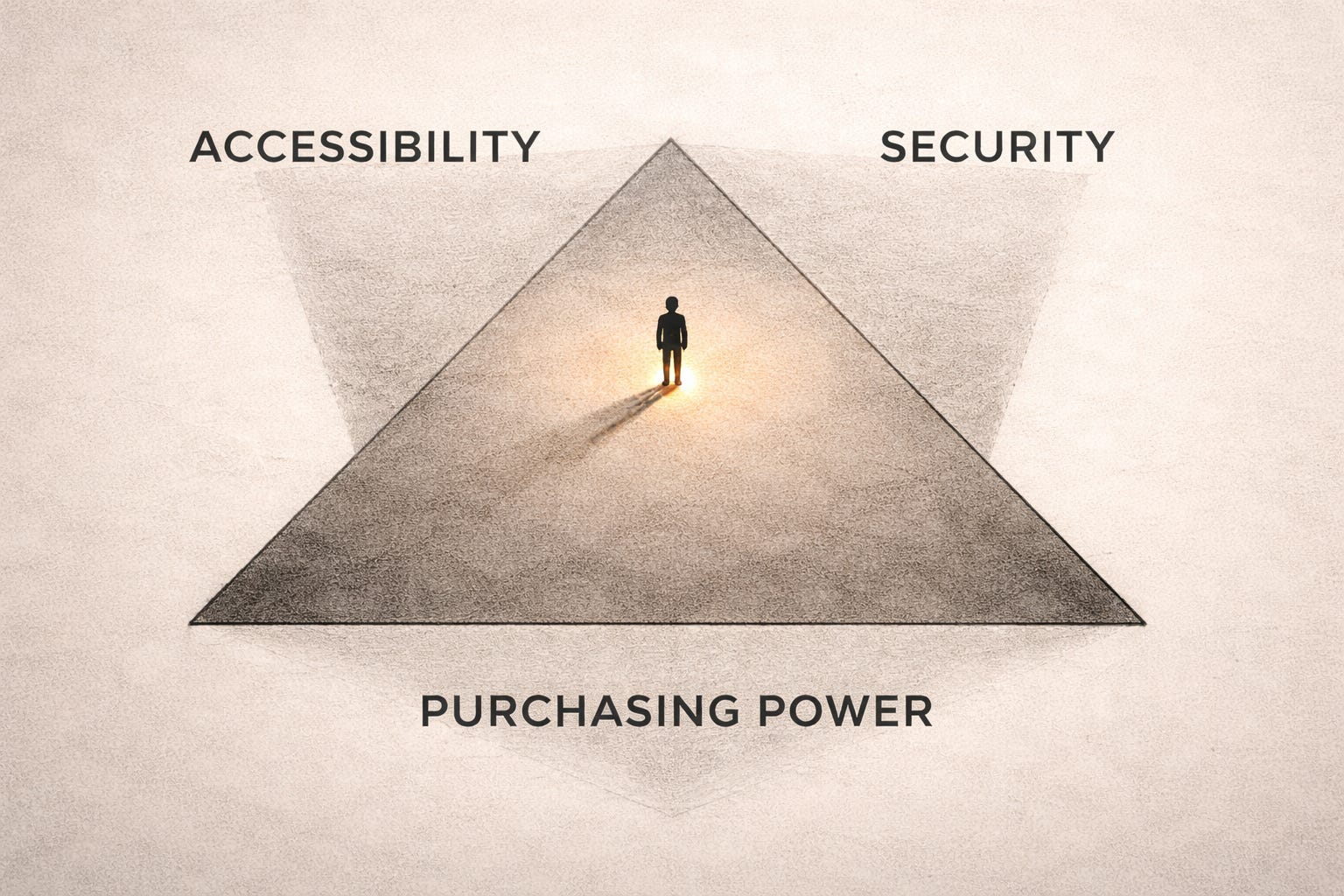

Every one of these instruments forces the same fundamental trade-off: you give up either accessibility, security, or purchasing power. Usually more than one.

And here’s what nobody tells you: the reason you have to play this game at all is because the money you earn loses value the moment you receive it. The system forces everyone to become a gambler or speculator. People think of investing as growing their money. It’s not. It’s protecting the value of their work from fiat debasement.

Why can’t we just earn something, securely store it, and be confident it will have the same or greater purchasing power at a later point in time?

Enter Bitcoin

Bitcoin changes the equation.

Anyone with a smartphone and internet access can acquire it. No minimum investment, no down payment, no gatekeeper, no geographic restriction. When you own a satoshi — the smallest unit of bitcoin — and properly store it with self-custody, you own a piece of digital currency that no one else can create more of. It’s a piece of a whole that is finite: 21 million bitcoin, ever.

Unlike a house, you can exchange your fiat currency for as much or as little as you want. It goes wherever you go, needs no maintenance, and you can freely transact with it for anything large or small. It’s incredibly liquid — you can trade some or all of it back into fiat currency in minutes.

