Fed Liquidity Watch #2: Weekly H.4.1 Liquidity Breakdown

Week Ended February 25, 2026: Reserves Rebound, Treasury Drains, Liquidity Stabilizes

Last week, liquidity slipped.

This week, it recovered.

Not dramatically. Not explosively. But enough to matter.

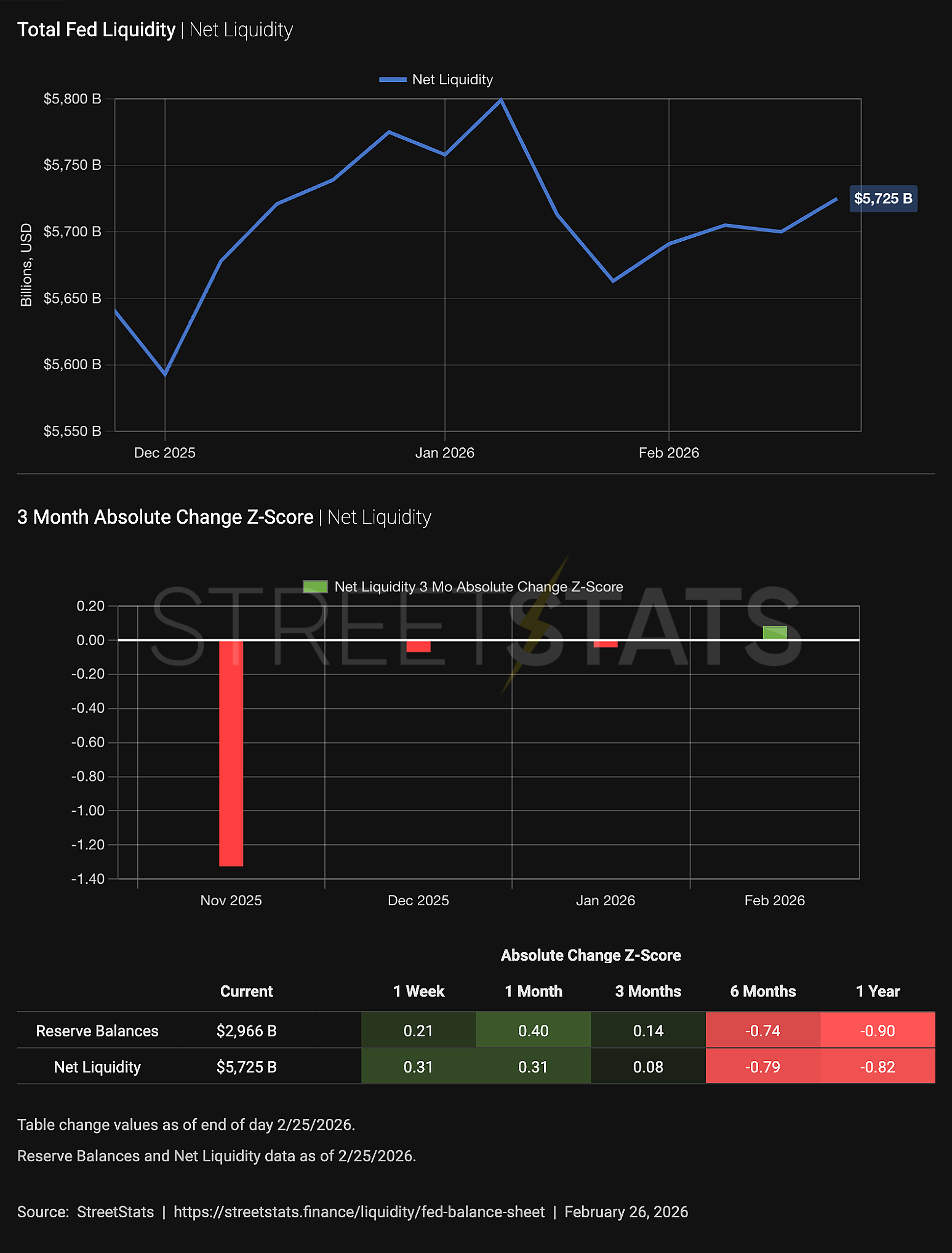

At 4:30 PM, the Fed released its latest H.4.1. Buried inside the tables — no headlines, no commentary — reserves rose $16B to $2.97T.

After a sharp drain the week before, the system absorbed cash again.

The question isn’t whether that happened.

The question is why.

What Changed This Week

Here are the mechanics:

Reserve balances: $2.97T (+$16B)

