Why the Financial System Doesn't Need Greedy People to Hurt You

From Norfolk Southern to your savings account — why harmful outcomes don't require villains.

Gordon Gekko said greed is good.

But here’s what nobody followed up with: the system doesn’t actually need greed to work the way it does. It doesn’t need anyone to be greedy. It just needs the incentives to be arranged a certain way — and then it runs itself.

Self-Interest Isn’t the Same Thing as Greed

Adam Smith is often cited in the same breath as Gekko, as if “greed is good” were simply a more aggressive paraphrase of The Wealth of Nations. But Smith didn’t praise greed. He praised self-interest — and the distinction matters more than most people realize.

Self-interest is comparative. It’s the natural competitive drive to improve your position relative to others. It motivates people to work harder, innovate, build things. Smith argued this force, operating across many individuals in a market, could produce outcomes that benefit everyone even though no one designed them to.

Greed is something else. Greed is acquisition without consideration of how others are affected. It’s not “I want to do well” — it’s “I want to do well regardless of what it costs anyone else.” The research on this distinction is fairly clear: greedy individuals do accumulate more material resources, but they also report lower life satisfaction, weaker relationships, and a measurably more objectifying view of the people around them.

The Gekko version collapses the two into one. And that’s where the confusion starts — because once you assume harmful outcomes require greedy actors, you spend all your time looking for the villain instead of looking at the structure.

Nobody Had to Be Evil in East Palestine, Ohio

On February 6, 2023, a Norfolk Southern freight train carrying hazardous chemicals derailed in East Palestine, Ohio. Toxic materials were released. Residents were evacuated, then told it was safe to return. The long-term health consequences are still unfolding.

Before the derailment, Norfolk Southern had helped block a federal safety rule intended to upgrade the rail industry’s braking systems — systems that hadn’t been meaningfully updated since the Civil War era. The company had also successfully lobbied against a “high-hazard” classification that would have triggered stricter safety oversight. And it had laid off thousands of workers despite internal warnings that understaffing was creating safety risks.

Were the executives sitting around a table saying “let’s poison a town”? Almost certainly not. They were responding rationally to the incentives in front of them. Safety upgrades cost money. Lobbying against regulations saves money. If something goes wrong, the cost falls somewhere else — on the residents, on the environment, on the future legal proceedings. The rational calculus, inside those incentives, pointed in one direction.

The structure produced a harmful outcome without requiring a single cartoon villain.

You can run the same analysis on the 2008 financial crisis. Powerful market incentives pushed financial firms toward increasing leverage and resisting regulation — not because they were uniquely evil, but because the system rewarded short-term risk-taking and punished caution. When it collapsed, it wasn’t because unusually bad people had taken over Wall Street. It was because the structure selected for certain behaviors, and those behaviors, aggregated across thousands of rational actors, produced a catastrophe.

Replace the people. The architecture produces the same outcomes.

