Fed Liquidity Watch // Issue #10

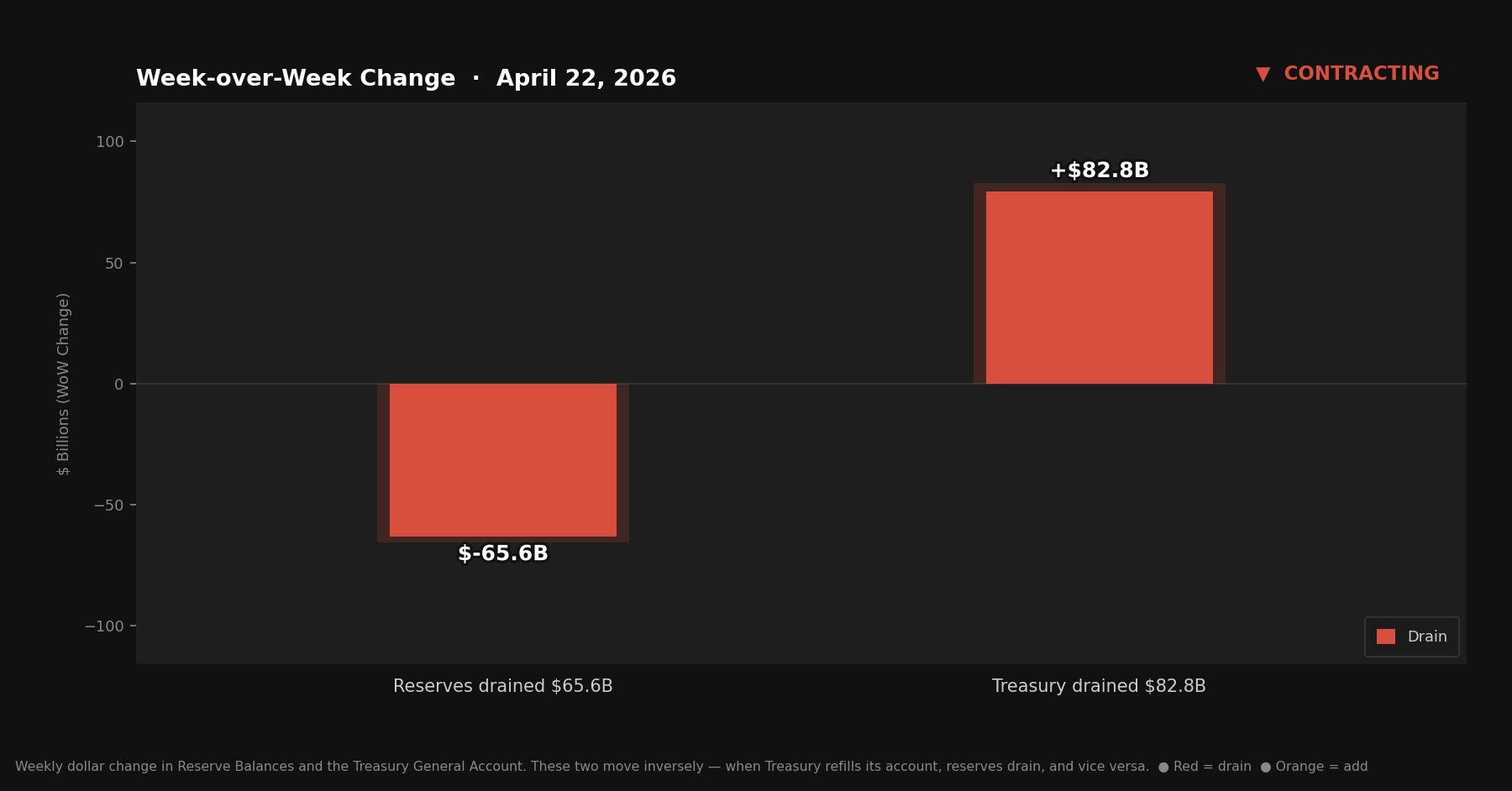

The TGA rose another $82.8B this week, pushing it above $1 trillion for the first time in this series. Reserves fell $65.6B. The reservoir is even larger than it was last week — and it will eventually

Issue #9 ended with a question: the TGA was sitting at $924.4 billion — the highest level in this series — and whether Treasury would begin spending it down or keep building.

This week answered that question.

The Treasury kept building.

