Darwin's Unfinished Argument

Why bitcoin might be the fittest money

Darwin didn’t think he was writing about money. He was watching pigeons.

Specifically, he was watching how breeders could take one species and, through nothing more than selective breeding over time, produce radically different animals — some bred for speed, some for appearance, some for strength. No grand design required from nature. No master blueprint. Just variation, selection, and time. What he didn’t know — couldn’t have known — is that the same invisible process has been running underneath human monetary history for five thousand years. And right now, we’re watching it happen in real time.

Darwin’s Algorithm, Stripped Down

Most people’s encounter with evolution is somewhere around 7th grade biology — fossils in rock, finches on islands, survival of the fittest in a vague, aggressive sense. And then it just sits there, a concept you recognize but rarely apply anywhere else.

Strip it down to first principles, and Darwin’s insight is almost embarrassingly simple: Variation → Selection → Retention → Time.

In any competitive system, things vary. Some variants survive the selection pressures of their environment better than others. The survivors persist. Their traits carry forward. Over time, through repetition, complex order emerges — not because anyone designed it that way, but because fit traits survive and unfit ones disappear.

No intent. No central planner. No guarantee of fairness. Just pressure, and what survives it.

Darwin himself put it plainly in On the Origin of Species: complex change does not require grand design — only variation, selection, and time. He was writing about finches and orchids. But the logic doesn’t care what you apply it to.

Because here’s what’s interesting: this isn’t just a biology theory. It describes how any competitive system operates over long stretches of time. Markets evolve. Language evolves. Institutions evolve. Ideas evolve. The things that survive do so because their properties made them more fit for the environment they existed in — not because someone voted for them or willed them to win.

Darwin never applied this framework to money. He was a naturalist, not an economist. But he left the door open. And if you walk through it, what you find on the other side is surprisingly clarifying.

