Fed Liquidity Watch // Issue #9 - Weekly H.4.1 Breakdown

The TGA surged $227 billion as April tax receipts rolled in. Reserves dropped $203 billion. And now the Treasury is sitting on $924 billion it will eventually spend back out.

April 16, 2026 Release

Last week’s issue ended with a watch: one of two things was about to happen. Either April tax receipts would arrive in force, the TGA would climb rapidly, and reserves would fall just as fast as they had risen — or the drawdown would continue and liquidity conditions would stay supportive into mid-month.

The verdict is in.

Tax season arrived. With force.

Here’s what the numbers say.

Quick Update — Week of April 16, 2026

Three rows from Table 1, Wednesday column:

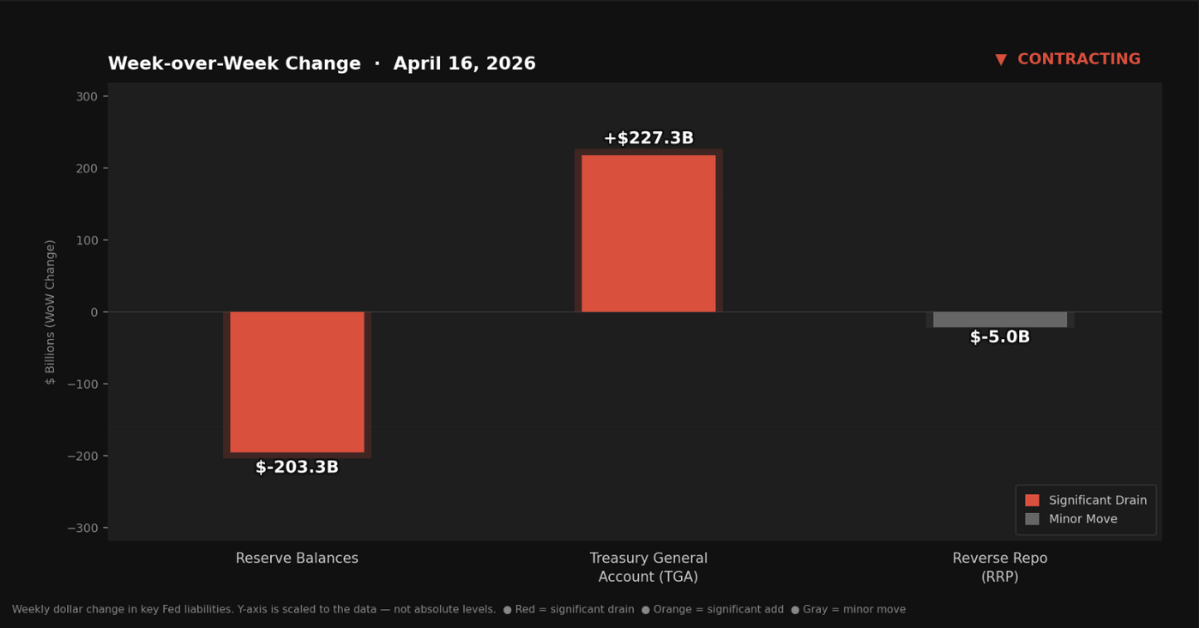

Reserve balances with Federal Reserve Banks: $2,980.2B — down $203.3B from last week

U.S. Treasury General Account (TGA): $924.4B — up $227.3B from last week

Reverse repurchase agreements (RRP): $339.9B — down $5.0B from last week

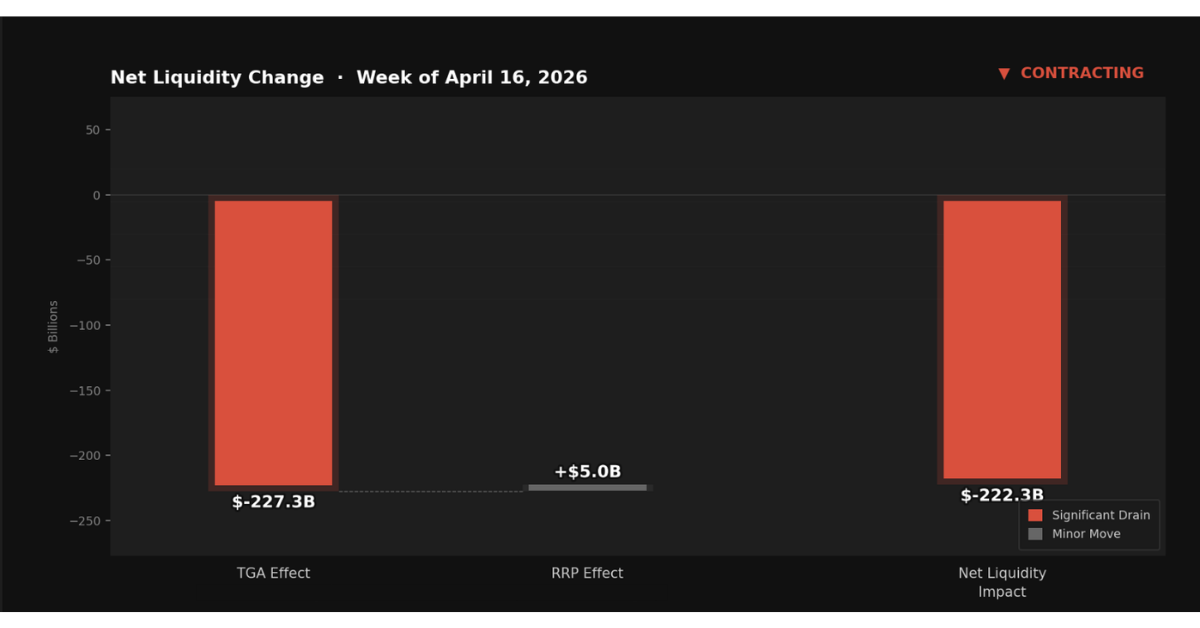

Liquidity Signal — Week of April 16, 2026

Direction: Contracting

Primary Driver: The Treasury General Account surged $227.3B in a single week as April tax receipts arrived in full force, pulling $203.3B out of reserve balances.

