Fed Liquidity Watch // Issue #4

The Treasury Spent. Reserves Breathed.

The Weekly H.4.1 Breakdown / March 12, 2026 Release

The report arrives the same way it always does.

Thursday at 4:30 PM. No announcement. No context. Just eleven pages of tables that most of the financial world ignores.

This week, if you scrolled to reserve balances, you found something different from what was seen in February.

Reserves didn’t fall.

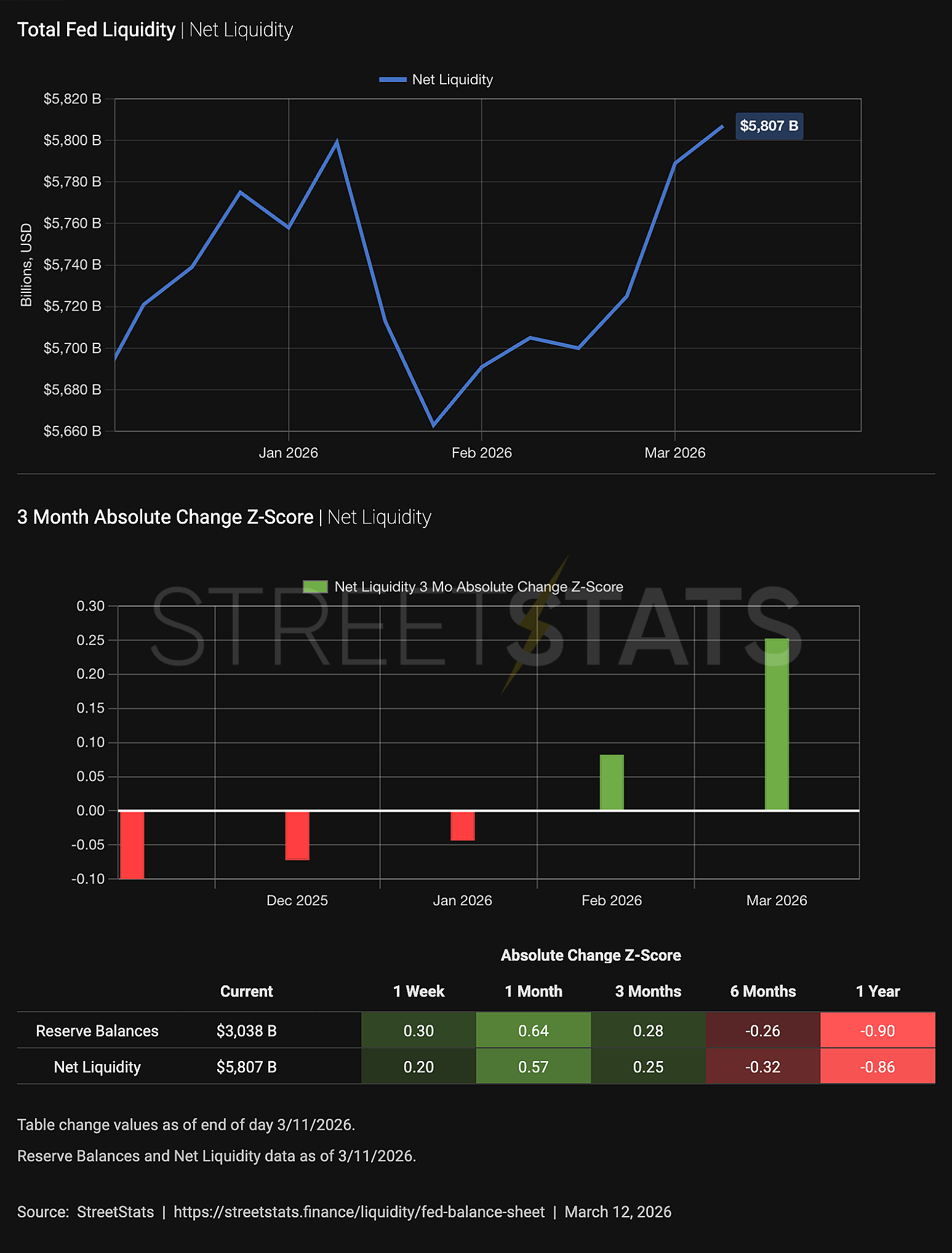

They rose — by $59.4 billion — to $3.073 trillion on Wednesday.

That’s worth understanding, because not long ago, the story was the opposite.

A Quick Recap

Issue #1 of this series covered the January 29th release. That week, reserves fell sharply — dropping $53.3 billion to $2.90 trillion — as the Treasury rebuilt its cash account at the Federal Reserve, pulling money out of the banking system in the process.

The lesson then was straightforward: the direction of the Treasury General Account matters as much as anything on the asset side of the balance sheet.

This week delivered the same lesson from the other direction.