Five Thousand Years of Monetary Selection

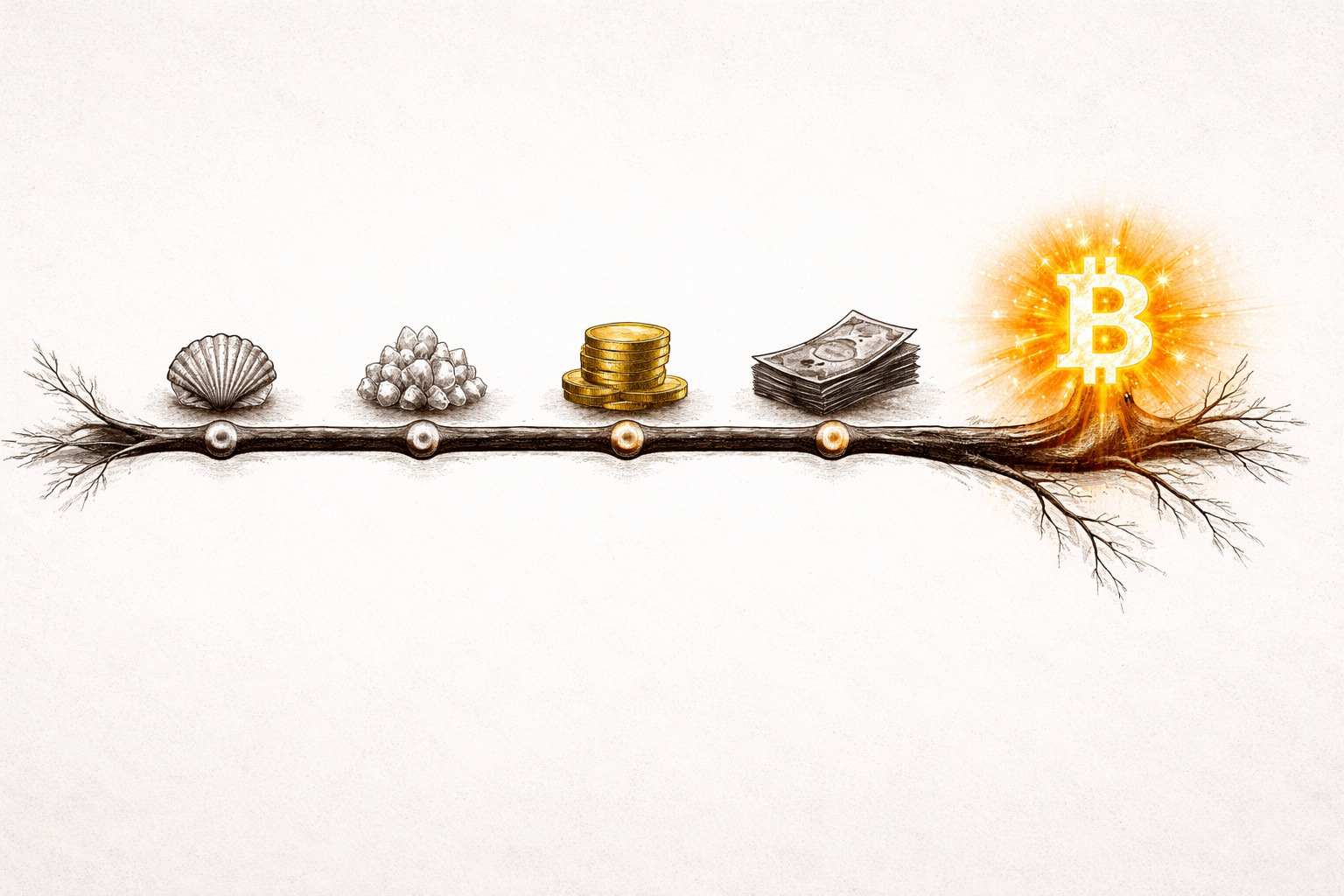

Let’s run a quick thought experiment. Imagine you’re living five thousand years ago. No paper, no banks, no credit cards. You want to trade with someone in the next valley. What do you use?

Whatever it is, it has to solve a specific set of problems. It needs to be portable — you can’t trade with a boulder. It needs to be scarce enough that you can’t just pick it up off the ground, or it’s worthless. It needs to be durable enough not to spoil. Divisible enough to make change. And hard enough to fake that people will trust it.

The monetary history of humanity is a sequence of things rising and falling based on how well they solved those problems. Not because committees convened and made decisions — but because the things that solved the problems better won, and the things that didn’t lost.

Shells worked for a while. Portable, easy to handle. But they weren’t scarce enough — you could gather too many from any beach, which meant anyone could flood the supply. Selection pressure removed them.

Salt was scarce and useful. Whole economies ran on it — the word “salary” comes from the Latin for salt payment. But salt is perishable and doesn’t travel well across wet conditions. Selection pressure removed it.

Gold emerged as the dominant form of money for most of recorded human history. Not because kings declared it valuable — though kings certainly tried to leverage it — but because gold is dense, nearly indestructible, globally scarce, uniform in composition, and extremely difficult to counterfeit with pre-industrial technology. It was fit. The selection pressures of trade, war, and commerce over centuries favored it.

Then came paper — claims on gold, more convenient than hauling metal across long distances. Useful, but with a catch: paper introduced something gold didn’t require. Trust in an intermediary. You weren’t holding the thing. You were holding a promise that the thing existed somewhere and would be honored.

And then fiat currency — paper money backed by nothing but government decree. Enormously flexible for states. Allows central banks to expand the money supply to finance wars, smooth recessions, bail out failing institutions. The properties that made it fit for governments — malleable supply, central control, infinite issuance — are precisely the properties that make it unfit for individuals over time. The debasement mechanism isn’t a bug that crept in accidentally. It’s structural. It was built in.

No single person or committee decided gold would outlast shells. No designer chose paper over salt. Markets, war, convenience, and institutional pressure decided over centuries. That’s natural selection. And it raises an obvious question: what happens when the environment changes again?

The Blocksize Wars: Natural Selection in Real Time

In 2017, Bitcoin nearly tore itself apart.

