Why the Fed's Balance Sheet Can Never Go Back to Normal

The hawk just hired the doves' economist

Kevin Warsh spent years at the Federal Reserve as the member most likely to dissent against quantitative easing. He warned, publicly and repeatedly, that flooding the banking system with reserves would distort markets and create dependencies that would be nearly impossible to unwind. He was right, and mostly ignored.

He’s spent 15 years being one of the most vocal people about the Fed’s balance sheet. Now, as the Fed Chair, his first major appointment to lead balance sheet policy includes Raghuram Rajan and Jeremy Stein.

If you know those names, you see the irony immediately. If you don’t, here’s why it matters: Rajan and Stein are two of the three co-authors of a paper presented at Jackson Hole in 2022 that provides the clearest academic argument for why the Fed’s balance sheet cannot be meaningfully or permanently shrunk.

The paper is called “Liquidity Dependence: Why Shrinking Central Bank Balance Sheets in an Uphill Task”.

Its core finding is that every round of quantitative easing leaves the banking system more dependent on reserves than before — not less. The ratchet clicks. It doesn’t unclick.

Warsh just handed his most important policy question to the people who wrote the academic case for why his preferred answer won’t work.

What the paper actually found

The paper starts from a straightforward observation about how banks work.

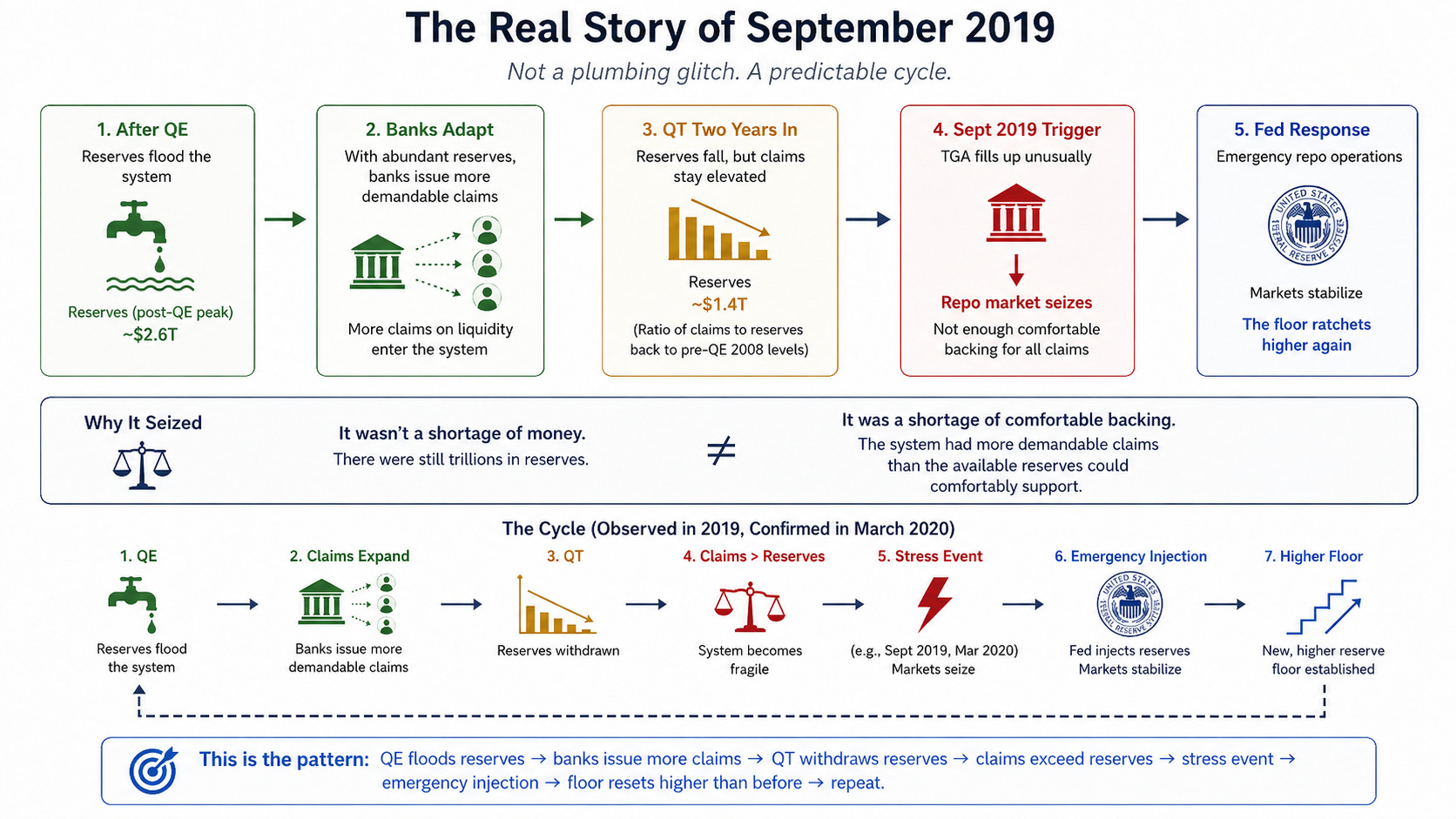

When the Fed expands its balance sheet during QE, it floods the banking system with reserves. Banks take that cheap, available money and do what banks do: they issue more promises to provide cash on demand — checking accounts, credit lines, overnight lending commitments. These are called “demandable claims.” Think of them as obligations the bank has made to hand you money whenever you ask.

Here’s the problem. When the Fed tries to shrink the balance sheet with QT, the reserves leave. But those demandable claims don’t. They’ve become embedded in the system. The banking sector’s promises to provide cash on demand have grown. The cushion available to back those promises has declined.

The paper’s exact language: “the supply of reserves creates its own demand for reserves over time, ratcheting up the required size of the Fed’s balance sheet.”

I want you to take a minute and think about what that’s saying. I read it as each round of QE being essentially a permanent because of how banking reorganizes itself when the system gets flooded with reserves. The banking system adjusts to the new level of Fed support. When support is withdrawn, the newly reorganized system breaks.

