The Menu is Broken

Why the four savings tools everyone recommends quietly fail the people who need them most

You do everything right. You get the degree, land the job, start putting money away. And yet — a few years in — it feels like you’re running in place. Your salary goes up, but so does everything else. The treadmill is speeding up, and nobody is explaining why the effort isn’t translating into ground.

The default assumption — the one most of us carry for a long time — is that the problem is personal. Maybe you’re not disciplined enough. Maybe you’re spending too much on small things. Maybe if you just optimized a little harder, found a better budgeting app, or finally started tracking every dollar, you’d feel like you were actually getting somewhere.

But what if the problem isn’t discipline? What if the tools themselves are broken?

When you enter adult financial life, the system hands you a menu. It’s presented as comprehensive — cash, savings accounts, retirement accounts, real estate. Four options, all legitimate, all widely used, all recommended by people who seem to know what they’re talking about. What almost nobody tells you is that every single option on that menu has a fundamental flaw baked into it. Not because the people who designed them were malicious, but because the menu was built around a different set of priorities than yours.

Before you can understand why saving feels so hard, it helps to take an honest look at what’s actually on offer.

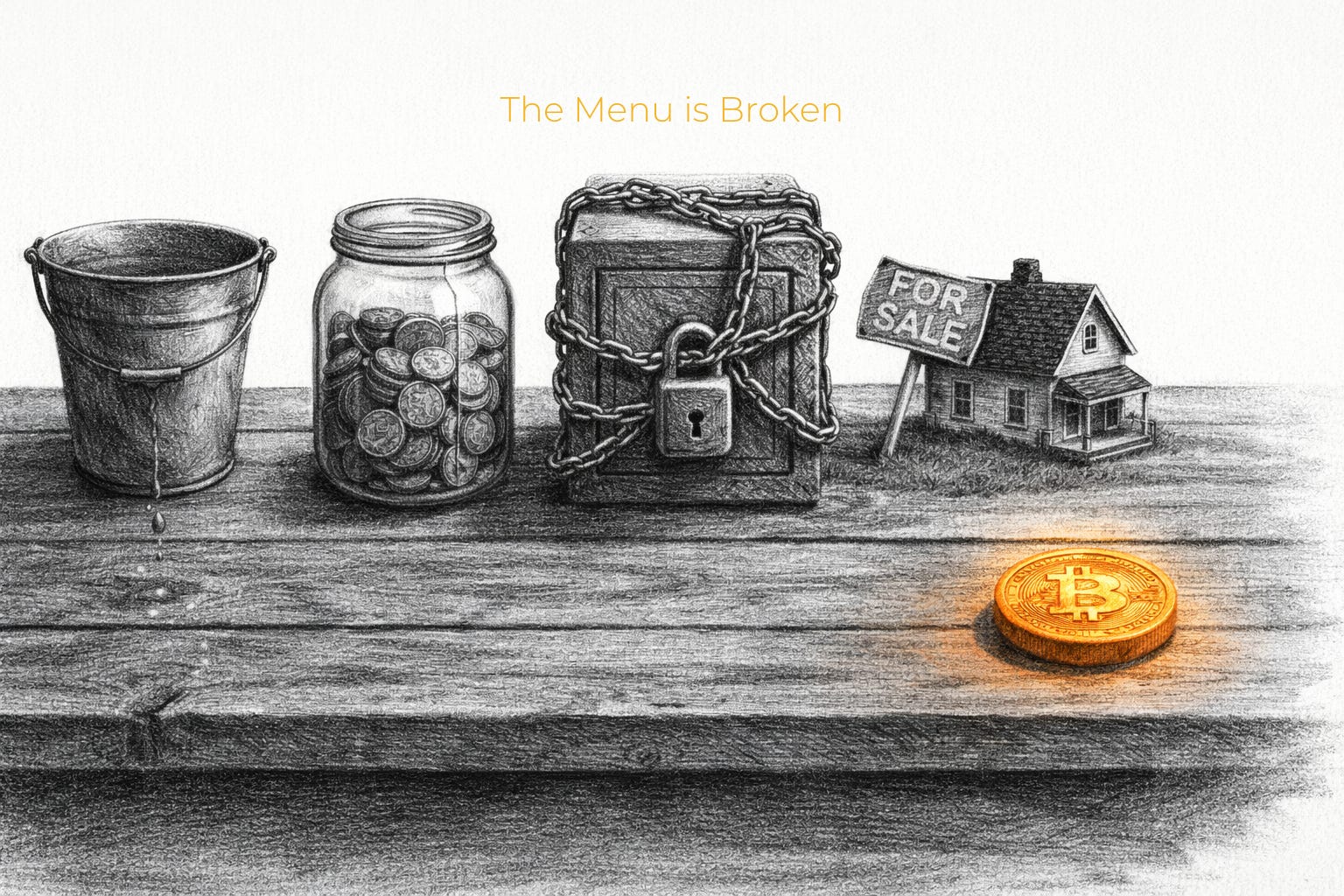

Option 1: Cash — The Bucket With a Hole

Cash is where most people start. It’s tangible, familiar, and immediately accessible. Holding it feels responsible — like a baseline of financial sanity. You know exactly how much you have at any given moment, and that certainty is genuinely comforting.

But here’s something that doesn’t get explained nearly enough: the Federal Reserve explicitly targets 2% inflation per year. That’s not a side effect of monetary policy — it’s a stated goal. The Fed is, by design, engineering an environment where a dollar held today is worth slightly less than a dollar held last year. Compounded over time, “slightly less” becomes something more serious. A dollar from 1970 buys a fraction of what it bought then. The same forces that feel manageable year over year have, over decades, accumulated into something dramatic.

Think of it this way: holding cash is like carrying water in a bucket with a small hole in it. You’re not saving — you’re deciding how fast it drains. The hole is small enough that you don’t notice it immediately, but it’s been there the whole time, and the longer you carry the bucket, the more you lose.