A faction of developers, miners, and prominent Bitcoin businesses argued that Bitcoin needed to increase its block size — the amount of data each block on the chain could hold. Their reasoning was practical: if Bitcoin was going to scale to millions of users, it needed to handle more transactions faster. Bigger blocks meant more capacity. The argument made intuitive sense.

This was a proposed mutation. A change to Bitcoin’s core properties.

What happened next was one of the most consequential events in Bitcoin’s short history — and most people missed it entirely.

The mutation was rejected. Not by a vote. Not by a committee. Not by Satoshi, who had disappeared years earlier. Not by any authority whatsoever. It was rejected because node operators — ordinary people running Bitcoin software on their own hardware, scattered across the world — simply refused to upgrade. The network didn’t accept the change because the network’s participants didn’t accept it.

The faction that wanted a larger block size eventually forked off and created Bitcoin Cash. They took their mutation and built something separate.

Today, Bitcoin Cash is worth a fraction of Bitcoin — used by a fraction of the people, with a fraction of the network effects.

That is natural selection in a distributed system. The proposed mutation failed the fitness test. Bitcoin’s existing properties — its conservatism, its resistance to easy change, its sheer gravitational weight of accumulated trust and network effects — proved more fit than the proposed change.

There’s a useful analogy from evolutionary biology here. An organism that mutates too easily in response to every environmental stressor can’t stabilize. It can’t build on itself. Fidelity of replication — the ability to faithfully reproduce your core traits generation after generation — is a fitness advantage in its own right. The organisms that last are the ones that change rarely and carefully, and only when the environment truly demands it.

Darwin understood this. Strong ideas, strong organisms, strong systems survive by resisting bad mutations, not by welcoming every proposed change. Bitcoin’s deep skepticism toward alteration isn’t rigidity. It’s fitness.

The Difficulty Adjustment: Adaptation by Design

Let me zoom in on one specific mechanism inside Bitcoin, because I think it’s one of the most elegant solutions I’ve encountered anywhere — in engineering or in nature.

Every roughly two weeks, Bitcoin automatically recalibrates how hard it is to mine a new block. If miners are plentiful — lots of hardware, lots of computing power chasing the cryptographic puzzle — the difficulty goes up. If miners drop off — power outages, hardware failures, government bans, whatever — the difficulty goes down.

The result is almost eerie in its stability: a new Bitcoin block gets produced approximately every 10 minutes, regardless of what happens in the external environment.

Here’s why that matters. In 2021, China banned Bitcoin mining. Not throttled it. Banned it. Roughly 50% of the world’s entire mining capacity went offline within months. Every critic pointed at this and said: this is it. The network will seize. The blocks will stop. Bitcoin will choke.

The difficulty adjustment kicked in. Mining difficulty dropped sharply to reflect the new reality. The remaining miners — now spread more widely across North America, Central Asia, and elsewhere — picked up the slack. The network never missed a beat. A new block every 10 minutes, same as always.

Think of it like a body’s immune response: the environment attacks, the system recalibrates, core integrity is preserved.

But here’s the nuance that I want to make sure lands correctly, because the Darwinian framing can accidentally obscure something important.

The difficulty adjustment didn’t emerge randomly. It wasn’t stumbled into. Before Satoshi published the Bitcoin whitepaper in 2008, there had been years of failed attempts at digital currency — e-gold, DigiCash, b-money, Hashcash, and others. Each failed for specific, documentable reasons. e-gold was seized by governments. DigiCash required trusted intermediaries and folded when the company did. b-money remained theoretical, never solving the double-spend problem cleanly. Hashcash worked as a proof-of-work concept but couldn’t function as a currency.

Satoshi had studied these failures. He understood exactly what selection pressures a digital currency would face — government hostility, mining concentration, hardware arms races, supply shocks, coordination attacks. The difficulty adjustment wasn’t an accidental adaptation that the network happened to develop. It was engineered deliberately by someone who had watched enough specimens fail to understand what fitness actually required.

