The Math Nobody Runs Before Buying the Dip

When a token crashes 80%, people think they're finally getting a good entry. The math says otherwise — and so does everything that drove the prior high.

Why “down 80%” doesn’t mean what you think it does

It’s somewhere in the next bear market. You’re scrolling through crypto charts — not your portfolio. You weren’t holding this one.

But a token that ran to $2.14 is sitting at $0.42. And the number feels like a signal.

The people who got in early already made their money. Now it’s actually cheap.

That sentence contains a math error most people never catch. This article is about that error — and the bigger one hiding behind it.

My journey to Bitcoin initially began through NFTs and yield farming obscure tokens. I know this feeling well — not from theory, but from experience. The pull of a price that used to be higher is quiet and almost automatic. It bypasses your critical thinking before you realize it’s happening. Running the actual numbers is what interrupts it.

The Math Nobody Runs

Let’s take the token seriously for a moment.

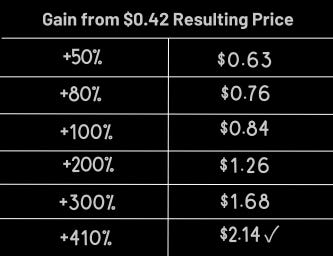

Peak price: $2.14. Current price: $0.42. That’s an 80% decline.

Here’s where most people’s thinking stops: It just needs to go up 80% and it’s back.

Run the numbers.

An 80% gain from $0.42 gets you to $0.76. Not even halfway back to $2.14.

A 100% gain — the thing doubles — gets you to $0.84. Still less than half the peak price.

To actually return to $2.14 from $0.42, the token needs to gain 410%.

Here is what I noticed when I finally ran those numbers: the gap between what a thing fell and what it needs to do to get back isn’t just uncomfortable — it’s consistently, quietly enormous. Percentage losses and percentage gains are not symmetrical. An 80% drop requires a 400% recovery. A 90% drop requires a 900% recovery. The math doesn’t care how you feel about the project.

This is the 410% problem.

But there’s a second problem hiding behind it. One that’s harder to see because it lives in an assumption rather than a calculation.

Why the Brain Gets This Wrong

The math is the easy part. The harder part is understanding why intelligent people never run it — and why they’d find a reason to dismiss it even if they did.

Anchoring to prior highs. The brain latches onto $2.14 as if that number is real and $0.42 is the temporary error. Psychologists call this anchoring — we treat the peak as the reference point and everything else as a deviation from it. For someone who missed the run, the old high isn’t even a loss. It’s a promise. The token proved it could get there. That feels like evidence. But the peak was almost always the product of specific conditions: a liquidity surge, a narrative moment, a wave of retail attention. It happened once, under those conditions. That’s not a guarantee it recurs.

Assuming the same cycle repeats. This is the real trap for late arrivals. The token went from $0.05 to $2.14. Why can’t it go from $0.42 to something even higher? The prior run looks like a proof of concept — a demonstration that the asset can do that. But the early gains were made by people who were positioned before the narrative was obvious. By the time a token is down 80% and visible to you, the early holders have already made their money and moved on to the next thesis. Catching the rerun of a cycle that ended is not the same thing as getting in early on a new one. You’re not early. You’re late to a party that ended.

Confusing price collapse with value. Price fell. That’s what happened. But did value fall? And — more importantly — was there a durable value floor to begin with? In traditional investing, earnings and cash flows create a floor. A company can be undervalued relative to what the underlying business actually generates. Many altcoins have no equivalent. Their value was whatever peak enthusiasm was willing to pay. When that enthusiasm ends, there’s nothing underneath to catch the fall.

“It used to be worth more” is history, not a promise. The market has no memory and no obligation. The prior high existed under a specific set of conditions that may be gone. Trends die. Narratives shift. Attention moves. Projects that were everywhere in one cycle are forgotten in the next. History records the number. It doesn’t guarantee the return.

Applying Bitcoin’s pattern to everything. Bitcoin has a documented history: deep bear market drawdowns followed, eventually, by new all-time highs. Many investors observe that pattern and apply it universally — assume every token will recover if you just hold long enough. Bitcoin is not a template. It is an exception. Most altcoins have not replicated that pattern. Many have never returned to prior highs after a cycle ends.

Survivorship bias. The coins that 100x get podcast episodes, Twitter threads, and dinner table conversations. The ones that went to zero or drifted down 95% and stayed there just disappear. Quietly. No post-mortem, no announcement. This creates a systematically distorted picture — the wins are loud, the losses are silent, and the base rate looks far better than it actually is.

“Buying the dip” as social currency. In bull markets, this phrase gets rewarded and celebrated. It works — until it doesn’t. The narrative carries forward into bear markets where it means something entirely different. A dip in an uptrend is a temporary pullback. A dip in a bear market can be a step down a staircase with no visible bottom.

What’s Actually Different About Bitcoin

This isn’t an anti-crypto argument. It’s a contrast argument — and the contrast matters.

Bitcoin was the first. Not first in a “who got there before everyone else” sense — first in a “this is what all of this was supposed to be” sense. The Bitcoin whitepaper describes a peer-to-peer electronic cash system. That’s the whole document. It was built to be money. Not a platform for launching tokens, not a layer for decentralized applications, not a vehicle for anything else. The purpose was singular, and it hasn’t changed.

