Fed Liquidity Watch // Issue #8 - Weekly H.4.1 Breakdown

Why Bank Reserves Just Jumped $119 Billion (And What It Means for April)

The Weekly H.4.1 Breakdown

Issue #8 — April 9, 2026 Release

Every Thursday, the Federal Reserve publishes a document most people have never heard of.

It’s called the H.4.1. Eleven pages of dense tables. No charts, no commentary, no headlines. Just numbers that describe the plumbing of the entire financial system.

Last week, I noted that April’s tax season would likely push the Treasury’s cash account higher and drain reserves in the process. That’s the standard April pattern — and it’s reliable enough to be worth flagging in advance.

This week, the opposite happened. Dramatically.

The TGA didn’t rise. It plunged. And reserves jumped by the largest single-week amount I’ve tracked in this series.

Here’s what the numbers actually say.

Quick Update — Week of April 9, 2026

Three rows from Table 1, Wednesday column:

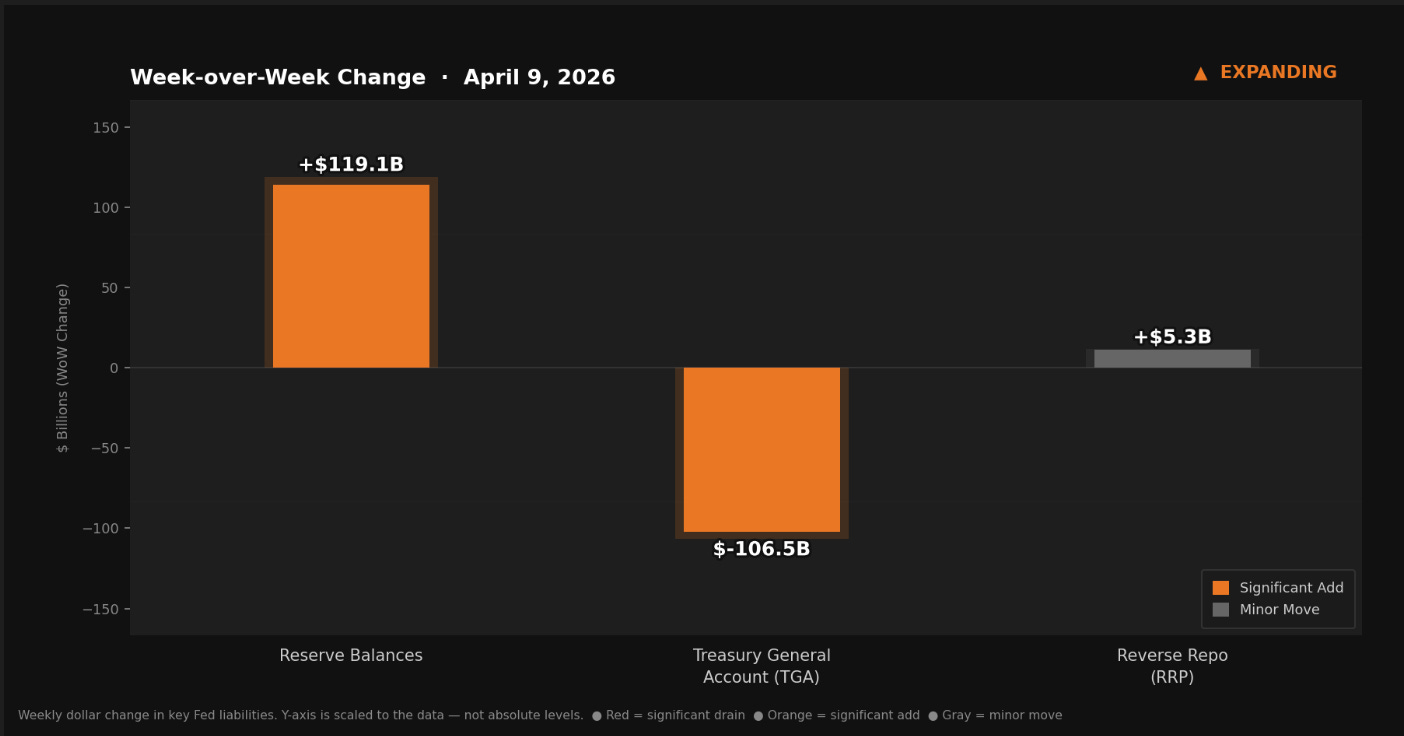

Reserve balances with Federal Reserve Banks: $3,183.5B — up $119.1B from last week