I like to think of the eventual 21 million bitcoins as a single piece of apex real estate — the most desirable property on the planet — where any individual can purchase and own pieces of it. When you hold Bitcoin in self-custody, you really own it. The thing itself, not an IOU that says you own the thing.

This is fundamentally different from every other asset. Think about a house, a piece of fine artwork, or even gold. You can’t acquire bits and pieces of a house. You can’t carry a Rembrandt in your pocket. And even tokenized assets — like XAUT (Tether Gold) — give you a representation of the asset, not the asset itself. A company stands between you and your gold, and that company answers to a government. If the government decides they want the gold, they take it.

Bitcoin is 1:1. No intermediary. No counterparty risk. No one to confiscate, dilute, or debase what you hold.

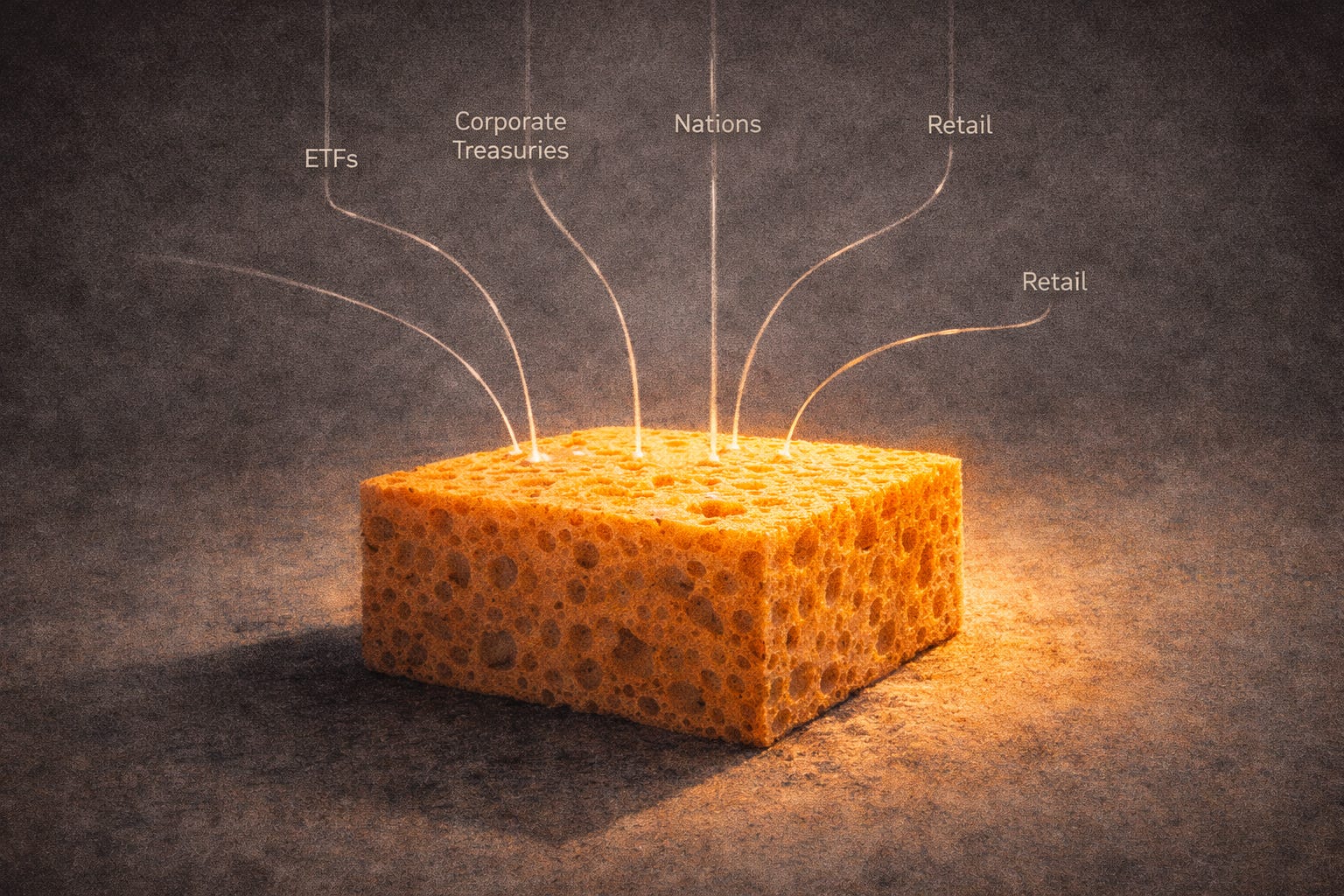

How Bitcoin Is Already Absorbing Liquidity

This isn’t theoretical. It’s already happening — from multiple directions simultaneously.