Bitcoin uses proof of work. This matters more than some explanations give it credit for. Every single new Bitcoin that enters circulation had to be produced through real-world energy — electricity, hardware, computational effort. The cost of production has a physical floor. It isn’t arbitrary. Every transaction on the network is validated the same way: real energy, real cost, real stakes. You cannot fake it. You cannot shortcut the thermodynamics.

There are tens of thousands of other blockchains. Most of them do not use proof of work. They use proof of stake or other mechanisms where validation is tied to how many tokens you already hold rather than how much energy you expend. Some do use proof of work — but nearly all of them have something Bitcoin doesn’t: a known creator. A founder. A company. A foundation. These are real people who can be pressured, regulated, discredited, or arrested. Their existence creates a vulnerability — a point of attack, a point of negotiation, a point of capture.

Satoshi Nakamoto disappeared. Intentionally, it appears. There is no one to arrest. No company to sue. No foundation to co-opt. No single developer who can be pressured into changing the rules.

The real governance of Bitcoin belongs to node runners — the individuals and institutions who run the Bitcoin software on their own hardware, maintain a copy of the entire transaction history, and verify the rules of the network. Here is what makes this remarkable: even if the most influential developers in the world reached consensus on changing Bitcoin’s rules, node runners are not required to adopt that version. They can simply continue running the version they believe in. The network is whoever is running the code.

This isn’t theoretical. It’s been tested. When a significant portion of Bitcoin’s development community and mining power backed Bitcoin Cash in 2017, it failed to displace Bitcoin. The nodes running the original rules kept running them. The version closest to what Satoshi originally designed remained the dominant network by a margin that isn’t close — and has only grown since. There is a reason Bitcoin Cash is not in the same stratosphere.

There’s one more thing worth saying about Bitcoin’s design, because it’s genuinely unusual in the history of financial systems.

In almost every system ever built, powerful participants are at least occasionally tempted to extract value at the expense of others. In Bitcoin, the incentives point the other direction. Miners need Bitcoin to have value to profit from their work. Holders need the network to remain trustworthy. Businesses built on Bitcoin need it to function. Node runners gain nothing from weakening the rules. Every participant who joins the network — whether it’s an individual protecting their savings, a family passing wealth across generations, a corporation managing a treasury, a community in a country with an unstable currency, or a sovereign nation building reserves that no other government can freeze — has interests aligned with the network’s health.

It is one of the only systems in history where joining makes it stronger, and where attacking it works against the attacker’s own interests.

Gold is the natural comparison. And gold has a long, credible history as a store of value. But gold is heavy. It’s expensive to store, costly to verify, and slow to move. It can be seized, counterfeited at scale, or replaced by paper claims that don’t represent the real thing. France once had to sail a ship across the Atlantic to attempt to redeem gold from the United States. Bitcoin can be transferred to the other side of the world, verified instantly, without a ship, without a third party, without anyone’s permission.

Think of what it means to hold value in something that can cross any border, survive any government, be divided into units small enough for anyone, and persist as long as the network runs. It is pure economic energy in digital form with no expiration date.

And the network effects are already, realistically, insurmountable. Even if someone built a technically identical system tomorrow — same supply cap, same proof of work, same design — it would start with nothing. No liquidity. No infrastructure. No institutional adoption. No cultural legibility. The people already holding Bitcoin have no reason to switch. New participants seeking a store of value would choose the network with the deepest pool of people to transact with. There is no second Bitcoin because there is no reason for a second one, and no one would be incentivized to join it. The pool of participants on a clone would be infinitely smaller. The incentive to join it would be infinitely weaker.

This is a one-of-one asset. Not because of price. Because of design, history, network, and incentives.

What “Cheap” Actually Means

“Down 80%” tells you what happened. It says nothing about what comes next.

The right question isn’t how much it fell. It’s: what would have to be true for this to recover — and is that actually likely given current conditions?

Cheap means underpriced relative to value. Price collapse alone doesn’t create value. It creates proximity to a number that used to exist, under conditions that may no longer exist.

The 410% problem is not just a calculation about one token. It’s a mental model. An asset can be down 80%, require a 410% recovery, and still not be cheap — if the narrative that drove the prior high has already moved on, if the early money is long gone, and if nothing fundamental has changed except the price.

The Shifted Perspective

Some altcoins do recover. The problem is that survivorship bias makes it look like they all do eventually — when in reality, the ones you heard about are simply the ones that made it. The ones that went to zero disappeared quietly.

The math is quiet and it doesn’t care about your feelings about a project. A 90% drawdown requires a 900% recovery. If that sounds unreasonable, it should — because for most things, most of the time, it is.

Bitcoin has done it. Repeatedly. Whether it continues to is an open question no one can honestly close for you. Because of its properties, I believe it’s real world purchasing power will trend in an upward direction forever.

The next time something feels cheap because it used to be higher, run the numbers first. A 410% recovery is not given. And even if it happens, the early money won’t be waiting to ride it back up with you. They made their gains and moved on.

The token isn’t on sale. You’re just late — and mistaking someone else’s exit for your entry.