The most uncomfortable part of this isn’t the math. It’s that holding cash *feels* prudent while it’s quietly doing the opposite of what you think it’s doing.

Option 2: The Savings Account — Neutral Is Not Enough

A savings account feels like a step up. You’re not just holding cash — you’re putting it somewhere that earns something. For a long time, most of us take quiet satisfaction in watching a small interest figure appear on our monthly statement.

One question worth asking is whether that interest rate keeps up with inflation. And historically, for most people in most time periods, the answer is no — or barely.

When the inflation rate meaningfully exceeds the rate your savings account pays, you are losing purchasing power while believing you are preserving it. The number in the account goes up; its real value goes sideways or down.

The interest rate problem is worse than it first appears because the dollar value of the return depends on how much you already have. At 3% annual interest:

- $10,000 earns $300 — not worth the illiquidity for a year

- $1,000,000 earns $30,000 — worth it

This is a miniature version of the Cantillon Effect built into the savings account itself: the tool nominally available to everyone advantages the already-wealthy far more than it advantages the person who needs it most. Higher deposits also earn higher rates at many banks (e.g. money market tiers, jumbo accounts) because large deposits increase the bank’s lending capacity.

There’s also a behavioral problem built into savings accounts that rarely gets acknowledged. Because the money is so accessible — a few taps on your phone and it’s in checking — it tends to get spent on emergencies, unexpected car repairs, or one-time opportunities before it accumulates into something meaningful. The account that’s supposed to be a step up from checking often functions as a slightly more formal version of the same thing.

This isn’t a criticism of people who use savings accounts. The tool just doesn’t do the job it appears to do. It offers the feeling of saving without the reality of value preservation.

Option 3: The 401k — The Best of a Bad Bunch

Of the four options on the standard menu, the 401k is genuinely the strongest — and that deserves to be said plainly. Particularly when an employer offers matching contributions, a 401k is one of the few mechanisms that allows an ordinary person to build wealth over time while capturing a meaningful benefit that effectively increases their total compensation. If you have access to an employer match and you’re not using it, that’s worth changing.