Liquidity Signal — This Week

Direction: Expanding

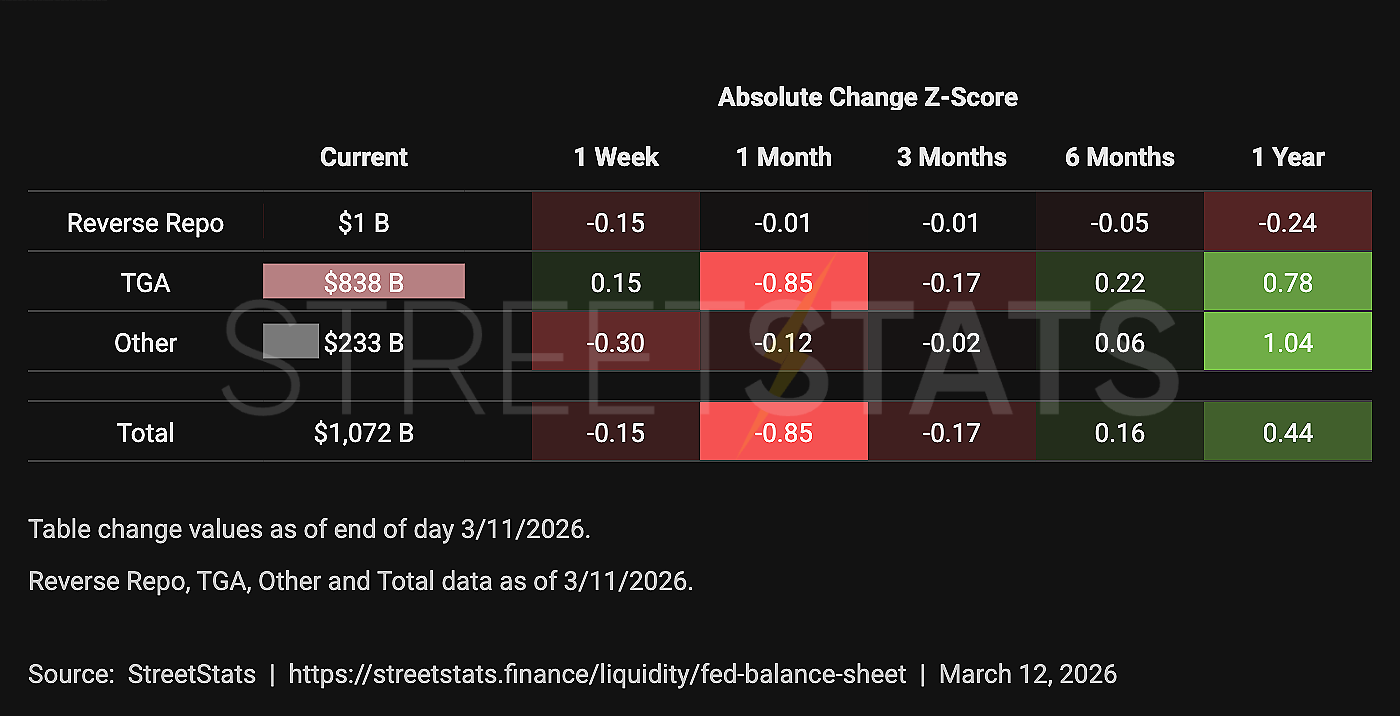

Primary Driver: TGA drawdown of $41.2B pushed cash into the banking system, lifting reserve balances by $59.4B on a Wednesday-to-Wednesday basis. RRP rose $6.0B, providing a partial offset.

Implication: Near-term liquidity conditions improved modestly this week. The TGA-to-reserves transmission worked in the direction of expansion. Watch whether continued Treasury spending sustains reserve growth, or whether a TGA rebuild reverses this week’s gains.

What Actually Happened This Week

Start with the three numbers that matter.

Reserve balances with Federal Reserve Banks came in at $3.073 trillion on Wednesday, up $59.4 billion from the prior Wednesday’s $3.014 trillion. That’s a meaningful single-week increase, and to understand it, you have to look at where it came from.

The TGA fell $41.2 billion — from $847.0 billion the prior Wednesday to $805.8 billion this week. When Treasury cash leaves its account at the Fed and flows into the economy as spending, that money finds its way into bank deposits, and those deposits settle as reserve balances at the Federal Reserve. Reserves rise. That’s the transmission mechanism, and it’s exactly what drove this week’s increase.

Reverse repurchase agreements (RRP) moved in the other direction, rising $6.0 billion from $319.5 billion to $325.5 billion. RRP agreements remove liquidity from the banking system — when money managers park cash overnight at the Fed in exchange for Treasuries, those funds leave reserves. So the $6.0 billion RRP increase partially offset the TGA-driven addition.

The net effect: a large Treasury drawdown pushed reserves higher, and a small RRP increase took a modest portion of that back. Liquidity conditions loosened on the week.