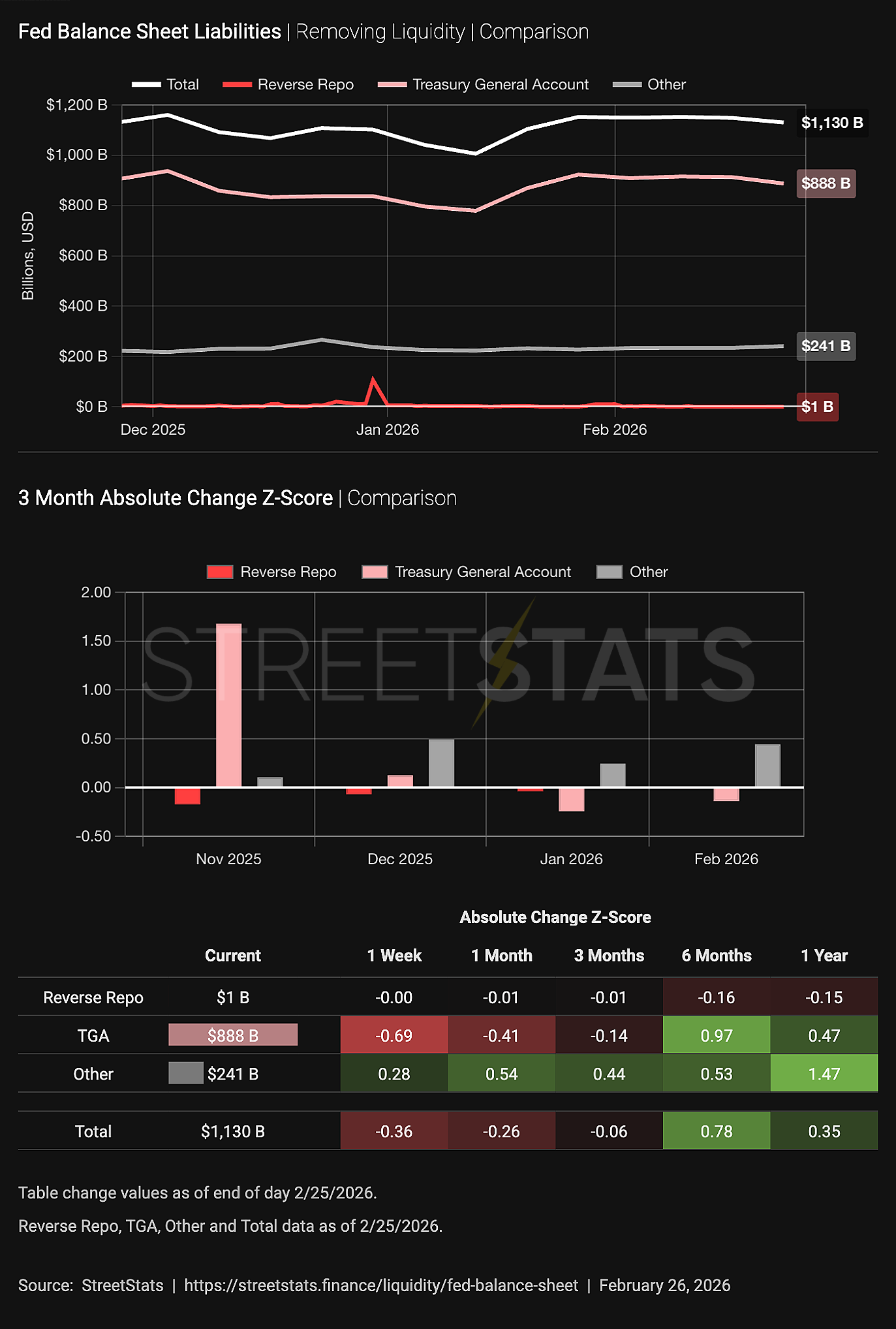

Treasury General Account (TGA): $888B (−$25B)

Reverse Repo (RRP): $321B (−$3.7B)

Treasury securities held outright: +$14.9B

MBS: −$3.9B

Reserves rose because the Treasury spent.

That’s the story.

The Mechanism

Last week, the Treasury rebuilt its General Account aggressively, pulling cash out of the banking system and driving reserves lower.

This week, it did the opposite.

When the TGA declines, cash moves back into commercial bank deposits. That increases reserves. This week’s $25B TGA drawdown was the primary driver of the $16B reserve rebound.

Reverse repo declined slightly — modest liquidity addition.

On the asset side, Reserve Management Purchases continued to add Treasury bills, while MBS runoff continued steadily.

Assets rose.

Liabilities absorbed less.

Reserves increased.

This wasn’t easing policy.

It was flow.

If you track net liquidity (Fed assets minus TGA minus RRP), this week reflects stabilization.

Not expansion.

Stabilization.

That distinction matters.

Liquidity regimes don’t flip instantly. They oscillate. They test boundaries. They build pressure.

We are still in a plateau.

The Regime as of February 25, 2026

QT has ended.

Treasury bill purchases continue.

MBS runoff remains gradual.

The TGA is the dominant short-term liquidity lever.

Reverse repo balances are far lower than during peak QT, reducing the system’s liquidity buffer.

Reserves rebounded this week after a sharp prior drawdown.

There is no stress signal.

No surge in emergency lending.

No hidden acceleration in asset growth.

The system is adjusting within a range.

This chart continues to show where liquidity is actually being removed: Treasury cash balances and reverse repo.

Asset growth is steady.

MBS runoff is predictable.

The Treasury is volatile.

That makes this a cash-cycle environment.

And cash cycles move faster than policy cycles.

The Bitcoin Lens

Fed liquidity is not the whole story.

Global liquidity matters. China matters. Dollar funding conditions matter.

But Fed reserves anchor the system.

When reserves contract sharply, risk compresses.

When reserves expand persistently, risk breathes.

This week’s rebound does not signal a new expansion regime. It simply offsets last week’s drain.

We remain inside a liquidity plateau.

And plateaus build tension.

If TGA volatility continues, liquidity will oscillate within this band. If asset growth begins to outpace Treasury rebuilding consistently, that’s when conditions shift.

The balance sheet will show it before price does.

The Bottom Line

Liquidity stabilized.

Reserves rose.

Treasury drained less.

Reverse repo drifted lower.

Nothing dramatic.

But liquidity shifts rarely announce themselves. They accumulate.

We’ll look again next Thursday.

Because markets follow narratives.

But they move on liquidity.