H.4.1 Liquidity Watch // Issue #16

The Fed's Overnight Parking Facility Just Absorbed $25 Billion — Here's What That Means for Reserves

The Weekly H.4.1 Breakdown

Issue #16 — June 3, 2026

Last week, the TGA refilled $60.7 billion and drove the contracting signal. This week the TGA barely moved — $3.0 billion.

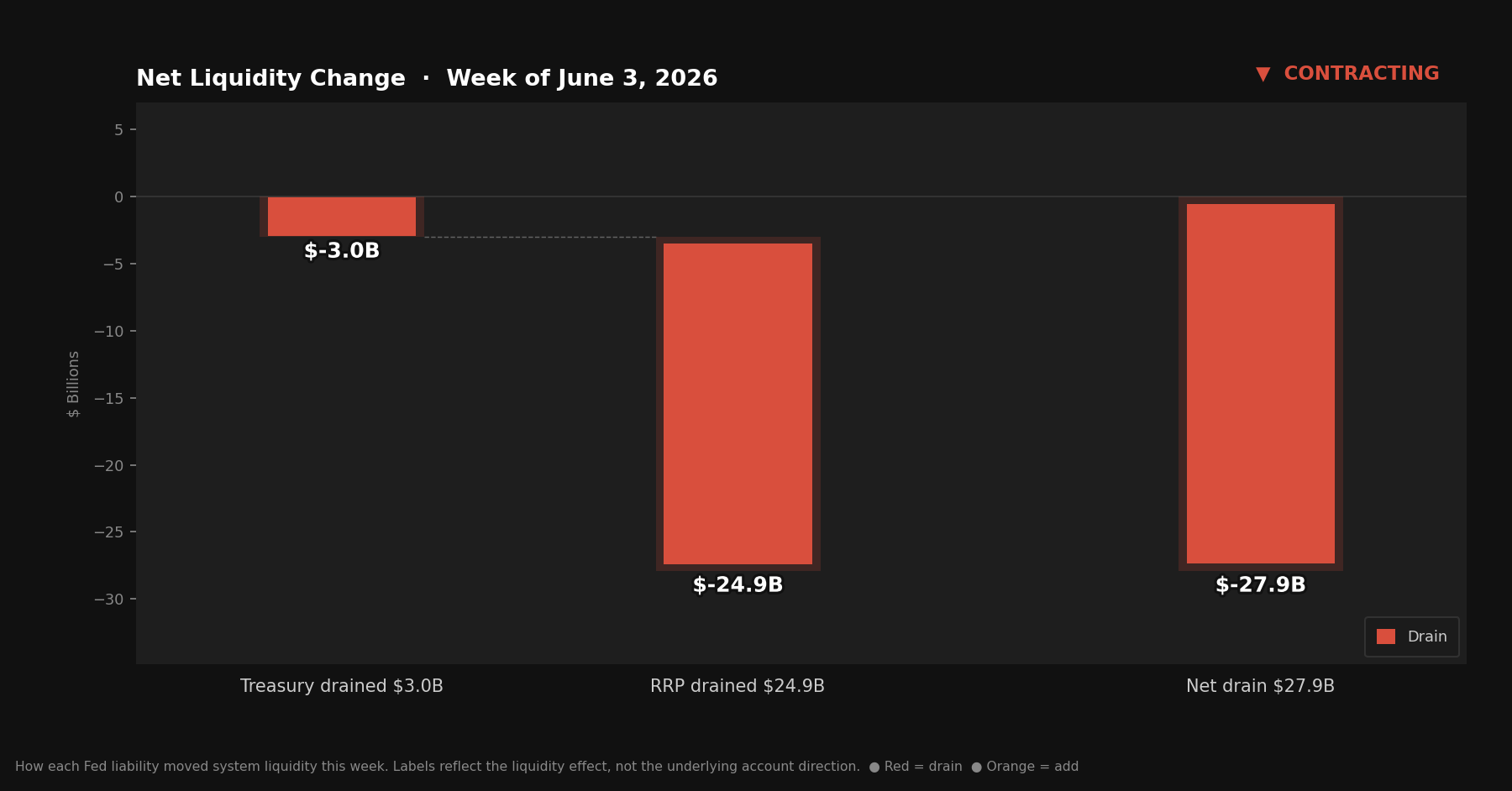

The contracting signal came anyway. The RRP pulled $24.9 billion out of circulation instead.

Three consecutive contracting signals now. The driver has shifted from fiscal to money market, but the direction hasn’t changed.

