Fed Liquidity Watch // Issue #12

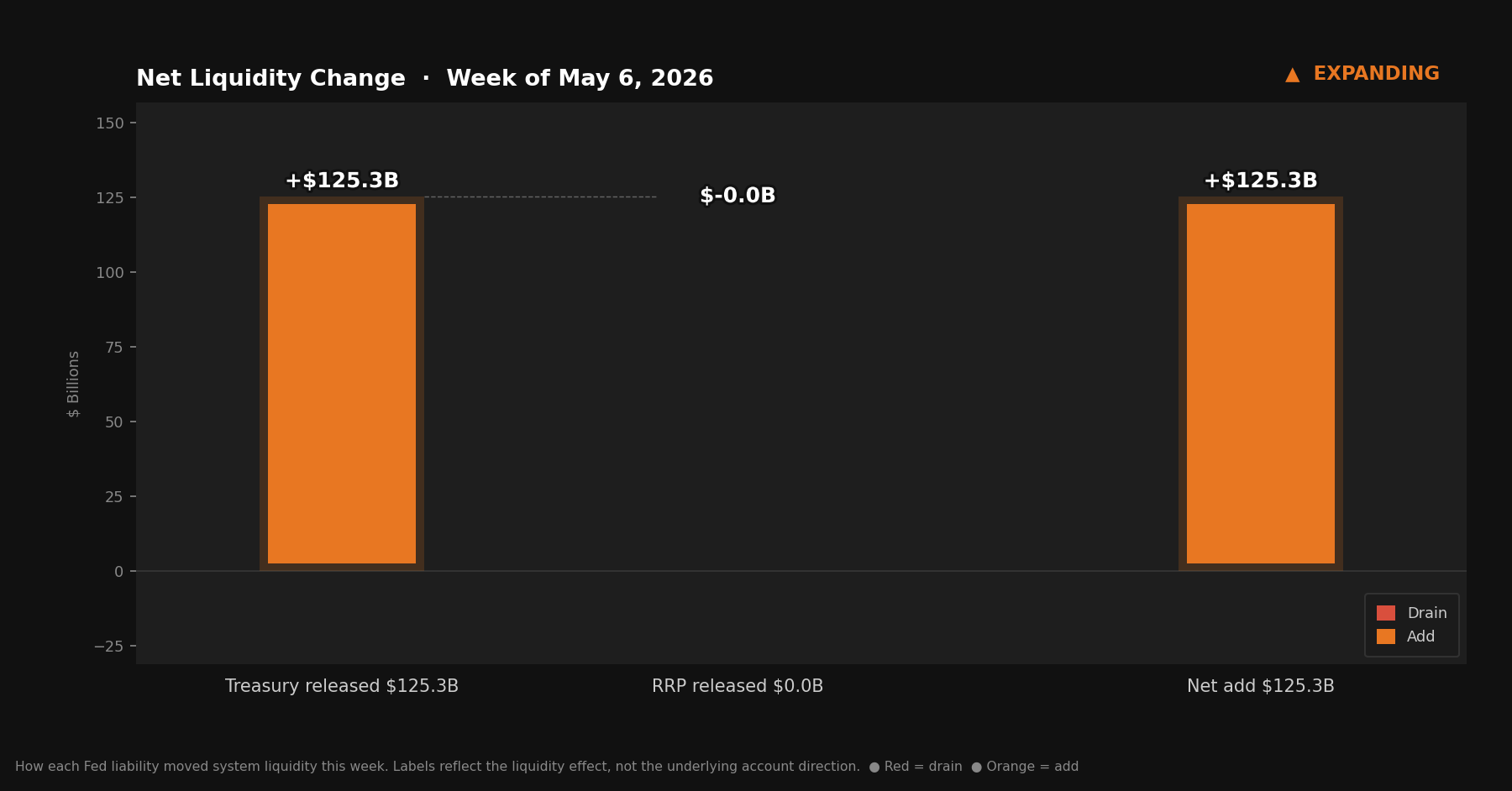

The TGA shed $125.3 billion in a single week — its steepest drawdown since the April peak. Reserves crossed $3 trillion for the first time in this series. The cycle that contracted sharply in April is

Issue #11 covered the first step down: a $19.1 billion TGA drawdown, modest but directional. The reservoir had started to drain.

This week, the drain opened up.