Net liquidity in the financial system, combining the Fed balance sheet, Treasury cash balances, and reverse repo usage

The Mechanics, Explained Simply

The Federal Reserve’s balance sheet works differently from what most people expect when they hear “Fed policy.”

Interest rate decisions get the headlines. But reserve balances are the plumbing — the actual level of liquid funds circulating through the banking system. And the plumbing is driven as much by Treasury activity as by anything the Fed does directly.

When the TGA falls, it means the Treasury is spending — paying federal contractors, disbursing transfer payments, covering debt obligations. Those dollars leave the Treasury’s account at the Fed and flow outward into the economy. They land in bank accounts. Those banks hold reserve balances at the Fed. Reserves rise.

The reverse is equally true. When the Treasury collects taxes or issues new debt, its account at the Fed grows. That cash gets pulled out of the banking system and sits at the Fed earning nothing. Reserves fall. We watched this happen in January, when the TGA rebuilt sharply and reserves dropped $53.3 billion in a single week.

This week, the Treasury was a net spender. That made reserves rise. Not because the Fed did anything dramatic — but because the plumbing did what it was designed to do.

The Asset Side

On the asset side, total Reserve Bank credit increased $15.4 billion on a weekly average basis, driven almost entirely by growth in Treasury bill holdings.

Bills rose to $358.8 billion on Wednesday — an increase consistent with the ongoing Reserve Management Purchase program, through which the Fed replaces a portion of maturing mortgage-backed securities with short-term Treasuries. MBS balances were essentially unchanged on the week, continuing their slow structural runoff from the QE era.

This bill-buying program is not stimulus in the traditional sense. It is stabilization — a way to prevent the balance sheet from contracting faster than reserve conditions can comfortably absorb. It runs in the background, quiet and consistent, and it has been a floor under the balance sheet for months.

Key liabilities on the Fed’s balance sheet that influence system liquidity

What Did Not Happen

Worth noting what the data does not show.

Primary credit — borrowing from the Fed’s discount window — remained small and essentially unchanged. No banks were seeking emergency funding. No swap lines surged. No new lending facilities were activated.

This was ordinary plumbing. Treasury cash moved through the system in the normal course of government operations. Reserves responded. The system absorbed the flows without friction or stress.

Mechanics matter. And when the mechanics are calm, that itself is information.

The Bigger Picture

One week does not define a trend. But context helps.

When this series launched in January, reserves had just dropped to $2.90 trillion after the TGA rebuilt sharply. The question at the time was whether Treasury-driven drains would persist and push reserves into uncomfortably tight territory.

Seven weeks later, reserves sit at $3.073 trillion. The TGA, which was rebuilt aggressively in January, has since declined as the government continued to spend. That decline has been a steady source of reserve creation — the same mechanism that drained reserves in January is now working in reverse.

The RRP facility, meanwhile, sits at $325.5 billion. A year ago on the same date it held $529.0 billion. That structural decline has been ongoing for some time, and it has an important implication: the large liquidity buffer that once existed in overnight reverse repo is largely gone. The system no longer has a reservoir of idle RRP cash that can flow back into reserves when needed. Reserve conditions are now more sensitive to TGA movements than at any point in recent memory — which makes the weekly Treasury cash swing more consequential than it used to be.

This week, that swing went in the right direction.

The Bitcoin Lens

Fed liquidity is not the only factor shaping how Bitcoin moves. Global credit conditions, China’s monetary cycle, dollar funding dynamics — all of these play a role over time.

But reserve balances anchor the domestic system. When they contract meaningfully, risk assets tend to feel it. When they expand, financial conditions breathe a little easier.

This week, they breathed easier.

That’s not a prediction. It doesn’t mean a breakout is imminent or that the liquidity backdrop has structurally turned. A single week of Treasury spending doesn’t establish a new regime. But directional data matters, and the direction this week was different from January.

Bitcoin exists precisely because its supply cannot expand to meet new liquidity. As conditions shift week by week — sometimes loosening, sometimes tightening — that structural reality doesn’t change. But it does mean that when new liquidity enters the system, Bitcoin is one of the places it has historically found a home.

The Regime as of March 11, 2026

Reserve Management Purchases continue, supporting bill holdings.

MBS runoff continues at a slow, structural pace.

TGA fell $41.2 billion — Treasury cash flowed into the banking system.

RRP rose modestly to $325.5 billion.

Reserve balances rose $59.4 billion to $3.073 trillion.

No stress.

No drama.

Just movement.

And movement in liquidity precedes movement in markets.

Why This Exists

Every Thursday at 4:30 PM ET, the Federal Reserve publishes this report.

Most people will never open it.

But three numbers — reserves, TGA, and reverse repo — tell you more about the state of financial conditions than most of the commentary that follows. This series exists to read those numbers clearly, every week, in plain language, without the noise.

Next week, we look again.

Because liquidity regimes don’t announce themselves.

They reveal themselves.