You Can't Eat a T-Bill (or a Dollar, or a Stablecoin)

Why stablecoins can prolong, but not save the US deficit

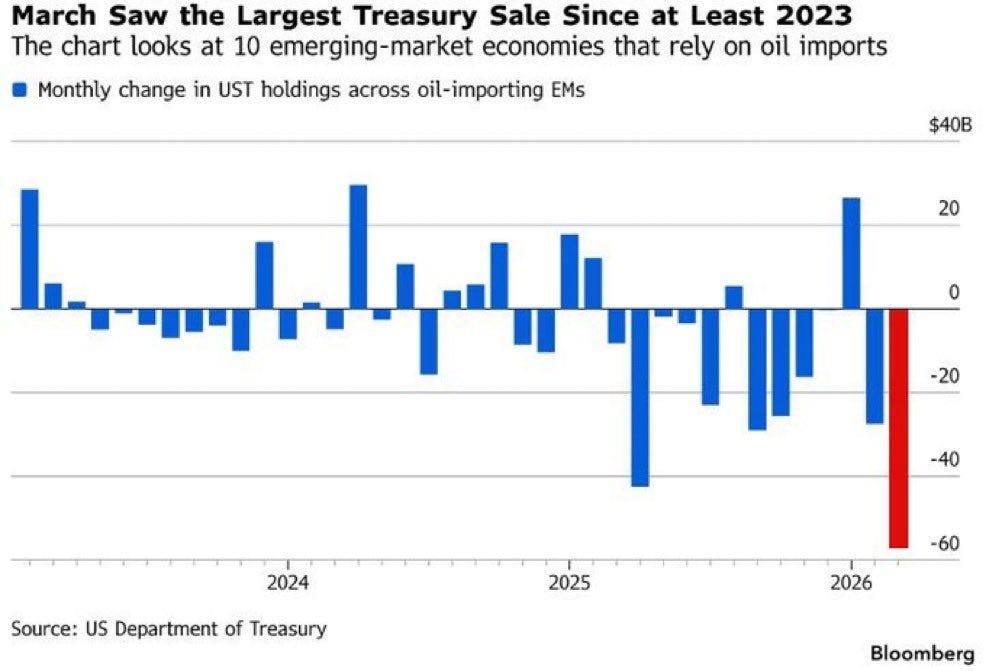

In March 2026, oil-importing emerging markets sold the most US Treasuries in at least three years.

No panic or crisis summit so no big headlines. Just a slow, coordinated decision playing out across numerous EM central banks: when the choice was between holding American paper and buying the energy to keep their economies running, they chose the energy.

That’s what happens when financial instruments compete with survival. And it sets up a question the stablecoin boom hasn’t answered yet.

The plan seems elegant. If the world holds US dollar stablecoins backed by USTs, those tokens need Treasuries behind them. New stablecoin demand becomes new Treasury demand. At a moment when the US government is running deficits that need continuous financing, the math is genuinely appealing.

Luke Gromen at FFTT has written about this connection directly. The stablecoin legislation being pushed by Treasury and Bessent is shaped around the deficit problem. The idea: manufacture offshore dollar demand, park it in T-bills, and keep the creditor line moving even as traditional buyers pull back. The logic holds up. If the world holds stablecoins, the issuer holds Treasuries.

My prior article, The Dollar’s Last Guarantee traces the full backstory on how the dollar arrived at this moment:

What the plan assumes, though, is that the world will keep holding.

Food and energy sit at the base of the hierarchy of needs. Financial instruments sit somewhere higher up — useful when the basics are covered, expendable when they’re not. The hierarchy has a rate of exchange. When oil prices spike, the exchange rate between dollars and survival goods shifts, and central banks act accordingly.

When the Strait of Hormuz closed and oil prices climbed, oil-importing economies ran the same basic calculation: hold the dollar claim, or use it to buy the energy. They used it to buy the energy. The March chart from above shows the result.

The same logic extends to stablecoins. A stablecoin is a dollar. It spends like one, it can ostensibly buy oil like one. The US plan works as long as the world chooses to hold — and the preference ordering is clear and shows no sign of revision.

I had my own counterargument that I needed to work through:

“But a stablecoin is cash-like, not a bond. An emerging market doesn’t have to sell it to raise dollars, it can just spend it. The token moves to the oil seller, the T-bill stays on the issuer’s balance sheet. Where’s the problem?”

