Fed Liquidity Watch // Issue #5

Reserves fell $74B this week. The calendar explains most of it — but the year-over-year trend is worth watching.

Week of March 18, 2026

Every week, the Federal Reserve publishes a report called the H.4.1 — a dense table of numbers that most people never see. Inside it are three figures that tell you more about the direction of global financial conditions than almost anything else you’ll read in the financial press. This is a plain-language breakdown of what those numbers said this week.

Quick Update

The H.4.1 report for the week ending March 18, 2026 tells a clean story: the Treasury collected, and the banking system felt it.

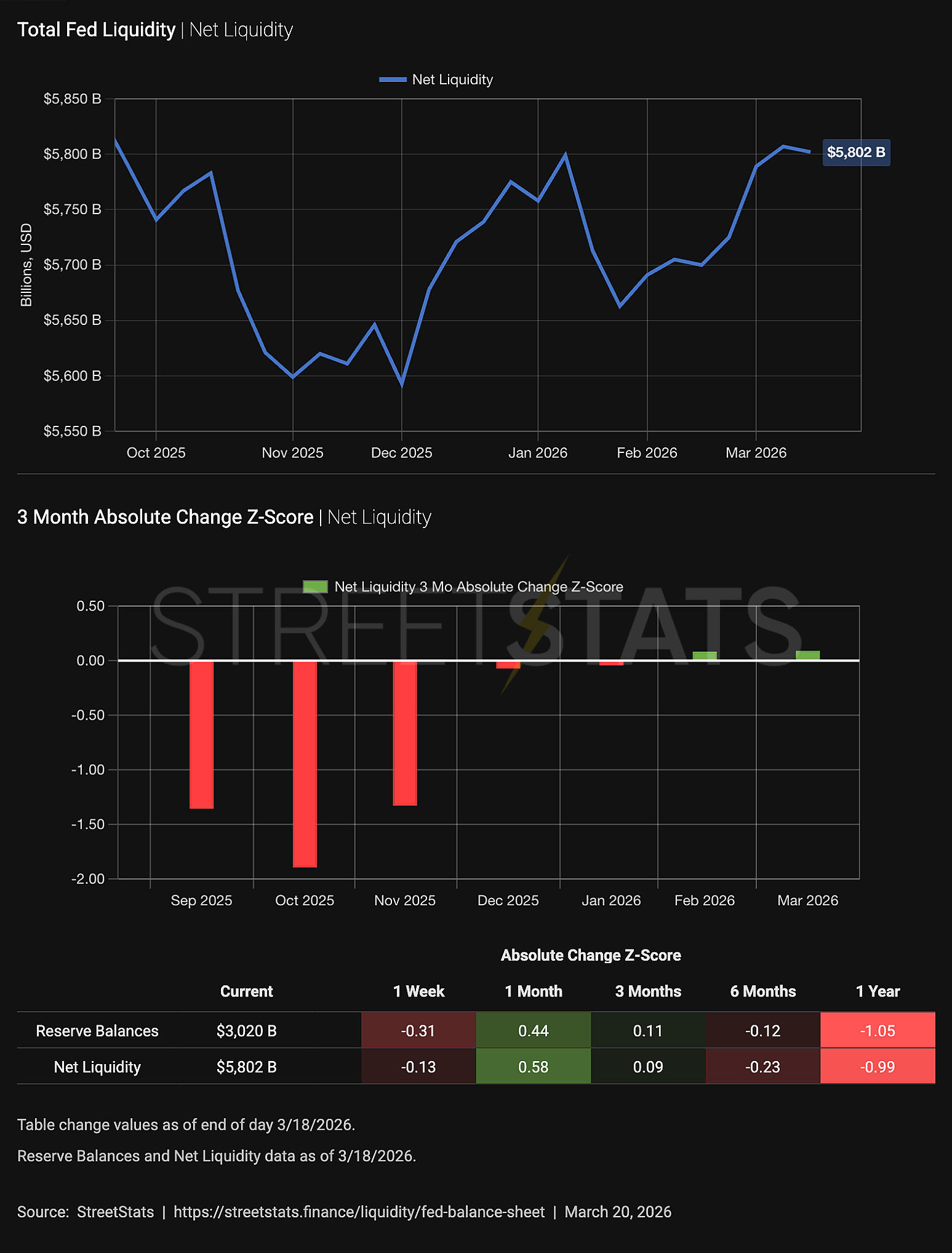

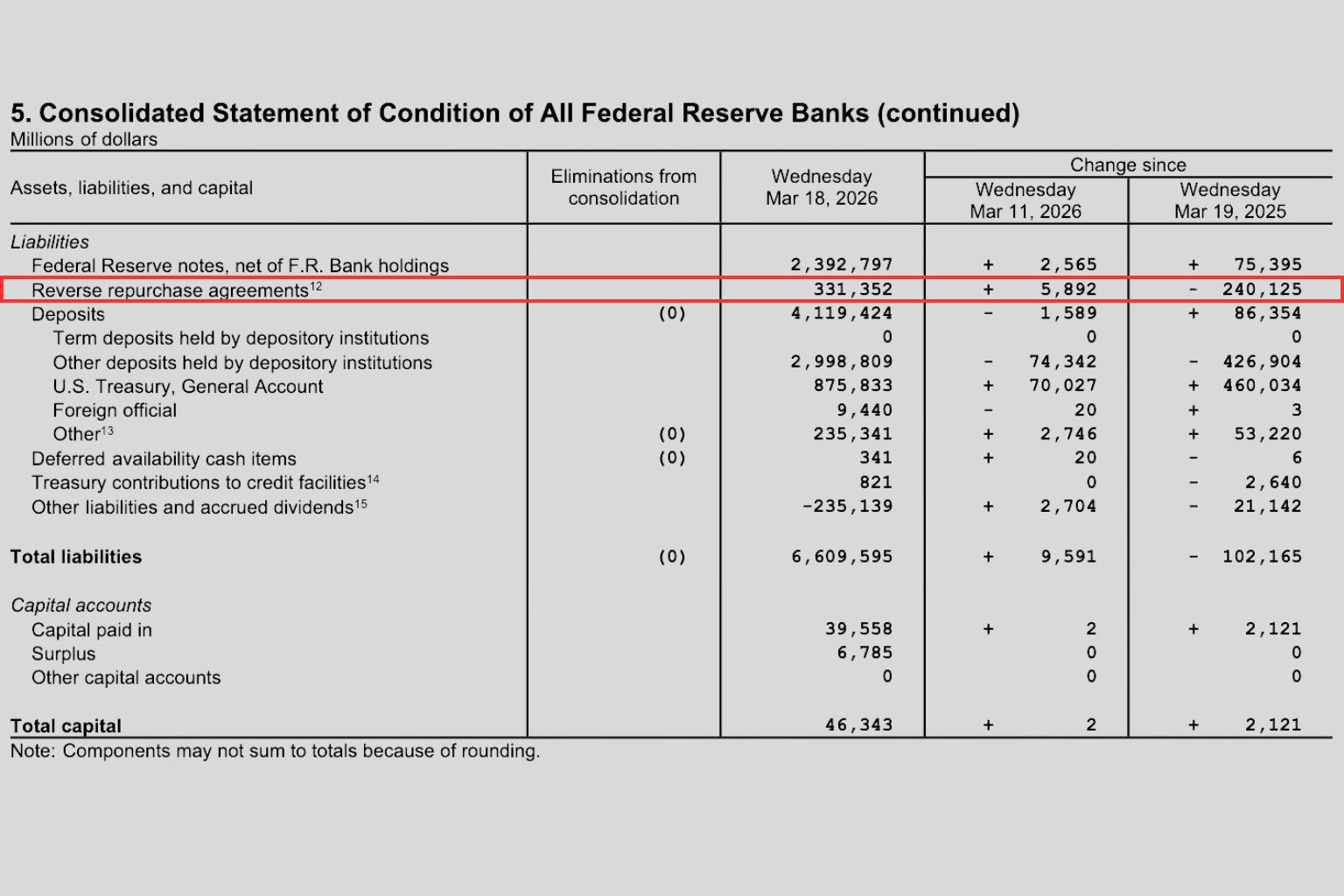

Reserve balances — the money commercial banks hold on deposit at the Federal Reserve — fell to $2.999T, down $74.3B from last week’s $3.073T. At the same time, the U.S. Treasury’s General Account (TGA) surged to $875.8B, up $70.0B from $805.8B the prior week. Reverse repurchase agreements (RRP) ticked up modestly to $331.4B from $325.5B, a gain of $5.9B.