But the 401k comes with trade-offs that tend to get glossed over in standard financial guidance.

The first is illiquidity. Your money is effectively locked up until you turn 59½. Withdraw early and you face income taxes on the withdrawal plus a 10% penalty on top of that. The tool that’s supposed to be your primary savings vehicle is one where accessing your savings before a certain age costs you significantly. In a financial emergency — a job loss, a medical crisis, a major unexpected expense — you often cannot reach the funds you’ve been setting aside for years without a serious financial hit.

The second is market exposure at precisely the wrong moment. The 2008 financial crisis hit many people hardest when they were closest to retirement, meaning they had both the most to lose and the least time to recover. Decades of disciplined contributions were reduced dramatically in a short period — not because of anything they did wrong, but because the primary vehicle for wealth-building available to them was tied to market performance they couldn’t control.

The third problem is subtler. The 401k requires ordinary people to become investors in a way they didn’t necessarily choose. You have to decide how to allocate across funds, how to rebalance, how to think about risk at different life stages. The system frames this as empowerment. For many people, it functions more like: there’s no other viable option, so here’s a set of complex levers to manage on top of everything else you’re already managing. The system forces everyone to become, in some sense, a gambler or a speculator — not because they wanted to, but because the alternative is holding cash in a leaking bucket.

Option 4: Real Estate — The Inaccessible Lifeboat

Historically, real estate has been the best store of value available to ordinary people. That’s still largely true, and it would be dishonest to suggest otherwise. A home purchased in a growing market and held through cycles has tended to preserve and grow purchasing power in ways that most other options haven’t matched consistently. Real estate works — when you can get in.

That’s the problem.

Buying a home requires a down payment — typically a meaningful percentage of the purchase price, often tens of thousands of dollars — before you can begin building equity. For someone starting out, carrying student debt and paying rent, accumulating that lump sum can feel like trying to catch a moving train.

And the train has been accelerating. After successive rounds of quantitative easing — the large-scale asset purchase programs the Federal Reserve conducted after the 2008 financial crisis, and again during the COVID-19 pandemic — home prices broadly inflated well beyond what wage growth could justify. The down payment that might have been achievable in 2010 had become a different target by 2020 and a different one again by the mid-2020s. In many markets, the math simply doesn’t close for someone earning a median income and starting from zero.

There’s also the reality of what happened in 2008. The people who suffered most severely in the housing crisis weren’t reckless speculators, by and large. Many were ordinary families who had done exactly what they were supposed to do — buy a home, build equity, treat it as their financial foundation — and discovered that when leverage meets a declining market, the damage can be severe and lasting. Real estate is illiquid. You can’t sell a bedroom when you need cash for an emergency. The asset works until it doesn’t, and when it doesn’t, you can’t exit quickly.

There’s an irony worth naming here: real estate works as a store of value precisely because money flows into it seeking protection from inflation. The same force that quietly erodes your savings makes houses expensive. It’s the same problem, seen from two different angles.

The Menu Got Worse

Each of these options existed before 2008. After 2008, they got harder to use.

When central banks around the world responded to the financial crisis with large-scale monetary expansion — and then repeated the process during COVID — they kept the global financial system from collapsing. That’s not a small thing. But the mechanism for doing so had consequences that fell unevenly.

Quantitative easing works, in part, by inflating asset prices. When the Fed buys assets and holds interest rates low, capital flows into stocks, real estate, and other stores of value in search of returns. People who already own assets benefit. People who are still trying to save enough to enter the market watch the target move further away.

What looks like assets “going up in value” is, in many cases, not those assets becoming more productive or more useful. It’s the unit we’re measuring them in — the dollar — becoming less valuable. The house didn’t become a better house. The dollar bought less of it. As a result, every option on the standard menu now costs more to access and delivers less in real terms than it did a generation ago. This isn’t bad luck. It’s a predictable outcome of how the monetary system functions.

