The Feeling of Being Too Late Is Not Evidence of Being Too Late

What the Internet in 1997 Can Tell You About Bitcoin Today

Most people who “missed the internet” didn’t miss it in 2010. They missed it in 1997, when it was already 14 years old, already worth hundreds of billions of dollars, and already considered a technology that serious, early-moving people had already claimed. They sat out because it felt too late — and it was just getting started.

The Objection

The feeling of having missed Bitcoin is understandable. Not lazy, not uninformed — understandable. Reasonable, even.

Bitcoin has already gone from fractions of a cent to tens of thousands of dollars. The people who got in at $100 are real. The early gains are genuinely, mathematically gone. You can’t go back and buy Bitcoin in 2010. Nobody can. That’s not a question of conviction or timing — it just isn’t available anymore.

So the feeling makes sense. If you’ve followed Bitcoin from a distance for years — watched the cycles, watched the believers get excited and the skeptics get proven wrong, watched the price do things that defy reasonable expectation — and you still haven’t bought any, the natural conclusion is that the boat has sailed. The people on it are already somewhere else. Standing on the dock is just standing on the dock.

But here’s the thing worth sitting with: what if the feeling of being too late isn’t primarily about the asset? What if it’s mostly about how human beings process timing?

We’ve had this exact feeling before. And the last time we had it, we were completely wrong.

A Thought Experiment — 1997

Go back to 1997. The internet is 14 years old — the World Wide Web, the version most people think of, had been publicly accessible since 1991. It isn’t small or fringe anymore. It’s a genuine phenomenon generating real economic activity.

Microsoft’s market cap sits somewhere between $200 and $300 billion. Yahoo is worth $30 to $40 billion. Amazon just went public. E-commerce exists. The infrastructure buildout is underway — fiber optic cables are going in the ground, data centers are being constructed, capital is flowing in at scale.

If you tried to value the internet as a single privately owned entity in 1997-1998 — aggregating its infrastructure, its major companies, its economic activity, its content — you’d land somewhere around $275 to $400 billion.

That is not a small number. That is not a speculative toy. Anyone looking at those figures with a straight face in 1997 could reasonably conclude: the time to get in was five years ago. The people who recognized this early, who built companies or bought the right stocks — they’ve already made their fortunes. What’s left for me?

And they would have been completely wrong.

What Happened Next

The internet in 1997 didn’t slow down. It kept compounding.

Run the same valuation exercise today — infrastructure, the major platforms, e-commerce revenue, advertising, content and intellectual property — and you arrive at roughly $15 to $18 trillion.

From $400 billion to $18 trillion. That’s more than a 50x from the moment it already felt too late.

This isn’t cherry-picked optimism. The internet became the backbone of a new economy. Of course it compounded. That’s what backbone technologies do when adoption is still early, when most businesses haven’t yet adapted, when the infrastructure to support mass use is still being built.

The people who said “I already missed it” in 1997 weren’t making a market call. They were making a psychological call. They felt too late — and that feeling, however reasonable it seemed in the moment, wasn’t tracking the technology. It was tracking their own internal sense of having arrived at the party after the good music stopped.

The music hadn’t started yet.

The Uncomfortable Parallel

Bitcoin launched in January 2009. As of 2024-2025, it is 15 to 16 years old.

That’s almost exactly the same position the internet held in 1997-1998, when “I already missed it” was the dominant sentiment among people who were paying attention but hadn’t yet acted.

Bitcoin’s market cap in this period has ranged around $1 to $2 trillion — larger in absolute terms than the internet’s $400 billion in 1997, but the world is also significantly larger. What matters more than the raw number is where Bitcoin sits on its adoption curve.

Consider this: in 1997, most Fortune 500 companies didn’t have a website. Today, most don’t have a Bitcoin treasury strategy. That’s not a verdict on Bitcoin. That’s a description of where a technology sits in the adoption cycle — before the obvious decision has become obvious to everyone, before the institutional inertia tips.

The signals look familiar: enormous relative to where it started, potentially small relative to where it could go. The ratio of believers to skeptics, the regulatory clarity still being established, the institutional awareness still building — it all rhymes with 1997 in ways that are at least worth examining honestly.

The Key Difference That Makes This More Interesting

Here’s where the internet comparison starts to break down — not because Bitcoin is worse, but because it’s competing for something fundamentally different.

The internet creates value through activity. The commerce it enables, the services it hosts, the connections it facilitates. It’s a productivity technology. Its value is a function of how much economic output flows through it.

Bitcoin isn’t competing to host websites or deliver packages. It’s competing for a different pool entirely: the global store of value. Gold, at roughly $15 trillion. Sovereign bonds held as reserves. Real estate purchased not as a place to live but as a place to park wealth. The $100 trillion-plus global money supply. These are assets people hold not because they produce cash flows — a bar of gold earns nothing sitting in a vault — but because they’re trying to preserve the value of what they’ve already earned.

Bitcoin is pure monetary premium in a way the internet never was.

But there’s something even more important, and it’s the thing the internet comparison misses entirely.