U.S. Treasury General Account (TGA): $697.1B — down $106.5B from last week

Reverse repurchase agreements (RRP): $344.9B — up $5.3B from last week

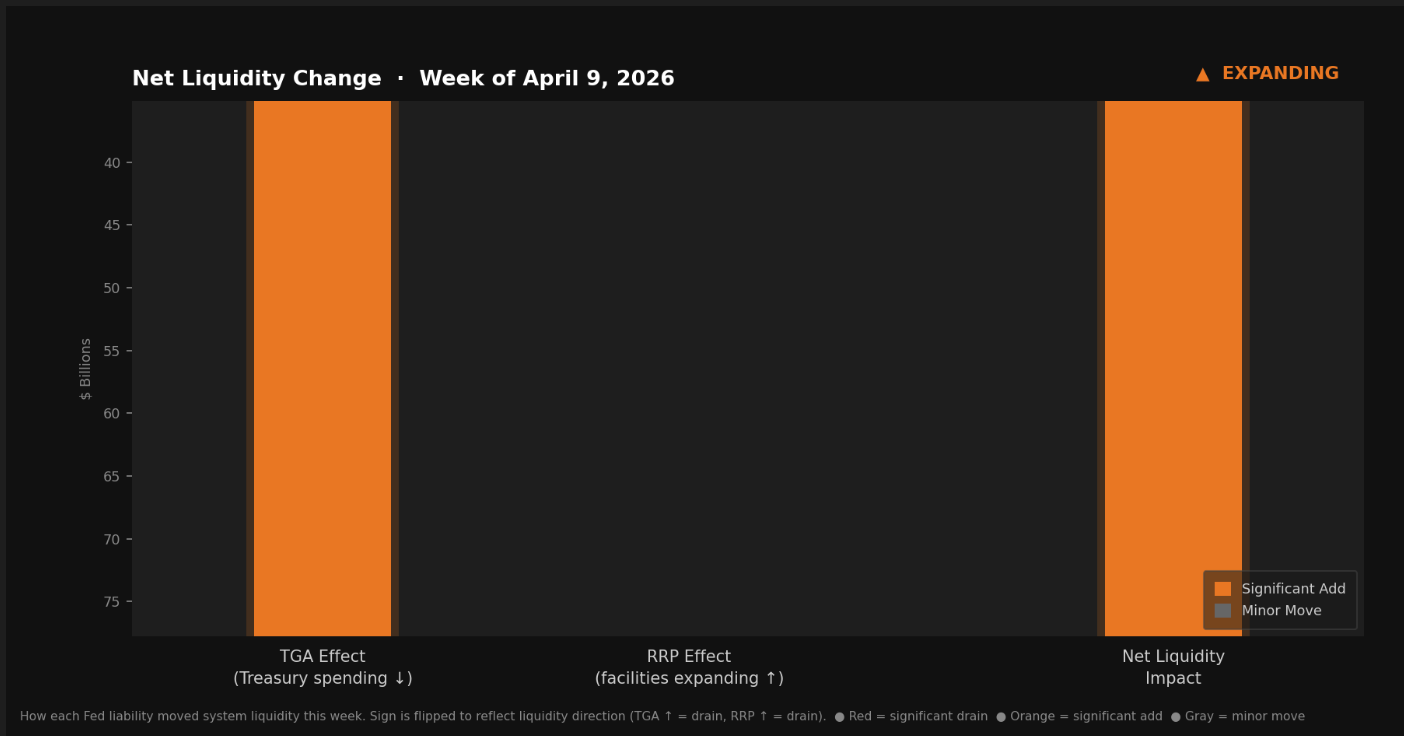

Liquidity Signal — Week of April 9, 2026

Direction: Expanding

Primary Driver: The Treasury General Account dropped $106.5B in a single week — its largest weekly decline in this series — releasing reserves into the banking system on a massive scale.

Implication: Liquidity conditions improved sharply this week. The size and direction of the TGA move during what should be peak tax-receipt season is unusual. If spending is simply outpacing early receipts, the calendar may assert itself in the weeks ahead with a hard reversal. Watch the TGA closely.

What Actually Happened

Start with the number that tells the story.

The Treasury’s General Account — the U.S. government’s operating cash account held at the Federal Reserve — fell $106.5 billion in a single week.

That is not a small move. Last week’s issue flagged a $33.9 billion TGA decline and called it meaningful. This week was three times that size.

When the TGA falls, the government is spending cash out of its account and into the broader economy. That money flows into the bank accounts of whoever received it — contractors, agencies, beneficiaries — which in turn shows up as higher reserve balances at the Federal Reserve.

That is exactly what happened.

Reserves rose $119.1 billion.

The accounting is directionally clean. The TGA shed $106.5 billion. Reverse repo absorbed a modest $5.3 billion of that inflow. Other balance sheet factors account for the remainder, and reserves landed $119.1 billion higher on the week. The Treasury spent. Banks received. Reserves expanded — at scale.

Net liquidity in the financial system, combining the Fed balance sheet, Treasury cash balances, and reverse repo usage.