Quick Update — Week ending June 3, 2026

Four rows from Table 1, Wednesday column:

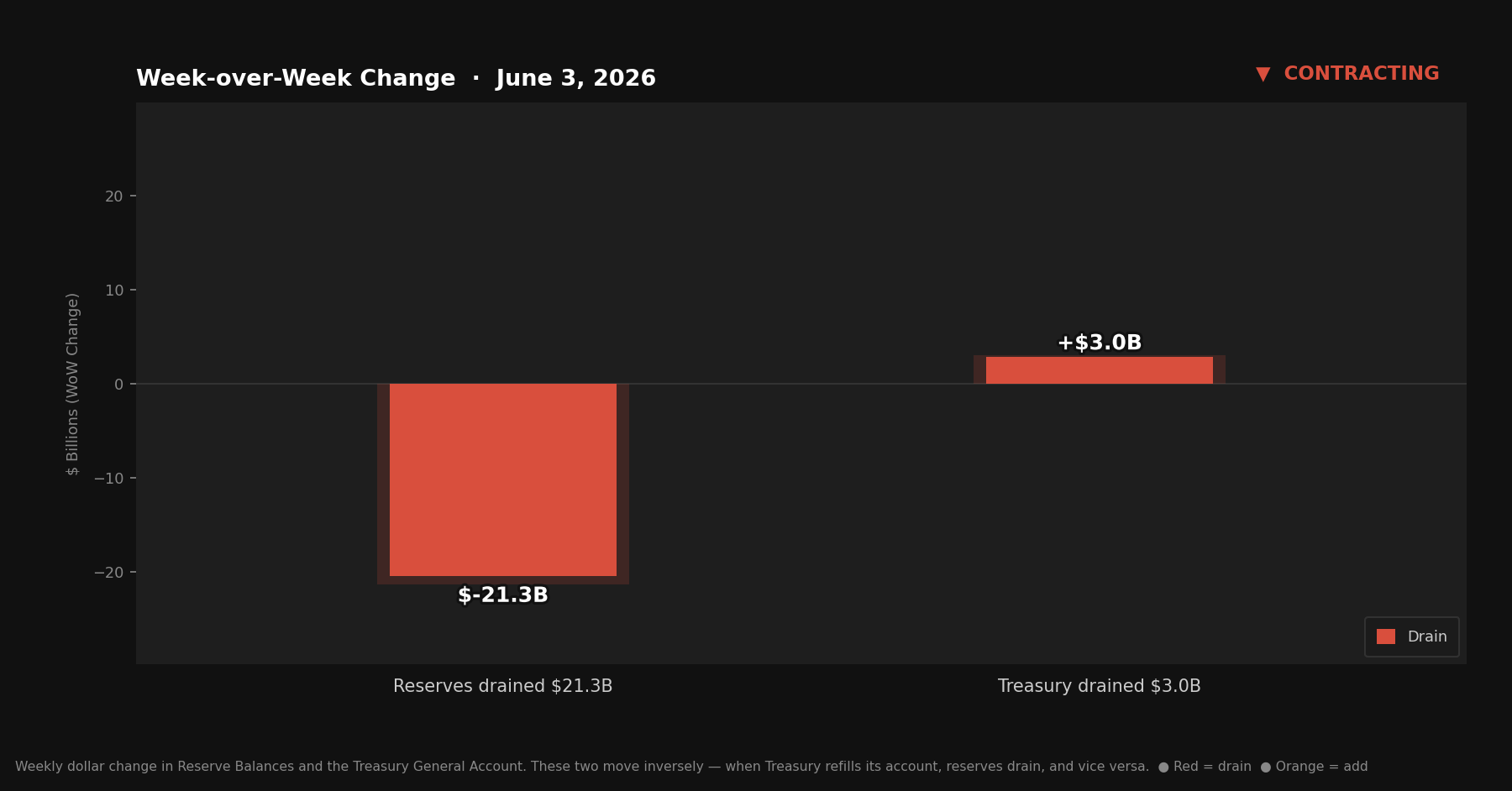

Reserve balances with Federal Reserve Banks: $3,045.7B — down $21.3B from last week

U.S. Treasury General Account (TGA): $845.7B — up $3.0B from last week

Reverse repurchase agreements (RRP): $325.8B — up $24.9B from last week

Central bank liquidity swaps: $0.1B — unchanged from last week (Near zero. No signal.)

Liquidity Signal — Week ending June 3, 2026

Direction: Contracting

Primary Driver: RRP surged $24.9B — money market funds parked more cash at the Fed overnight, pulling it out of general circulation

Implication: Third consecutive contracting signal; the TGA was nearly flat; the drain came from the overnight facility, not fiscal operations

4-Week Trend: Contracting 3 of 4 weeks. Issue #13 was the last expanding signal.

What Actually Happened

The week-ending TGA balance is $845.7 billion. That’s up $3.0 billion from last week’s $842.7 billion — close enough to flat that it’s not the story.