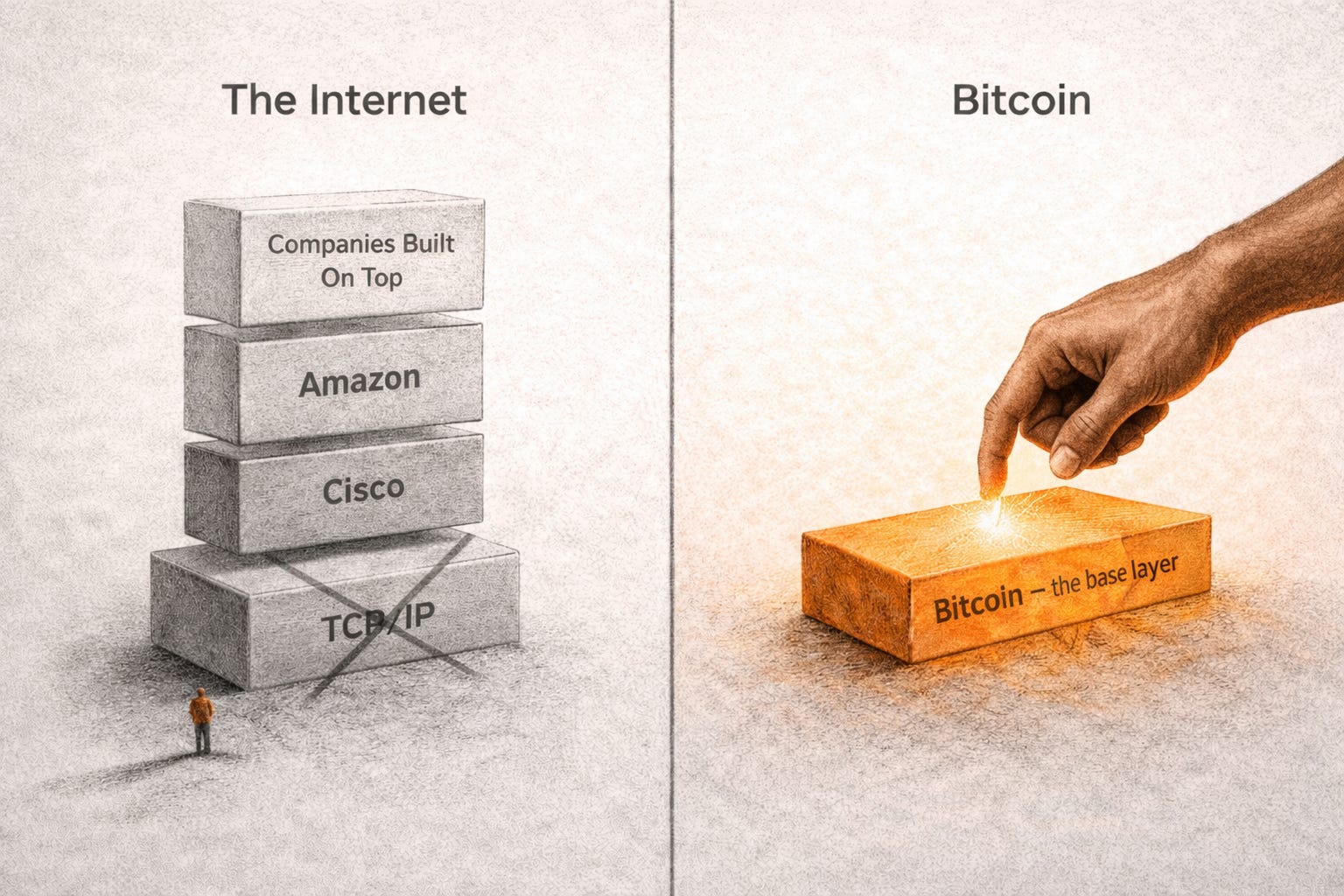

With the internet, you could never own the base layer. There were no shares of TCP/IP. No fractions of HTTP. If you wanted to participate in the internet’s rise, you had to buy equity in companies built on top of it — Cisco, Amazon, AOL, Yahoo. You were always one step removed from the thing itself. The infrastructure was never for sale.

With Bitcoin, the base layer is the asset.

You’re not buying a company that benefits from the network. You’re buying the network directly. Any fraction, held in a wallet only you control, with no intermediary standing between you and it. There will be — and already are — layers and companies built on top of Bitcoin: Lightning Network, layer 2s, Bitcoin-native financial services. Those are the Cisco and Amazon of this cycle. But underneath all of it sits the thing itself. And unlike the internet, you can actually own it. That option simply didn’t exist in 1997. It does now.

If Bitcoin captures even a fraction of the global store-of-value market, the 50x internet comparison isn’t bold speculation. It could turn out to be conservative — because the addressable pool is fundamentally larger, and this time the base layer is available for anyone to hold directly.

What You’re Really Saying

When someone says “I already missed Bitcoin,” they’re making a specific claim: that the majority of its value appreciation is behind it, not ahead of it.

That’s a falsifiable claim. And the burden of proof for it is significant.

The people who made that claim about the internet in 1997 weren’t foolish. They weren’t lazy. They read the room and reached the wrong conclusion — not because they lacked intelligence, but because they mistook the feeling of lateness for evidence of lateness. Those two things are not the same.

The feeling of having missed something is a psychological state. It’s your brain pattern-matching against situations where arriving late genuinely meant you were out of luck — the sold-out concert, the job that just got filled, the house that went to another offer. That pattern is useful in those situations. It isn’t a substitute for thinking carefully about where a technology sits in its adoption curve.

Here’s a more useful question: what would actually have to be true for the best days of Bitcoin to already be behind it? Work through that answer honestly. What would need to be true about adoption rates, about the global competition for store-of-value status, about the regulatory environment, about the technology’s durability and the institutions still on the sideline?

Don’t let the feeling do the work. The reasoning can.

The Window Isn’t What You Think It Is

You don’t have to believe in Bitcoin. But if your reason for staying out is that you already missed it, it’s worth asking: missed what, exactly?

The price that existed five years ago? That’s true — it’s gone and it isn’t coming back. But that’s not the same as missing the technology. The adoption curve. The window to own the base layer before the next wave of institutional and sovereign accumulation makes that decision feel as obvious as having a website did in 2005.

The window isn’t defined by price. It’s defined by where you are in the adoption cycle. And adoption, as of this writing, is still early by almost any reasonable measure.

In 1997, the internet looked late. It had just gotten started.