The Mechanics Behind the Number

Three levers control reserve balances. Understanding each one is the difference between seeing the headlines and understanding the story.

Reserve balances are the funds that commercial banks hold at the Federal Reserve — the banking system’s collective checking account. When this number rises, banks have more capacity to lend, invest, and support the broader economy. When it falls, conditions tighten, even if the Fed hasn’t changed policy rates.

The Treasury General Account (TGA) is the U.S. government’s operational bank account, also held at the Fed. When the government collects taxes or issues new debt, the TGA rises. When it spends, the TGA falls. The critical point: TGA movements are a direct counterweight to reserve balances. Every dollar that leaves the TGA enters the banking system as reserves. Every dollar that enters the TGA is pulled out of reserves. The Treasury is effectively a massive liquidity valve — and this week it moved hard.

Reverse repurchase agreements (RRP) are overnight parking accounts where financial institutions — primarily money market funds — deposit cash with the Fed in exchange for a small amount of interest. Money sitting in the RRP is money not circulating as reserves. This week, RRP balances rose a modest $5.3 billion, absorbing a small portion of the TGA-released liquidity before it could reach reserve balances in full.

The net picture: $106.5 billion out of the TGA, $5.3 billion into the RRP, and $119.1 billion into reserves — with other balance sheet movements accounting for the difference.

Key liabilities on the Fed’s balance sheet that influence system liquidity.

The April Paradox

Here is the part worth sitting with.

Last week’s note flagged April as tax season — a period when the TGA historically swells as receipts arrive from individuals, corporations, and trusts, pulling reserves out of the banking system. That pattern is real and repeats reliably. It was worth flagging.

This week ran the opposite direction by a wide margin.

Two explanations are worth holding simultaneously.