The Monetary Version of the Same Thing

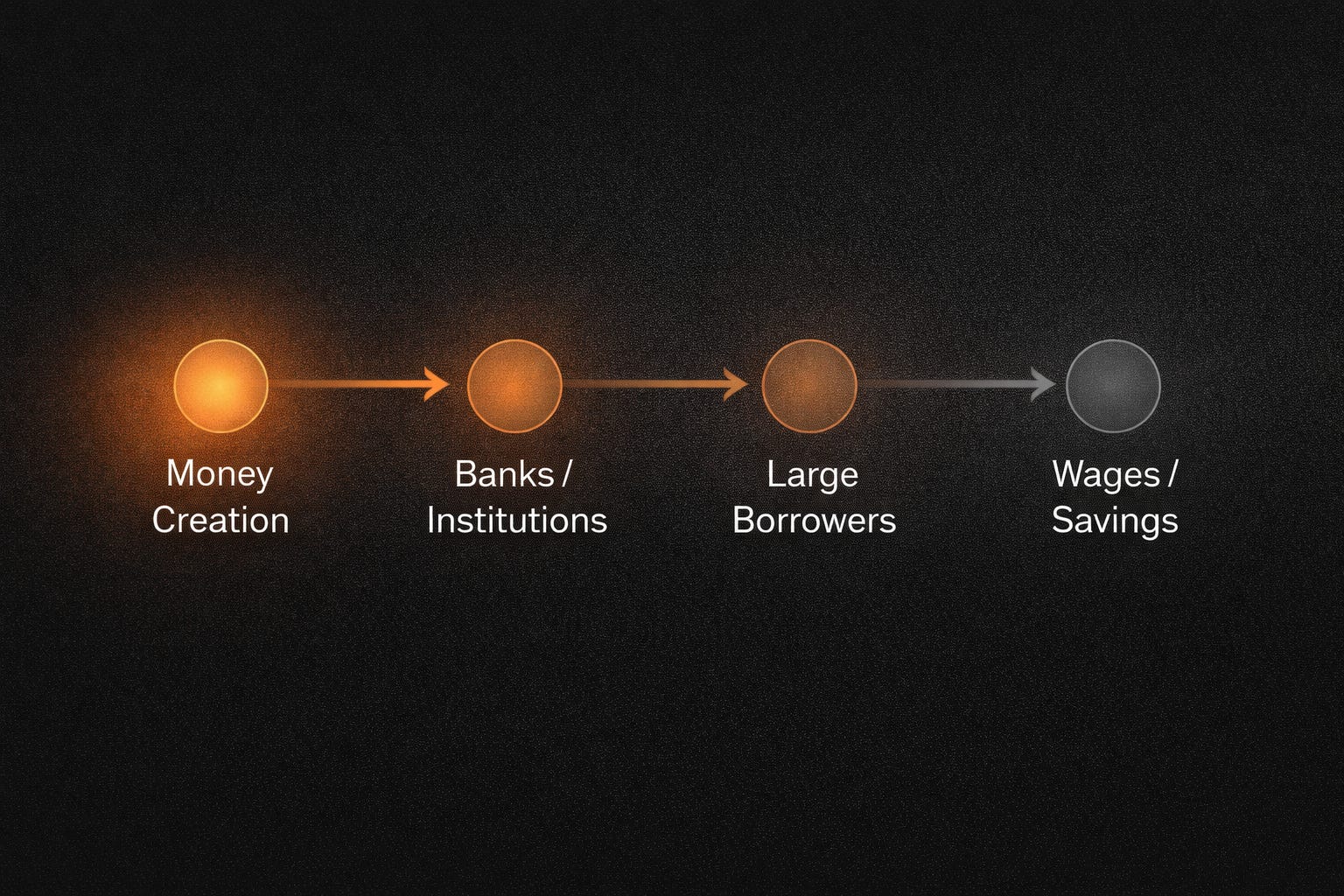

The Cantillon Effect is what happens when you apply this structural logic to money creation.

New money doesn’t appear everywhere at once. When the Federal Reserve expands the money supply — through bond purchases, reserve management, or the various tools it has accumulated over a century — that money enters the system at a specific point. Banks and financial institutions access it first. Large borrowers access it next. By the time it moves through the economy and eventually shows up in wages, the price level has already begun adjusting upward.

The people first in line capture purchasing power before prices rise to reflect the expanded supply. The people at the end of the chain — the person with $40,000 in a savings account, the worker whose salary adjusts slowly or not at all — absorb the cost.

Nobody at the Federal Reserve has to want to hurt you for this to happen. The mechanism doesn’t require malice. It doesn’t even require awareness. It runs on the physics of how money moves through an economy where it enters at one point and distributes outward from there.

The outcome looks like greed — the wealthy accumulate, the saver’s purchasing power quietly erodes, the gap widens year after year. But the cause isn’t character. It’s the incentive structure embedded in the architecture.

Architecture, Not Character

When we blame individuals, something feels resolved. The story has a villain. But nothing actually changes.

Replace the central bankers with other central bankers, the financial executives with different executives, the lobbyists with different lobbyists. The architecture produces the same pressures. The same rational responses emerge. The outcomes follow.

This isn’t a cynical take. It’s actually the more hopeful frame, because blaming character is a dead end and examining structure opens a door. The question worth asking isn’t “are these people greedy?” — it’s “what does the structure reward?”

The honest answer, in a monetary system with a discretionary money supply: it rewards being closest to the source. It rewards being the institution that accesses new money before prices adjust. It rewards holding assets rather than savings. None of those rewards require anyone to be evil. They follow from the architecture.

The Move Available to the Individual

You cannot redesign the Federal Reserve. No individual can. The architecture of the monetary system was built over a century by legislation, international agreements, and institutional precedent. Voting in different central bankers doesn’t change the structural incentives they operate within any more than changing the pilot changes the flight path programmed into the autopilot.

So what can an individual actually do?

Bitcoin offers something specific here — and it’s worth being precise about what that something is.

Bitcoin isn’t invisible to the existing system. Major financial institutions hold it. ETFs tracking its price are listed on regulated exchanges. Governments are actively debating whether to include it in strategic reserves. The existing financial architecture increasingly recognizes it, prices it, and interacts with it. It isn’t outside the system in the sense of being irrelevant to it.

But the existing architecture cannot alter it.

No committee can vote to increase its supply. No central bank can create more of it to manage a crisis. No institution sits closest to a Bitcoin money printer, because there is no printer. The issuance schedule — already more than 93% complete — is written in code and enforced by every node in the network simultaneously. The Cantillon Effect cannot operate through Bitcoin the way it operates through fiat, because there is no discretionary expansion for any actor to be first in line to capture.

This is the distinction the individual can act on. You cannot change the architecture of the fiat system. But you can move wealth into something that the architecture increasingly acknowledges — while remaining unable to change it. It’s recognized by the machine. It is not governed by it.

That’s not a small thing.

The question isn’t whether the people running the financial system are good or bad. Most of them probably are good — working within incentive structures they didn’t design and largely don’t question, doing what the architecture rewards because that’s what architectures do.

The question is what the structure rewards.

Once you see it that way, the anger dissolves. And something more useful takes its place.