This is what makes Bitcoin genuinely remarkable: not that it evolved without a designer, but that its designer understood the evolutionary pressures so thoroughly that he could engineer survival into the architecture from the start. Satoshi’s genius wasn’t only technical. It was ecological — an unusually clear-eyed reading of the environment that allowed him to build something with adaptation baked in as a first principle.

Darwin documented how organisms acquire fitness over millions of years through trial, error, and selection. Satoshi compressed that logic into a whitepaper and a few thousand lines of code — and got it right the first time, because he had already done the naturalist’s work of observing what failed and asking why.

The Uncomfortable Darwinian Truth

Darwin quietly teaches something that makes people uncomfortable: nature doesn’t reward intention. It rewards fitness.

The organisms that survive aren’t necessarily the most elegant, the best-marketed, or the ones with the most institutional support. They’re the ones that survive the pressure they actually face.

Apply this to money, and it gets clarifying fast.

Fiat currency has enormous institutional backing. Governments endorse it, mandate it, and in most countries legally require it for tax payments and debt settlement. Banks promote it. Every school teaches it. Central banks employ armies of economists to manage it. It has intention behind it, authority behind it, legal infrastructure behind it.

But good intentions don’t confer fitness. The structural debasement mechanism — the built-in pressure that erodes purchasing power over time — is a fitness liability at the individual level. A dollar in 1971, the year Nixon ended the gold standard, has the purchasing power of roughly a nickel today. That isn’t bad luck. That isn’t mismanagement. It’s the predictable, structural output of a system designed to allow monetary expansion without the constraint of a scarce underlying asset.

Bitcoin has no marketing department. No government endorsement. No central authority advocating for its survival. It has been called a Ponzi scheme, a tool for criminals, an environmental catastrophe, a speculative bubble, and a fad. It has survived every one of those characterizations by simply continuing to function.

It survives because its properties make it fit — not because anyone is rooting for it.

This reframes the entire Bitcoin debate in a way I find genuinely useful. The question isn’t “will enough people adopt it?” or “will institutions embrace it?” — natural selection doesn’t ask for permission or require a consensus vote before it operates. The question is simpler: does Bitcoin have the fitness traits to survive the selection pressures it actually faces? Fifteen years of track record — through exchange collapses, regulatory attacks, fork wars, country-level mining bans, and price swings that would have destroyed almost any other asset class — suggests: yes.

This also explains something about early Bitcoin adopters that sometimes confuses people from the outside — the conviction, the intensity, occasionally the frustration when people dismiss it. They aren’t zealots. They’ve looked at the evolutionary logic — the fitness properties, the selection history, the structural liabilities of the alternative — and followed it to its conclusion. Whether you agree with that conclusion or not, the reasoning behind it is more serious than it typically gets credit for.

Final Thoughts

Darwin sat on On the Origin of Species for twenty years before he published it.

He had the core argument worked out. He had the evidence. He spent two decades collecting more, anticipating objections, and sharpening the framework. He knew the book would be disruptive. He published anyway, eventually, because the argument was sound and the evidence was overwhelming.

His insight was never really about biology in the narrow sense. It was about how complex, adaptive order emerges — not from a grand designer imposing will on matter, but from variation, selection, and time operating on whatever exists. The natural world was simply where the evidence was clearest.

Money is one of the most complex adaptive systems humanity has ever built. It has been evolving for five thousand years — through shells and salt and gold and paper and digital ledgers — and the selection pressures it faces today are unlike any it has faced before. You can move value across borders in minutes. You can freeze a nation’s treasury with a phone call. You can create a trillion dollars without a printing press.

Most of us are living through a significant monetary selection event right now, without quite realizing we’re watching evolution happen in real time.

You don’t need to buy Bitcoin to take this question seriously. But it might be worth asking what Darwin would have asked — which isn’t “who do I want to win?” but something quieter and more honest: which money is fit?

He would have had a lot to say about 2009. He would have recognized it immediately.