Quick Update — Report Release: April 23, 2026

Three rows from Table 1, Wednesday column:

Reserve balances with Federal Reserve Banks: $2,914.6B — down $65.6B from last week

U.S. Treasury General Account (TGA): $1,007.2B — up $82.8B from last week

Reverse repurchase agreements (RRP): $325.1B — down $14.7B from last week

Liquidity Signal — Week of April 22, 2026

Direction: Contracting

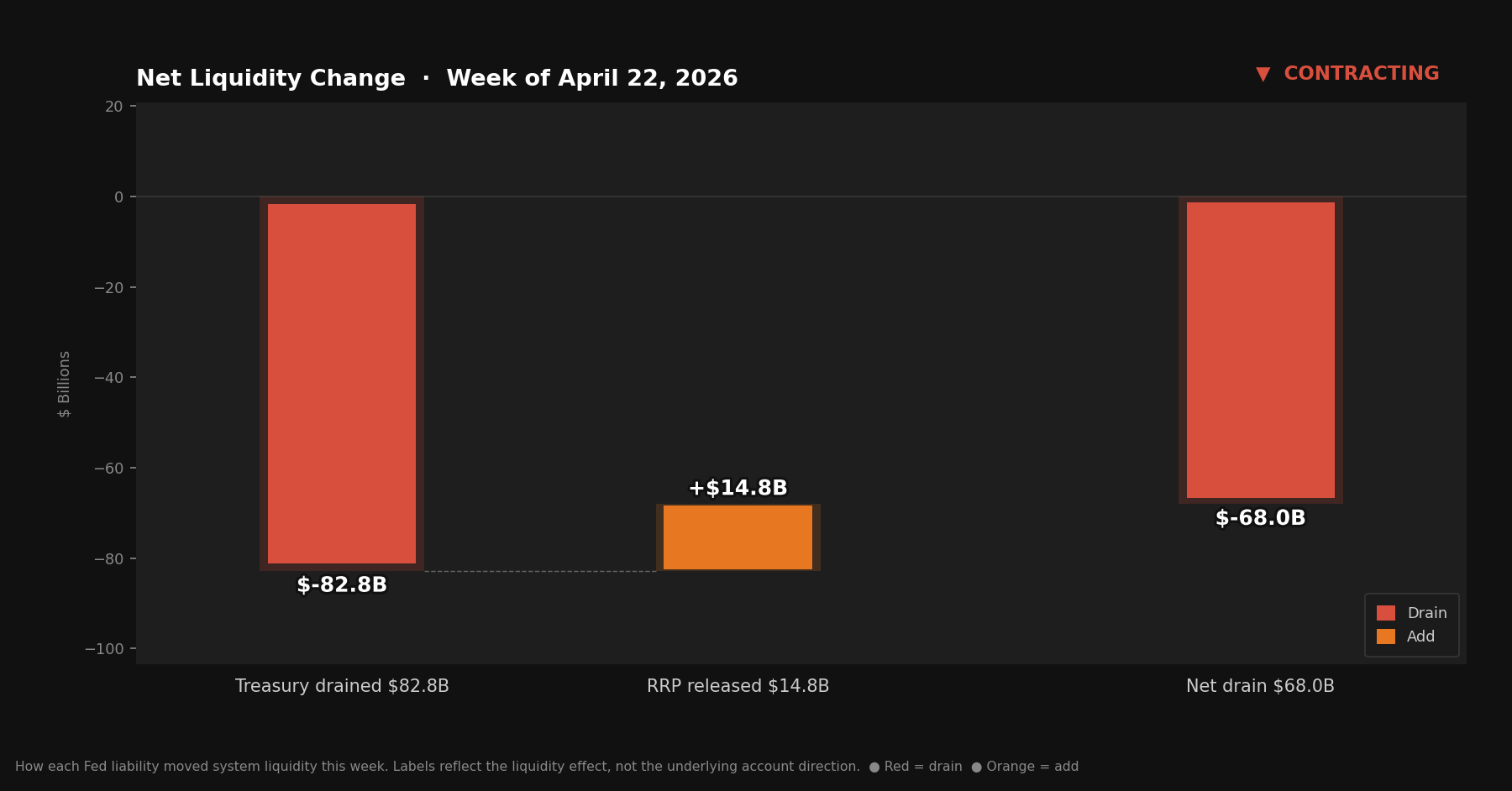

Primary Driver: The Treasury General Account rose another $82.8B this week, crossing the $1 trillion threshold for the first time in this series. Reserves fell $65.6B in response.

Implication: Contraction continued — though at a fraction of last week’s pace. The TGA at $1.007 trillion is an even larger loaded spring. Every dollar in that account represents future liquidity waiting to be released. The timing of Treasury drawdowns — not necessarily Fed action — will determine when conditions shift.

What Actually Happened

Last week’s $227.3 billion TGA surge was the kind of move that dominates the picture. This week looks quieter by comparison.