The Question That Should Already Have an Answer

At some point, if you sit with all of this long enough, you arrive at a question that sounds almost embarrassingly simple:

*Why can’t we just earn something, securely store it, and be confident it will have the same or greater purchasing power later?*

This isn’t an unreasonable thing to want. It’s arguably the most basic function you’d want money to serve. Not speculation, not market timing, not the ongoing management of complex instruments — just the ability to store the value of your work and trust that it’ll still be worth something later.

None of the four options on the standard menu fully answer that question. Cash erodes by design. Savings accounts barely keep pace in the best of times. The 401k locks your money away and ties its fate to market performance. Real estate has worked for those who could get in, but carries illiquidity risk and has moved structurally out of reach for a growing portion of the population.

That’s not a coincidence or a run of bad luck. It’s what you’d expect from a monetary system that wasn’t designed around the needs of the ordinary saver.

The Option That Was Missing

Bitcoin is not easy to explain briefly, and this piece isn’t an attempt to explain all of it. But it’s worth walking through why it answers the question that everything else leaves open.

Bitcoin has a fixed supply. There will only ever be 21 million of them. That number is enforced by a global network — not by a committee, not by a central bank, not by any single person or institution. Nobody can create more, regardless of how much incentive exists to do so. Gold has historically served as a hard money because supply is limited by the physical difficulty of mining it — but if prices rise high enough, humans will find more gold. With Bitcoin, additional supply is structurally impossible. The rules are code, and the code doesn’t bend.

That single property changes everything about how it functions as a store of value. Every other option on the menu is subject to dilution in some form — cash through money creation, real estate through new development, stocks through share issuance. Bitcoin is the first widely accessible asset where the supply is genuinely, structurally, permanently fixed.

It’s also accessible in a way that nothing else on the menu is. There’s no down payment. No employer has to offer it. There’s no minimum, no financial advisor required, no waiting period. Anyone with a smartphone and internet access can acquire it — in any amount, starting with whatever they can manage. Most people don’t buy a whole Bitcoin; they buy fractions, sometimes very small ones, in amounts that fit their situation.

A useful way to think about it: imagine all 21 million Bitcoin as a single piece of the most valuable real estate on the planet. Anyone can own a piece of it, in any size, at any time. You don’t have to buy the whole thing. You can add to your share over time as you’re able. Unlike a house, you don’t have to sell all of it at once when circumstances change — you can exchange a portion of it back into dollars in minutes, as much or as little as you need.

And when you hold Bitcoin in what’s called self-custody — meaning you hold the private keys yourself, rather than keeping it on an exchange — you own the actual asset. Not an IOU. Not a fund share. Not a claim that depends on a company staying solvent. The thing itself. That distinction sounds technical, but it matters in a way that most traditional financial instruments can’t match.

The volatility is real, and it would be dishonest to minimize it. Bitcoin’s price in dollar terms has swung dramatically, in both directions, multiple times. And over time, it has proven favorable for the patient holders who think in years, not days. It’s also worth separating two kinds of risk: the volatility that’s visible — price moves you can track on a chart — and the erosion that’s structural — the slow, invisible loss of purchasing power that characterizes every other option on the standard menu. One is loud. The other is quiet. Only one of them tends to get called “safe.”

A Different Way to See the Menu

The feeling of running in place — working hard, doing everything you’re supposed to do, still not gaining ground — isn’t a personal failure. It’s a rational response to a set of tools that don’t actually solve the problem you’re trying to solve.

The menu you were handed after graduation isn’t unique to you. It’s the same menu everyone gets. The options on it have real histories and genuine uses. But none of them fully answer the most basic question a person can ask about money: how do I store what I’ve earned and trust that it’ll still be worth something later?

Understanding that the question doesn’t have a good answer in the existing system isn’t pessimism. It’s clarity. And clarity tends to be where better decisions begin.