Quick Update — Week of May 6, 2026

Three rows from Table 1, Wednesday column:

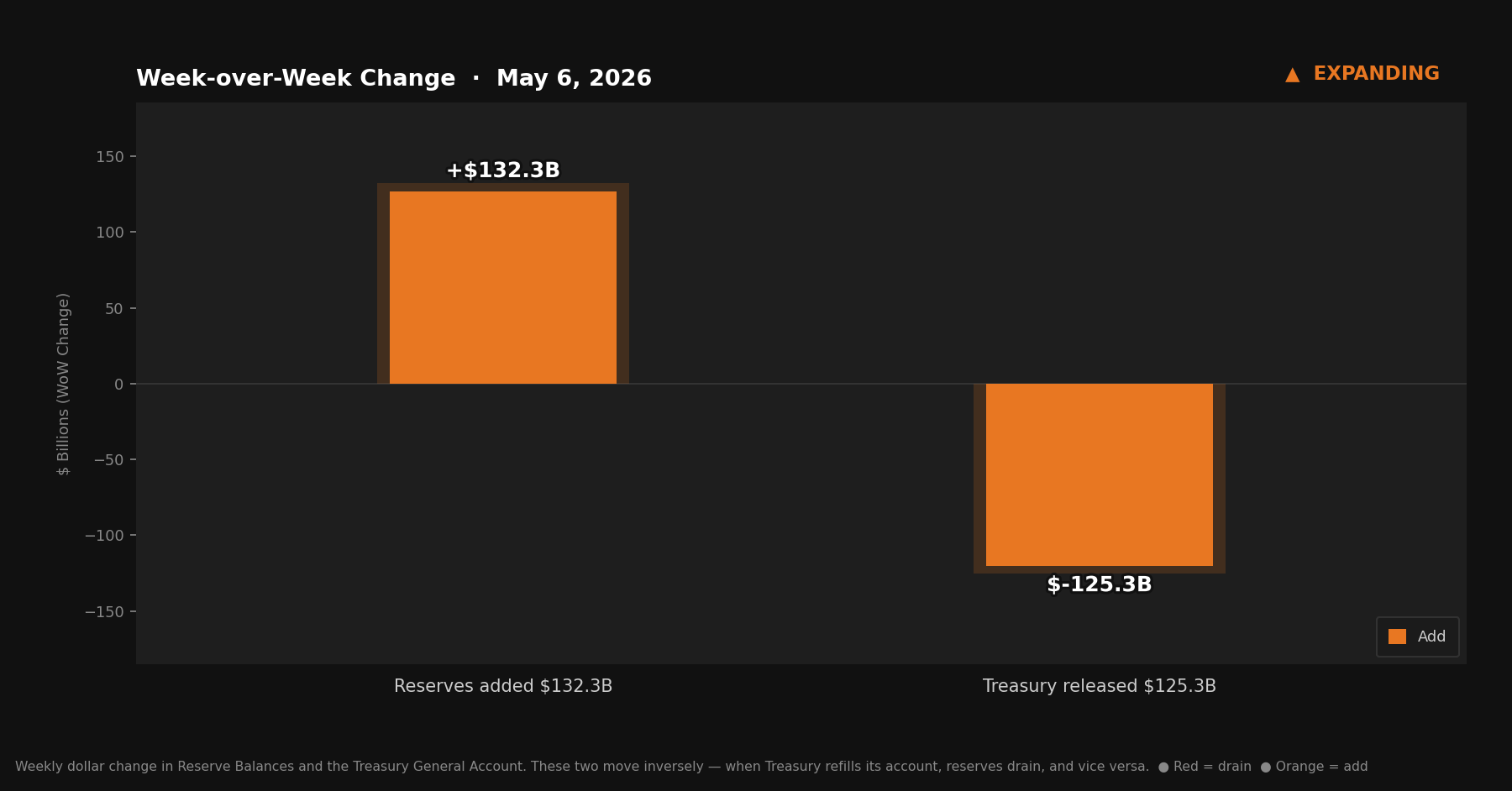

Reserve balances with Federal Reserve Banks: $3,051.5B — up $132.3B from last week

U.S. Treasury General Account (TGA): $862.8B — down $125.3B from last week

Reverse repurchase agreements (RRP): $322.7B — unchanged from last week

Liquidity Signal — Week of May 6, 2026

Direction: Expanding

Primary Driver: The TGA dropped $125.3 billion in a single week — the steepest drawdown since the April peak. Reserves surged $132.3 billion in response, crossing $3 trillion for the first time in this series.

Implication: What took three weeks to accumulate is unwinding fast. The liquidity contraction driven by the April tax surge is reversing with significant force. Reserves crossing $3T is not a footnote — it marks the banking system’s deepest reserve position in recent memory.

What Actually Happened

Last week the TGA sat at $988.1 billion — still elevated, still close to the $1.007 trillion peak it hit the week prior. The first step of the drawdown had been modest. $19 billion. A signal, not a flood.

This week: $125.3 billion out.