Through Wall Street. When spot Bitcoin ETFs launched, they became the most popular ETF debut of all time. Billions of dollars flowed in within weeks, outpacing even gold’s ETF launch. Pension funds, mutual funds, 401(k)s, sovereign wealth funds — they all use ETFs to get exposure to assets. Now that Bitcoin lives inside that ecosystem, a portfolio manager can allocate to it with a few clicks. Bitcoin didn’t just step through the door to mainstream finance — it kicked it open.

Through corporate treasuries. Companies are converting cash reserves into Bitcoin. The most prominent example — Strategy (formerly MicroStrategy) — now holds over 762,000 BTC, roughly 3.6% of all Bitcoin that will ever exist, on a single corporate balance sheet. The logic is straightforward: cash on a balance sheet is guaranteed to lose purchasing power over time. Bitcoin, while volatile in the short term, has consistently increased in purchasing power over every meaningful time horizon since its creation. As more CFOs reach this conclusion, more corporate liquidity flows into Bitcoin.

Through real estate and lending. Innovative models are emerging that fuse property assets with Bitcoin as dual collateral for loans. A borrower can refinance a mortgage with the building plus Bitcoin held in escrow, creating a risk-adjusted return that appeals to conservative institutional capital like pension funds. Bitcoin is seeping into the old guard of finance through structures that look familiar to traditional lenders.

Through nations. When the United States froze Russia’s dollar-denominated assets after the invasion of Ukraine, every country in the world took notice. If the reserve currency can be weaponized, then holding it carries a risk most nations hadn’t fully considered. Bitcoin offers something no other reserve asset does — it can’t be frozen, seized, or sanctioned by another nation. Multiple governments are now actively exploring Bitcoin as a strategic reserve asset, and several are already accumulating it. In a multipolar world where trust between nations is declining, a neutral, borderless asset isn’t a novelty — it’s becoming a necessity. Unlike gold, which is expensive and time-consuming to transport (France once had to send a massive ship just to redeem its gold from the United States), Bitcoin can move anywhere, in any amount, almost instantly. And it becomes apparent immediately if someone doesn’t actually have it.

Each of these channels reinforces the others. As more capital flows in, Bitcoin’s market deepens, volatility gradually tempers, and it becomes more attractive to the next pool of capital. It’s a feedback loop — and it’s accelerating.

The Sponge That Doesn’t Change

This is the core metaphor of this publication, and it’s worth sitting with for a moment.

Think of Bitcoin as a sponge. As the financial system creates more and more liquidity — more debt, more credit, more units of currency — that liquidity needs somewhere to go. People and institutions exchange it for assets that they hope will preserve value: real estate, equities, bonds, gold, collectibles.

Bitcoin absorbs that liquidity. But unlike every other asset, the sponge doesn’t change. It doesn’t expand to accommodate more capital. It doesn’t shrink when people withdraw. The supply is fixed. The rules are fixed. No one can alter them — not a CEO, not a central bank, not a government.

Anyone can squeeze liquidity in or out as they please. But the sponge remains the same.

Over time, as more people, companies, and nations recognize this, more liquidity flows in. And because the supply can’t expand to meet demand, each unit becomes more valuable in purchasing power terms. This is the opposite of fiat currency, where the supply must expand continuously, making each unit less valuable over time.

The thesis of The Orange Sponge is simple: this process is inevitable. Not because of hype, not because of speculation, but because of the logical, step-by-step way that Bitcoin has proven useful to very different stakeholders with very different needs. A person trying to escape a debt trap, a pension fund looking for risk-adjusted returns, a nation seeking a neutral reserve asset — they all arrive at the same conclusion through different paths.

Why This Matters for You

If you’re reading this and feeling like something about the financial system doesn’t add up — like you’re working harder but not getting ahead, like your salary increases but your purchasing power doesn’t — you’re not wrong. That’s not a personal failure. That’s the system working exactly as designed.

The money you earn is slowly losing its value. The system requires you to become an investor just to stay in place. And the further you are from the creation of new money — the further you are from Wall Street, from central banking, from the levers of monetary policy — the more this erodes your financial position.

Bitcoin doesn’t fix everything. But it offers something no other asset does: a way to store the value of your work in something that can’t be debased, diluted, or taken from you. Something you can hold yourself. Something that works the same whether you have $50 or $50 million.

I didn’t find Bitcoin because I was looking for it. I found it because I was broke and confused, wondering why working hard wasn’t enough. Everything I’ve learned since then — about money, about economics, about how the system actually works — traces back to that starting point.

This publication is me sharing what I’ve found along the way. Not as an expert. As a student who’s still learning, and who believes more people deserve to understand what’s happening to their money and what they can do about it.

The world’s liquidity is searching for a home. Bit by bit, it’s finding one.

Welcome to The Orange Sponge.

If this shifted how you think about money, Bitcoin, or both — subscribe below. Every week, I explore these ideas further. Because understanding the plumbing matters more than following the headlines.