Implication: Last week’s sharp expansion reversed almost entirely. The tax season correction flagged in Issue #8 arrived — and arrived large. The TGA now sits at $924.4B, well above its recent range. How quickly and heavily the Treasury spends that down will determine whether the next few weeks bring a resumption of expansion or continued tightening.

What Actually Happened

The call from last week held.

Issue #8 noted that April tax receipts typically arrive in the second and third weeks of the month — and that if they came in full force, the TGA would rebuild sharply and reserves would fall just as fast. That is precisely what happened.

The TGA rose $227.3 billion in a single week.

That is not a routine swing. To put it in context: the largest single-week TGA increase previously tracked in this series was $33.9 billion. This week was nearly seven times that size.

Where did that $227.3 billion come from? Tax receipts — corporations, individuals, and trusts filing their April returns. The flow runs in the opposite direction from last week: instead of the Treasury spending cash into the banking system, the banking system paid into the Treasury. Every tax payment reduces a bank deposit somewhere in the economy, which reduces bank reserves at the Fed.

Reserves fell $203.3 billion.

The RRP absorbed almost nothing — it fell $5.0 billion, meaning money market funds actually moved slightly out of their Fed parking accounts rather than into them. The full brunt of the liquidity drain hit reserves directly.

Net liquidity in the financial system, combining the Fed balance sheet, Treasury cash balances, and reverse repo usage.

The Mechanics, Briefly

For anyone following for the first time: the three numbers in this series are a simplified read on domestic financial plumbing.

Reserve balances are what commercial banks hold at the Fed — the banking system’s collective checking account. When this number falls, banks have less capacity to lend and invest freely, even if the Fed’s policy rate hasn’t moved an inch.

The TGA is the U.S. government’s bank account at the Fed. Tax receipts go in; spending comes out. It is an inverse counterweight to reserves — when the TGA rises, reserves fall; when the TGA falls, reserves rise. The two move like opposite ends of a seesaw.

The RRP is an overnight parking facility where money market funds earn a small yield by depositing cash at the Fed. Money sitting in the RRP is not actively circulating as reserves.

This week: $227.3 billion into the TGA. $5.0 billion out of the RRP. $203.3 billion out of reserves. Other balance sheet factors account for the remainder.

Key liabilities on the Fed’s balance sheet that influence system liquidity.

The Reservoir Is Full

The TGA now sits at $924.4 billion.

That is the highest level in this series. It is also, in a sense, stored potential energy. That cash does not earn interest sitting in a government account at the Fed. It will be spent. The question is the rate and the timing.

When the Treasury spends, the TGA falls and reserves rise. That is the same dynamic that produced last week’s $119 billion reserve surge — and the same dynamic that produced the large TGA drawdowns tracked throughout this series. The longer the TGA sits elevated, the more compressed the release will be when spending resumes.

A few threads worth watching:

The defense spending trajectory flagged in Issue #8 has not changed. A proposed $1.5 trillion defense budget represents sustained future fiscal outflows. When that spending flows through the TGA — paying contractors, restocking munitions, funding operations — reserves will rise. Not as monetary expansion. As fiscal mechanics.

The debt ceiling trajectory also matters. When the Treasury is constrained from issuing new debt, it draws down its cash account to fund operations, releasing reserves. When the constraint lifts and Treasury refills the TGA by issuing new bills and bonds, it drains reserves again. A TGA at $924.4 billion means the government has significant operating runway — but it also means a substantial drawdown cycle is likely ahead.

The direction this week is clearly contractionary. Whether it sustains depends on how quickly the Treasury begins deploying the cash it just collected.

What Did Not Happen

No emergency lending. No primary credit spike. No reactivation of crisis facilities. No balance sheet expansion by the Fed.

What happened this week was entirely fiscal — the normal tax collection mechanism pulling $227 billion out of the banking system in a single week. The Fed’s own balance sheet barely moved.

That matters because the story told in most financial commentary will not mention any of this. The reserve drawdown will go unnoted. The TGA sitting at a record high will go unexamined. The implications for liquidity conditions in the weeks ahead will go unexplained.

The people who track these numbers tend to be a few steps ahead of the people who don’t.

The Bitcoin Lens

One week of sharp expansion followed by one week of sharp contraction.

What you’re watching is the ebb and flow of fiscal liquidity — the government spending in one week, collecting in another, with reserves rising and falling as the tides shift. The individual weeks matter less than the direction over time. And the direction over time is more spending, more debt issuance, more money flowing through the system — because that is what the long-run fiscal trajectory demands.

The TGA sitting at $924.4 billion is not a ceiling. It is a reservoir. At some point, it flows back out. When it does, reserves will rise again — and the conditions that tend to benefit liquidity-sensitive assets will reassert.

The supply of bitcoin does not respond to any of this. Not to the April receipt wave. Not to the TGA level. Not to whatever the next drawdown looks like. Not to the defense budget proposal sitting in Congress. Twenty-one million. That number is the same this week as it was last week, and it will be the same when the reservoir eventually drains.

The system creates the liquidity. Bitcoin exists to absorb it.

The H.4.1 report is released every Thursday by the Federal Reserve. This series tracks the three figures that matter most: reserve balances, the TGA, and reverse repo — and explains what their movements mean for financial conditions.