The TGA fell from $988.1B to $862.8B in a single Wednesday-to-Wednesday window. To put that in context, the entire three-week buildup from the April tax surge added roughly $310 billion to the TGA. This week’s drawdown erased about 40% of that accumulation in one week.

On the other side of the ledger, reserves jumped $132.3 billion — from $2,919.2B to $3,051.5B. Reserve balances at Federal Reserve banks now sit above $3 trillion for the first time in this series.

The RRP barely moved. A rounding-difference change. The TGA was the entire story this week.

Net liquidity in the financial system, combining Treasury cash balances and reverse repo usage.

The Mechanics, Briefly

For anyone joining for the first time:

Reserve balances are what commercial banks hold at the Fed — the banking system’s collective checking account. When reserves rise, banks have more room to lend and invest. When reserves fall, that capacity tightens.

The TGA is the federal government’s checking account at the Fed. Tax receipts flow in; spending flows out. When Treasury spends, money leaves its account and lands as reserves in the banking system. The two accounts sit at opposite ends of the same seesaw — one goes down, the other goes up.

The RRP is an overnight facility where money market funds park cash at the Fed. Dollars sitting there are not in circulation.

This week: $125.3 billion drained from the TGA. Reserves rose $132.3 billion — slightly more than the TGA drawdown, meaning other Fed balance sheet movements contributed an additional ~$7 billion on top of the fiscal flow. One account contracted sharply; the other expanded sharply.

Reserve Balances and the Treasury General Account move inversely — when Treasury refills its account, reserves drain, and vice versa.

The TGA’s climb from under $700B to $1.007T over three weeks was one of the more dramatic liquidity-draining sequences in this series. The mechanism was entirely fiscal: April tax receipts pouring into the government’s account, pulling reserves out of the banking system in the process.

The drawdown is now reversing with a magnitude that mirrors the accumulation.

A $125.3 billion single-week TGA decline is not routine. The government doesn’t decide to spend $125 billion in a week as a policy choice — this is the mechanical consequence of normal operations pressing against a constrained borrowing environment. With the debt ceiling still binding, Treasury is managing its cash balance carefully, deploying it for required spending while it can’t refill through new issuance at normal volumes.

The result is a concentrated, fast drawdown. And when the TGA drains fast, reserves build fast. That’s what happened this week.

Crossing $3 Trillion

Reserves at $3,051.5B is worth pausing on.

Three weeks ago, when the TGA was peaking, reserves fell to around $2,400B — a level that represented genuine tightening in available banking-system liquidity. The April surge had drained roughly $500 billion worth of reserve capacity at its worst point.

This week’s reading represents a near-complete recovery of that contraction, and then some. At $3.051T, reserves are meaningfully above where they were before April’s tax season began. The liquidity that was temporarily extracted from the banking system has not only returned — it has returned at an amplified level.

The pace of this matters. A $132 billion single-week reserve increase is a significant injection by any historical measure. It doesn’t represent a Fed action; the Fed’s balance sheet didn’t change. This is the fiscal plumbing operating exactly as designed — government spending flows out to the private sector, landing as reserves. The question going forward is how long the TGA drawdown continues at this pace, and whether it moderates or accelerates as the debt ceiling situation evolves.

What Didn’t Move

The Fed remained passive throughout. No policy change, no balance sheet adjustment, nothing from the FOMC.

This continues to be the defining context for this series: the most significant movements in reserve balances are happening entirely on the fiscal side. Tax season built the TGA up. Government spending is bringing it back down. The Fed is watching.

The distinction between monetary and fiscal drivers of liquidity matters practically. When coverage focuses on Fed decisions — rate meetings, balance sheet programs — it misses the mechanism that’s been doing most of the work in this cycle. The plumbing underneath those decisions is running on its own schedule.

The Bitcoin Lens

$125 billion left the Treasury’s account this week and flowed into the banking system. Reserves crossed $3 trillion. The cycle that accumulates and then releases is working exactly as designed.

The interesting question isn’t whether this week’s number is large or small. It’s what the cumulative picture looks like after years of these cycles — accumulate, spend, accumulate, spend — each iteration leaving behind a slightly larger total monetary base than before. The tools that manage this process are all denominated in the same expanding unit.

Bitcoin’s supply doesn’t respond to this cycle. It doesn’t expand when the TGA drains. It doesn’t contract when tax season tightens reserves. Whatever gets released into the banking system this week, the 21 million stays exactly what it was.

The reservoir opened this week. The cycle continues.

The H.4.1 report is released every Thursday by the Federal Reserve. This series tracks the three figures that matter most: reserve balances, the TGA, and reverse repo — and explains what their movements mean for financial conditions.