The mechanic is real. A stablecoin settles instantly; a Treasury takes time to sell, requires finding a buyer, and can move the price on the way out. A stablecoin could, in theory, circulate through the global oil market indefinitely without ever triggering a Treasury sale.

So to me, this is the reasonable objection. And it’s right, but only goes so far.

After further consideration, I think my own objection stops one step short.

A fully-reserved stablecoin exists as a financial instrument only while net holding demand exists. The token(s) can change hands a hundred times — that part of the objection is true. As long as the world holds as many coins as it redeems, the backing Treasuries sit untouched on the issuer’s balance sheet.

But holding is a choice made one holder at a time. When an EM spends a stablecoin to buy oil, the oil seller now holds it. That seller faces the same question: hold, spend, convert to something else (net result similar to spend), or redeem for cash. If they hold, spend, or convert, the coin moves to the next hand — and the backing T-bill stays where it is. The pressure only surfaces when someone wants their dollars back. At that point, the coin goes back to the issuer, who has to sell the backing Treasury to fund the redemption. And there has to be a willing buyer.

Spending or converting relocates the question. Each transaction hands it to a new holder, but no transaction resolves it. The hot potato moves down the chain until someone decides they want cash — and at that point, whoever issued the coin has to deal with what comes next.

Now the mechanism becomes the trap.

Two kinds of stablecoins exist in meaningful scale.

The first kind is the regulated & fully-reserved variety like Circle’s USDC, now operating under an emerging U.S. stablecoin framework. USDC is backed one-for-one by cash and highly liquid cash-equivalent assets, with most reserves held in a BlackRock government money market fund invested in short-dated Treasuries, Treasury repo, and cash. Institutional Circle Mint customers can redeem directly; everyday users typically access redemption indirectly through exchanges, though Circle says it will redeem presented USDC in compliance with MiCA. Every token in circulation corresponds to reserve assets that are heavily Treasury-linked. This is the coin the deficit-funding thesis requires.

Tether’s USDT operates under different rules. Backed by a broader, less cash-equivalent reserve mix, holding a mix of Treasuries, Bitcoin, and gold. Most retail holders can’t redeem directly so they sell on an exchange instead, which buffers the issuer from direct redemption pressure. That coin has genuine circulation properties. It moves through markets without triggering the one-to-one obligation. Or at the very least, not as easily.

The problem is that these two designs are in tension with each other. A coin rigid enough to park money in Treasuries at the scale the thesis requires is also the one that gets converted or redeemed when the world decides it needs oil more than dollar exposure.

A coin loose enough to circulate freely and absorbing velocity, drifting from hand to hand without forcing a redemption, doesn’t serve the deficit-financing goal. The US can design toward one or the other. The distance between them is where the plan gets complicated.

For the domestic banking angle — what yield-bearing stablecoins do to bank net interest margins — I covered that in the article below:

One more element worth considering.

A US Treasury has friction. To exit, you find a buyer, accept a price, wait for settlement. That process takes time, and time functions as a kind of grip — the inconvenience keeps holders in the position longer than pure preference might dictate. Whether or not the friction was designed with this in mind, it works as a stickiness mechanism.

A stablecoin strips that out. It moves like cash. No bid-ask spread, no settlement window, no counterparty to locate. You hold it until you want something else, and then you swap it.

The timing problem is real. The US has made the dollar claim significantly easier to exit at exactly the moment it needs dollar claims to be sticky. Frictionlessness is usually a feature. In a captive-buyer scheme, it’s a design flaw.

Iran is already accepting stablecoins for Hormuz transit payments — alongside yuan and Bitcoin. The oil sellers receiving them aren’t running a redemption calculation. They’re running a preference calculation: hold a dollar instrument, or hold something harder.

In the long run, that’s the more consequential question. Stablecoins will function more and more like cash — circulating, spending, moving through the system without the mechanics described above becoming the primary constraint. As that happens, what matters less is who redeems what. What matters more is whether people want to hold dollar-denominated instruments at all.

Demand for Bitcoin and gold has been growing relative to demand for fiat claims, and a stablecoin is a fiat claim. Whatever gravitational pull draws capital away from the dollar pulls on the stablecoin too. The wrapper is different; the underlying exposure is the same.

Bitcoin, in this framing, is less a mechanism than a signal. Each time an oil seller prefers it to a dollar claim, the preference ordering the scheme depends on shifts a little further.

The US wants the world to hold dollars. The world wants to hold what dollars buy. A stablecoin just makes the swap faster.