The evidence is in what happened to bank liabilities between 2009 and 2021. Time deposits — stable, longer-term funding that doesn’t need to be repaid immediately — fell from about 25% to 5% of GDP. Demand deposits (checking accounts, instant-access money) rose from roughly 30% to 80% of GDP. The banking system permanently shortened the maturity of how it funds itself. More promises came due immediately. Fewer were structured to wait.

The floor rose. And the structure of the banking system reorganized to require that the floor stay there.

September 2019 wasn’t a plumbing accident

Our uber intelligent leaders want you to believe that the September 2019 repo market seizure was a technical glitch — a temporary mismatch between Treasury bill supply and reserve levels, worsened by the Treasury General Account sitting unusually full. The Fed stepped in, markets stabilized, and the episode was mentally filed under “weird but fixable.”

The paper reframes it entirely.

By September 2019, the Fed had been running QT for two years. Reserves had fallen from their post-QE peak to roughly $1.4 trillion. That’s still an enormous number in absolute terms. But the ratio of demandable claims to available reserves had crept back to pre-QE 2008 levels. The absolute number of reserves had changed. The ratio hadn’t. And it’s the ratio that breaks things.

There was enough money in the system, but it seized because the banks had issued far more claims on liquidity than the reserves available could comfortably back. The Treasury account filling up was the trigger. The system that reorganized itself around higher reserves, was now being asked to function with fewer of them.

March 2020 confirmed the dynamic at larger scale. COVID created the stress event; the Fed’s predictable response of injecting trillions, stabilized it. And the floor ratcheted up again.

The pattern: QE floods reserves → banks issue more demandable claims → QT withdraws reserves → claims exceed reserves → stress event → emergency injection → floor resets higher than before → repeat.

Why the fix isn’t more QT

The paper’s proposed solutions are notable for where they look: not at the Fed’s balance sheet, but at bank behavior.

The authors’ argument goes like this:

Banks issuing more demandable claims than they could actually meet isn’t irrational. Given the context, it’s rational. The Fed has repeatedly demonstrated that when liquidity stress arrives, it will intervene. So issuing commitments you couldn’t fully honor if everyone called them at once is a reasonable bet — the Fed will cover you.

The paper calls this the “liquidity put,” and banks have been rationally exploiting it for fifteen years.