Last week, the TGA drove the signal. This week the reverse repo facility did.

The RRP ended the week at $325.8 billion — up $24.9 billion from last week’s $300.9 billion. Money market funds parked nearly $25 billion more at the Fed’s overnight facility. That cash doesn’t circulate. It doesn’t sit in bank reserves. It moves from the broader market onto the Fed’s liability ledger and stays there until the morning, when the trade rolls over.

When $24.9 billion moves in that direction in a single week, the effect on reserves is mechanical. Reserves fell $21.3 billion, from $3,067.0 billion to $3,045.7 billion.

Why did the RRP surge? The facility has been declining for weeks — it hit $300.9 billion last week, down from much higher levels earlier this year. Money market funds use the RRP when they have excess cash and the overnight rate there is competitive with alternatives. Quarter-end dynamics can also shift that calculus: banks tend to reduce their repo activity at the end of each quarter, which pushes money market funds toward the Fed’s facility instead. June 30 is approaching.

The Fed’s balance sheet provided a partial offset. T-bill holdings rose $6.6 billion to $469.5 billion — the Reserve Management Purchases running quietly in the background. SOMA stands at $6.436 trillion. Without those purchases, the reserve decline would have been closer to $27.9 billion.

Net liquidity in the financial system, combining Treasury cash balances and reverse repo usage.

The Mechanics, Briefly

For readers joining this series for the first time:

Reserve balances are what commercial banks hold at the Fed — the banking system’s collective checking account. When reserves rise, banks have more capacity to lend and invest. When reserves fall, that capacity tightens.

The TGA is the federal government’s checking account at the Fed. Tax receipts flow in; government spending flows out. When Treasury spends, money leaves its account and enters the banking system as reserves. When Treasury refills, money flows the other direction. The TGA and reserves sit at opposite ends of the same seesaw.

The RRP is an overnight facility where money market funds park cash at the Fed. Dollars sitting there are not in general circulation. When RRP falls, that money returns to the broader system. When RRP rises, that money exits.

This week: the TGA barely moved. The RRP pulled $24.9 billion in. The Fed’s ongoing T-bill purchases added approximately $6.6 billion back. Reserves fell $21.3 billion.

Reserve Balances and the Treasury General Account move inversely — when Treasury refills its account, reserves drain, and vice versa.

The Fed’s Two Hands

Most coverage of the Fed tracks the rate decision. That hand has been stationary.

Since December 12, 2025, the Fed has been conducting Reserve Management Purchases — buying Treasury bills at roughly $40 billion per month. Add approximately $13 to $15 billion per month in ongoing MBS reinvestment, and the Fed is putting around $53 to $55 billion per month back into the system through balance sheet operations.

These purchases don’t appear in the TGA or RRP lines tracked in this report. They land on the asset side of the Fed’s balance sheet, in T-bill holdings — which reached $469.5 billion this week, up $6.6 billion from last week’s $462.9 billion. Total securities held outright (SOMA) stand at $6.436 trillion.

The effect is a steady, quiet partial offset. This week, the RRP drained $24.9 billion. The TGA added another $3.0 billion. The RMPs added back approximately $6.6 billion. Reserves still fell $21.3 billion — but the gross drain before that offset was closer to $27.9 billion.

The balance sheet hand is not reversing the trend. It’s slowing the math.

What to Watch

The RRP is the line to track over the next few weeks. Quarter-end is June 30, and money market funds typically shift more cash toward the Fed’s overnight facility as banks reduce their repo activity to clean up balance sheets at month-end. If that dynamic is already building, the RRP could remain elevated or continue rising through the end of the month — extending the contracting signal further before any reversal. A sustained RRP decline after June 30 would be the first indication that quarter-end pressure has cleared. The TGA at $845.7 billion remains elevated; any sign of renewed Treasury spending resuming its drawdown would provide partial offset to whatever the RRP does in the near term.

The Bitcoin Lens

This week’s contracting signal came from an overnight facility, not a fiscal shift. $24.9 billion parked at the Fed, rolling daily, earning a small return. The TGA barely moved. From that distance, it looks modest.

These mechanics matter for Bitcoin’s short-run price environment. Less reserve capacity in the banking system is a tighter backdrop, and tight weeks tend to remove tailwinds more than add headwinds. But the RRP can reverse quickly — especially after quarter-end clears.

The longer view is what anchors this series. The system always needs more dollars — not as a preference or a policy choice, but as a structural requirement of a global reserve currency built on compounding debt. The TGA fills and empties. The RRP rises and falls. The Fed buys T-bills one month and pauses the next. The week-to-week mechanics move in every direction.

The total dollars in the system move in one direction. Bitcoin’s supply does not move at all.