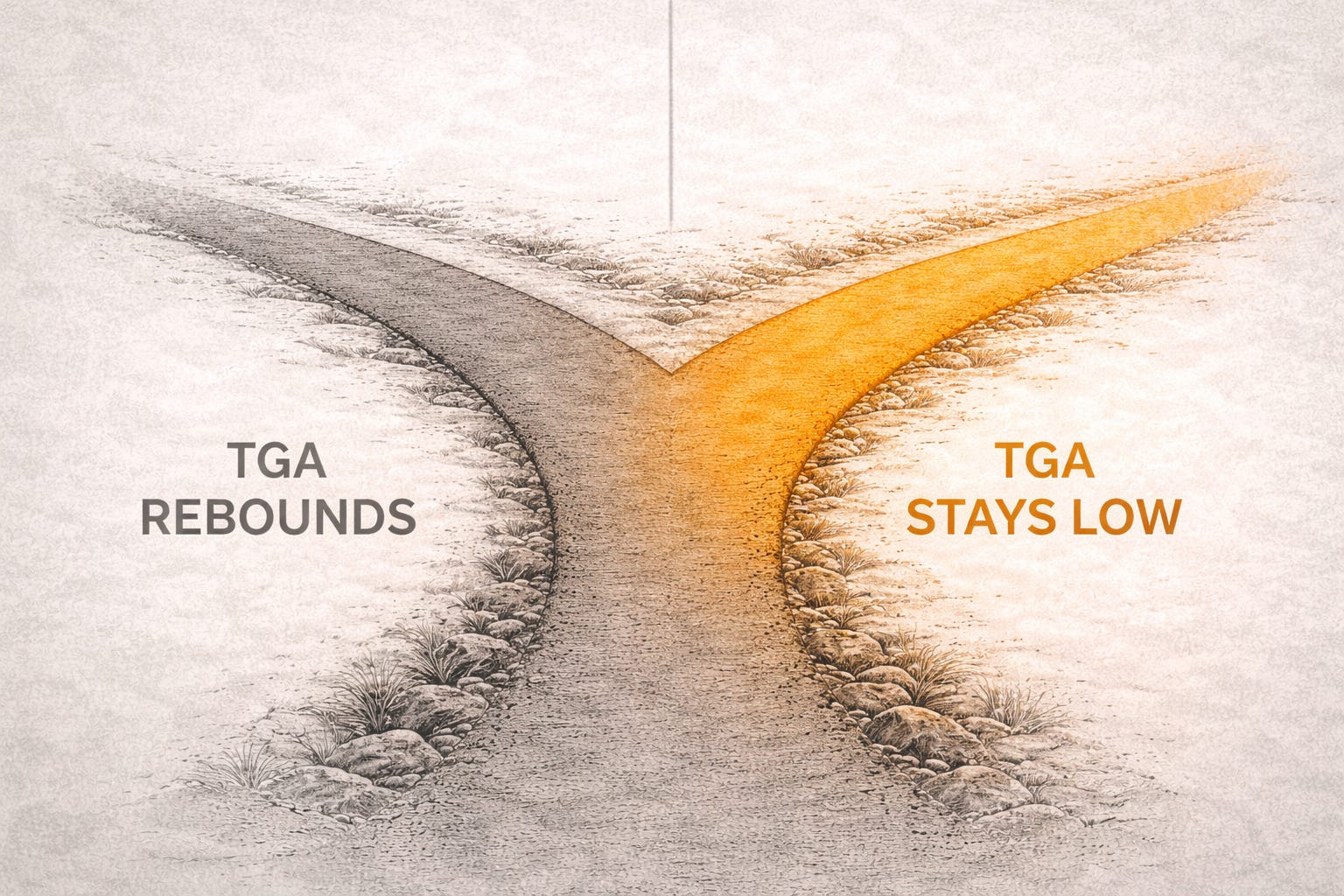

The first is timing. The bulk of April tax receipts typically arrive in the second and third weeks of the month, not the first. It’s possible what we’re seeing is normal government spending hitting the system before the big receipt wave has arrived. In that reading, the TGA decline this week is temporary, and a significant rebound is still coming — one that will pull reserves back down just as fast as they rose.

The second is magnitude. Even if that rebound comes, the TGA would need to climb steeply from its current $697.1 billion to offset this week’s drop. A week ago, the TGA stood at $803.6 billion. Two weeks ago, it was $837.4 billion. The starting point for any tax-season rebuild is lower than the calendar would suggest, which could compress how much the subsequent tightening actually bites.

One of two things is about to happen. Either April receipts arrive in force, the TGA begins climbing rapidly, and reserves get pulled back down — tightening conditions quickly and potentially sharply. Or the drawdown continues, and liquidity conditions stay supportive into mid-month. Both readings have implications for how risk assets behave over the next few weeks.

There is a third factor worth naming. The United States is currently 40 days into a military operation against Iran. Estimated direct costs have run approximately $45 billion — roughly $1 billion per day in munitions, naval operations, and logistics. The Pentagon has reportedly requested an additional $200 billion supplemental on top of that, and the White House has proposed a $1.5 trillion defense budget for next year, the largest proposed year-over-year increase since World War II. A ceasefire was announced on April 7, but the fiscal machinery it set in motion does not stop when the guns pause. War spending flows through the same plumbing as any other government spending. When the Defense Department pays contractors, reimburses allies, or restocks depleted munitions inventories, those dollars leave the TGA and enter the banking system as reserves. The war isn’t the whole story this week. But it is part of the accounting — and it is not a small part.

This week’s direction was clearly positive. The question now is whether April tax receipts, war spending dynamics, and the broader fiscal trajectory add up to a reversal or a continuation in the weeks ahead.

What Did Not Happen

No spike in emergency lending.

No surge in primary credit borrowing from the Fed.

No reactivation of crisis facilities.

No stealth balance sheet expansion.

What happened this week was fiscal plumbing — the government spending at an unusual pace, releasing reserves into the banking system as it does every time it spends. Most financial commentary this week will not mention this. The people who track it tend to be ahead of the people who don’t.

The Bitcoin Lens

A $119 billion single-week reserve increase is the kind of move that matters for liquidity-sensitive assets.

Fed liquidity is one input. Global liquidity is the fuller picture — China’s credit cycle, dollar funding conditions, and cross-border capital flows all shape the environment. But domestic reserve balances anchor the U.S. banking system, and they have a consistent relationship with risk appetite. When reserves expand persistently, the conditions for risk assets tend to improve. When they contract, the opposite tends to follow.

This week, they expanded — sharply.

One week is still one data point. The pattern that matters is what happens over the next three weeks as April receipts either arrive in force or don’t. If the TGA stays suppressed, this becomes a genuine liquidity tailwind. If it rebounds steeply, the move reverses just as fast.

Bitcoin absorbs liquidity over time because its supply cannot expand to meet demand. Every additional dollar created by the global monetary system — through deficit spending, through bank lending, through the fiscal dynamics on display this week — has exactly 21 million bitcoins available to absorb it. That number does not change based on what the Treasury’s calendar does in April.

It also does not change based on what happens in Iran. A $1.5 trillion proposed defense budget — the largest year-over-year increase since World War II — represents a sustained fiscal expansion that will flow through this same plumbing for years, not weeks. If that spending materializes at scale, it will add trillions in liquidity to the global financial system over the course of a decade. The supply of bitcoin will not respond.

What changes week to week is the rate at which that liquidity is flowing. This week, it flowed with unusual force.

The H.4.1 report is released every Thursday afternoon by the Federal Reserve. This series tracks the three figures that matter most: reserve balances, the TGA, and reverse repo — and explains what their movements mean for financial conditions.