Fixing the ratchet means changing those incentives. Requiring longer deposit maturity. Stricter stress tests for credit-line drawdowns. Counter-cyclical supervisory pressure to prevent the kind of liability shortening that happened from 2009 to 2021. Possibly requiring banks to hold reserves against credit lines the same way they hold capital against loans.

These aren’t bad ideas. But they operate on a ten-year horizon, not a quarterly one. In the meantime, the banking structure that exists is the one that exists. And that structure, the paper argues, has already reorganized around a balance sheet floor it can’t easily operate (or operate at all, IMO) below.

One more finding complicates the usual defense of QE. QE is meant to pull long-term interest rates down by nudging investors toward riskier assets with greater yield. But banks adapt too. During QE, they shorten the maturity of their own liabilities, partially undoing the very effect the policy is trying to produce. So QE may be weaker on the way in and harder to reverse on the way out — an uncomfortable combination.

The steelman

The paper does not say QT is impossible. That’s the honest version of what it found.

What it says is that QT is harder and riskier than conventional models assume, and that the costs are asymmetric; shrinking is more disruptive than expanding. I don’t want to make it sound like they’re promoting “QE forever”. Rather, the authors’ conclusion is that if you want to be able to reverse QE, you have to fix bank behavior first.

Their proposed fixes — supervisory requirements on deposit maturity, credit-line stress tests, reserves averaging requirements — are legitimate policy tools that could, over time, reduce the dependence they’ve documented.

Reserve levels did fall significantly after 2014. But the ratchet raises the floor over the long run even if there’s some runoff in between crises.

However; if the fixes required to make QT sustainable are supervisory and multi-year, and the next stress event arrives on a shorter timeline, the interim period looks like the current structure continuing to operate with its current dependencies. Which means the floor stays where it is until the supervisory work is done — if it gets done.

What Warsh might actually do

This is the genuinely open question, and I don’t have a confident answer.

Option one: Warsh uses the Rajan-Stein appointment as intellectual due diligence — let the authors of the academic case do the hard work of identifying what supervisory fixes are needed to make QT viable, then execute anyway. The hawk gets the doves to write the manual for how to make the hawk’s preferred policy work.

Option two: the task force findings, combined with the political and financial stability pressures of actually trying to run QT against a system that has already reorganized itself, persuade Warsh that the cost is too high. The conclusions land in late 2026 — inside a global liquidity window already under pressure — and the message is “not now, not this way.”

Option three: the task force doesn’t matter much because the next crisis arrives before the findings do. Fiscal pressure, a sovereign debt dislocation, another repo event. And the response writes itself, regardless of what any task force concluded.

My personal bet would be some version of option three. Crisis arrives before any meaningful changes can be made and his hand is forced. The global debt-based fiat system is near the end game and the options are limited to print or perish.

The paper’s closing line is understated in a way that makes it land harder: “QT may therefore not be as benign or painless for the financial sector and the economy as QE.” Expanding is easy. Contracting is hard.

The question this leaves

If the paper is even partially right, then the Fed’s balance sheet has a floor that rises with each cycle. The supervisory fixes that could lower that floor take years. The stress events that force re-expansion tend to arrive on shorter timelines. The ratchet goes up. It doesn’t reverse in a straight line.

Each time the Fed expands again because of whatever inevitable crisis unfolds, the new floor lands higher than the last one.

Warsh knows this. The economists he hired spent twenty years proving it. The task force he built from that knowledge may produce real supervisory reforms that matter over the next decade. But the next decade starts from wherever the floor sits today, not from wherever it sat in 2008.

The H.4.1 series I run each week tracks the weekly mechanics of that floor: the TGA, the RRP, the reserve balances that tell you whether the plumbing is loose or tight. Week to week it moves in every direction. The secular direction is the one this paper is describing.

If the reserve base has a floor that only ratchets upward, and that floor rises with each crisis response, the logical question is: what asset is designed for a world where the dollar supply only expands? Not week to week. Not QT versus QE. In aggregate, across cycles, over decades. Forever.

The paper is an academic proof of the mechanism behind everything this publication tracks. Bitcoin — or as I like to call it — the orange sponge, keeps absorbing because the level of liquidity underneath everything else doesn’t stop rising.

Source: Acharya, Chauhan, Rajan & Steffen, “Liquidity Dependence” (Jackson Hole 2022). Task force appointments reported July 9, 2026.