But quiet is relative. The TGA rose another $82.8 billion.

That pushed it above $1 trillion — to $1.007 trillion as of Wednesday.

To put that in context: this series began tracking when the TGA was well below $400 billion. In the span of two weeks, it has added over $310 billion and crossed a threshold that is, if nothing else, a number most people instinctively notice.

Reserves fell $65.6 billion — a more moderate decline than last week’s $203.3 billion, but directionally consistent. The system continued to tighten.

The RRP fell $14.7 billion. Money market funds withdrew slightly from their Fed parking accounts, pushing a small amount of cash back into circulation. This partially offset the TGA-driven drain — but only partially. The net effect was a liquidity contraction of approximately $68 billion.

Net liquidity in the financial system, combining Treasury cash balances and reverse repo usage.

The Mechanics, Briefly

For anyone following for the first time:

Reserve balances are what commercial banks hold at the Fed — the banking system’s collective checking account. When reserves fall, banks have less capacity to lend and invest freely, independent of any change in the Fed’s policy rate.

The TGA is the government’s bank account at the Fed. Tax receipts flow in; spending flows out. It moves inversely to reserves — when the TGA rises, reserves fall; when the TGA falls, reserves rise. They sit at opposite ends of the same seesaw.

The RRP is an overnight facility where money market funds earn a yield by parking cash at the Fed. Money sitting in the RRP is not circulating as reserves.

This week: $82.8 billion into the TGA. $14.7 billion out of the RRP. $65.6 billion out of reserves.

Reserve Balances and the Treasury General Account move inversely — when Treasury refills its account, reserves drain, and vice versa.

The Trillion-Dollar Account

There is something clarifying about a round number.

A $1 trillion TGA does not mean anything different, mechanically, than a $999 billion TGA. The seesaw still works the same way. The reserve dynamics are unchanged. But it is the kind of figure that stops you for a moment and asks you to register what you are actually looking at.

The federal government is holding over one trillion dollars in its checking account at the Federal Reserve.

That cash is sitting completely outside the banking system. It is not earning interest. It is not being lent. It is not circulating. It exists as a claim — a very large one — that will eventually be converted into spending. When it does, the flow runs in reverse: the TGA declines, reserves rise, and the banking system receives an injection of liquidity it does not currently have.

The question of when has not changed from last week. The debt ceiling situation continues to constrain Treasury’s ability to issue new securities, which means the existing cash pile becomes the operating fund. Defense appropriations, entitlement payments, and routine government operations will begin drawing it down. The pace at which that happens will determine whether the next several weeks look contractionary or expansionary.

What is clear is that the reservoir is larger than it was last week. And the larger the reservoir, the more significant the eventual release.

What Did Not Happen

The Fed did not expand its balance sheet. No emergency lending. No new facilities. No policy change.

The contraction this week — and last week — is entirely fiscal in origin. The Treasury collected taxes, built its cash balance, and the banking system’s reserves contracted as a direct consequence. The Fed was a passive observer.

This is a distinction worth holding. When reserves fall because the Fed is actively reducing its balance sheet, the mechanism is monetary policy. When reserves fall because the TGA is rising, the mechanism is fiscal plumbing. Both produce the same result on bank reserve balances. But they have different drivers, different reversal dynamics, and different implications for what comes next.

The Fed has not tightened. The Treasury has been accumulating. Those are different stories, even when they appear in the same number.

The Bitcoin Lens

The TGA just crossed $1 trillion.

That trillion dollars represents the purchasing power of tax payments collected from millions of people and businesses — workers, small companies, corporations — flowing into a government account where it sits, inert, until it is allocated and spent. The mechanism that produced this is not controversial or dramatic. It is routine. It happens every April.

But routine does not mean unimportant. The ebb and flow of these balances shapes the liquidity conditions that move through the entire financial system — lending rates, credit availability, asset prices — without a press conference, without a vote, without a headline.

Bitcoin sits outside this cycle — and not just this week’s. The TGA will drain, refill, and drain again. Reserves will rise and fall with each turn of the seesaw. RRP balances will shift. And across every one of those movements, the aggregate supply of dollars in the system has a directional bias: it grows. That is what the architecture produces — more dollars, more cycles, more seesawing — over time and over decades.

Bitcoin’s supply does not respond to any of it. The issuance is fixed and tapering. The total will never exceed 21 million. The number that mattered this week was $1.007 trillion in a government account. That number will keep changing. The other one will not.

The H.4.1 report is released every Thursday by the Federal Reserve. This series tracks the three figures that matter most: reserve balances, the TGA, and reverse repo — and explains what their movements mean for financial conditions.