All three figures moved in the same direction: tighter.

Liquidity Signal — Week of March 18, 2026

Direction: Contracting

Primary Driver: TGA surge of +$70.0B pulled reserves sharply lower — consistent with quarterly tax payment inflows

Implication: Mechanical seasonal drain; watch for reversal over the coming weeks as government spending flows back into the system

Net liquidity in the financial system, combining the Fed balance sheet, Treasury cash balances, and reverse repo usage.

The Mechanics: What Actually Happened

The connection between a rising TGA and falling reserves is worth understanding, because it happens every quarter and most people don’t realize they’re looking at the same event from two sides of the same ledger.

When money flows into the Treasury’s General Account — through tax payments, bond auction proceeds, or other government receipts — it effectively leaves the banking system. The same dollar cannot simultaneously sit in a bank’s reserve account at the Fed and in the Treasury’s account at the Fed.

So when the TGA rises, reserve balances fall by a corresponding amount. This week: TGA up $70.0B, reserves down $74.3B. The math nearly squares.

The timing is the tell. The middle of March is when quarterly estimated tax payments are due. Businesses, self-employed workers, and individuals with significant non-wage income all file and pay in the same window. For the week of March 18, that seasonal effect shows up precisely where you’d expect it on the balance sheet. This isn’t a policy decision by the Federal Reserve. It’s a calendar.

The slight uptick in RRP usage — up $5.9B — is consistent with the overall picture. When reserves thin out and banks and money market funds have less cash to deploy elsewhere, they tend to park more of it overnight at the Fed through the reverse repo facility. The move is small, but it points in the same direction as everything else this week.

Why It Might Not Last

A TGA surge driven by tax receipts is not the same as a structural shift in liquidity conditions. The Treasury doesn’t accumulate money permanently — it spends it. As government payments flow back out over the coming weeks (salaries, contracts, social programs, interest on the debt), that cash re-enters the banking system and replenishes reserves. This cycle repeats every quarter around tax deadlines.

The more meaningful question for liquidity watchers is whether the TGA rise is entirely seasonal or whether the Treasury is building a larger cash balance ahead of something — significant debt issuance, a policy announcement, or fiscal uncertainty that warrants holding more cash than usual.

For now, the simplest interpretation is the right one: tax season pulled liquidity toward Washington for a week. The money will work its way back out.

The Year-Over-Year View

Zoom out from the week-over-week noise, and the longer picture looks different.

Compared to March 2025, reserve balances are down $447.8B. The TGA is up $417.1B. RRP is down $189.9B year-over-year. The year-over-year signal is that reserves have been contracting steadily over a longer time horizon, while the Treasury has been holding more cash than it did a year ago.

This matters because the level of reserves determines how sensitive the financial system is to any given shock. Abundant reserves absorb disruptions without much market impact. Tighter reserves mean less buffer — the same TGA surge or repo stress that barely registers in a liquid environment can amplify quickly when the cushion has been eroded.

We’re not at crisis levels. But the trajectory over the past twelve months points toward a system with less room for error than it had a year ago.

What This Means for Bitcoin

Bitcoin doesn’t have a quarterly tax payment cycle. It doesn’t have a General Account. It doesn’t have a fiscal calendar that causes its supply to contract in mid-March and expand again in April.

What it has is a supply that cannot respond to any of these pressures. At all.

The global liquidity cycle turns constantly — tax seasons, debt ceiling negotiations, refunding announcements, emergency facilities opened and closed. All of these move reserves, TGA, and RRP week to week. Bitcoin observes all of it from the outside. Its supply doesn’t contract when the Treasury collects taxes and doesn’t expand when the government spends. The number of bitcoin that will ever exist was set in 2009. Whatever new supply entered circulation between March 2025 and March 2026 did so on a schedule written in code — indifferent to tax season, the debt ceiling, or any decision made in Washington.

When liquidity conditions loosen and capital searches for places to go, Bitcoin absorbs some of it — not because anyone is directing it there, but because a fixed-supply asset in an expanding monetary system is structurally in the path of that flow. When conditions tighten, Bitcoin prices feel the pressure like any other risk asset in the short run.

But the supply itself doesn’t change. The weekly H.4.1 can compress reserves, drain liquidity, and tighten conditions — and Bitcoin remains exactly as scarce as it was the week before.

That’s the asymmetry this series is built to track.